Should I Participate in ESPP at Work? 5 Situations to Consider.

When you think about your employer benefits a question you should ask yourself is “Should I participate in ESPP at work?” If you have this benefit it may not be clear why you would participate.

At first, ESPPs may not seem as attractive as receiving RSUs or even your 401k match. They can be confusing and contributions may seem small.

However, when you look beneath the surface it becomes clear how useful these plans are in accumulating your wealth and vested shares of your employer. But even with a great employer benefit like ESPP, it is important to understand under which circumstances you would use it.

To understand if ESPP is worth it, you will need to learn:

- What it is and how it works?

- How is an ESPP taxed?

- Should you prioritize it based on your ability to afford it?

- How does it compare to saving in your 401k?

- Can you pair it with RSUs?

- Do you use it if you have already accumulated a large amount of your employer’s stock?

- Is it appropriate to use if you are saving for a big purchase like a house?

This is a long one. If you already read five articles on ESPPs you can skip the first two sections. However, I do think my explanation takes a unique angle and there are a ton of awesome charts!

What is an ESPP?

An Employee Stock Purchase Plan (ESPP) is an arrangement between you and your employer. It allows you to buy company stock through payroll deductions. You can contribute the lesser of up to a maximum of $25,000 per calendar year. An ESPP usually allows you to buy your employer’s stock at a discount, anywhere between 1 to 15%.

An ESPP has three key dates: the offer date, the purchase date, and the sale date. These dates will impact how your ESPP is taxed.

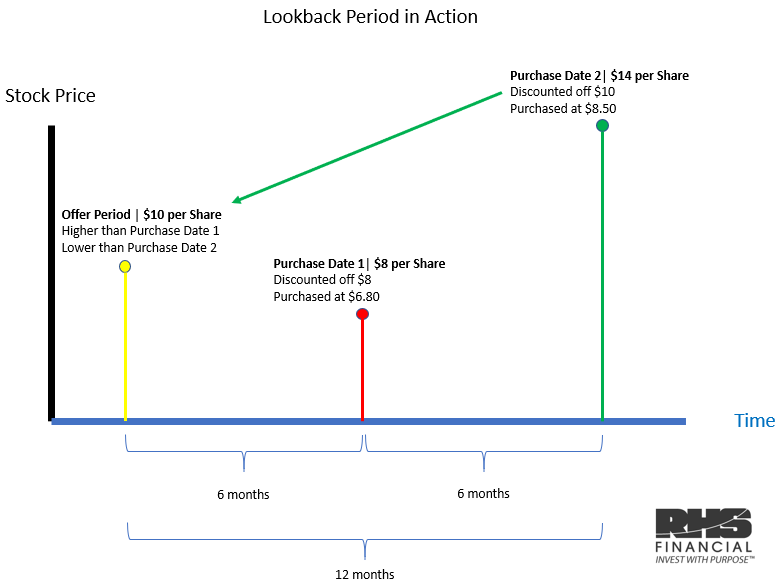

Traditionally ESPP has a 12-month offer period starting at the offer date. Usually, it will have two purchase periods every 6 months. Your paychecks will be deducted beginning on the offer date and continuing through to each purchase date.

In addition, some ESPP plans offer a lookback feature. A lookback feature applies the discount to the lower price between the current purchase date and the offer period.

ESPPs Differences

There are two types of ESPP plans that you may encounter. A section 423 plan (tax-qualified) and ones that don’t fall under any IRS provision (non-qualified). A tax-qualified ESPP will require you to keep a close eye on the date of the offer and the purchase date to make the most tax-intelligent decision around the date of the sale.

ESPPs can be structured differently. So it is important that you speak to your employer before making any decisions with ESPPs. The discounts, key dates, lookback provisions, and more, such as your ability to withdraw the money prior to the purchase date, can all be different.

For the purpose of this article, I am going to assume that you have a tax-qualified ESPP with a 15% discount, a 12-month offer period with two 6-month purchase dates and that you have a lookback provision available.

As with any complex financial concept please consult your tax advisor or financial advisor.

How is an ESPP taxed?

ESPP tax rules are some of the most complicated in the world of equity compensation. To make sense of them it is important to understand:

- how the lookback period works

- how the discount works

- the key dates

- the difference between a disqualifying disposition and a qualifying disposition

Lookback

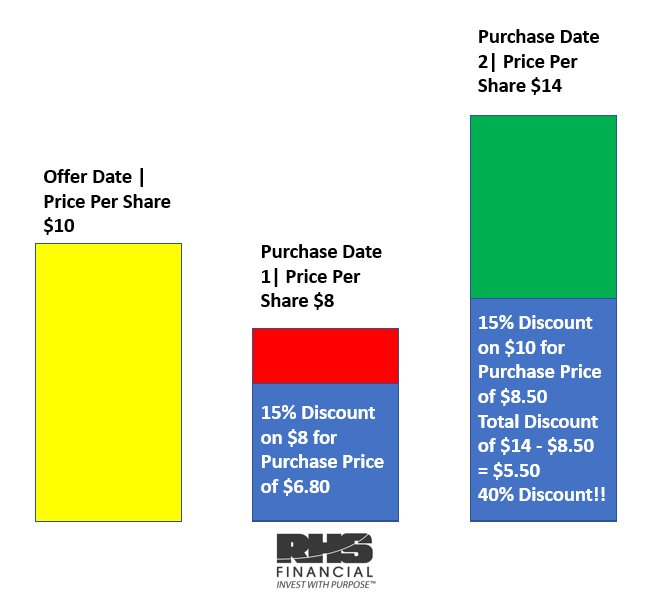

ESPP plans that have a lookback period will allow you to apply the discount to the lower stock price between one of two dates. Either the offer period price or the current purchase price.

In our assumption, an ESPP discount of 15% is applied to the lower of the two prices. If the lower of the stock prices is $10 you will have the opportunity to buy it at $8.50. If the lower of the stock prices is $8 you will have the opportunity to buy it at $6.80.

Key Dates

The key dates include:

- the offer period

- the purchase period

- when you actually sell

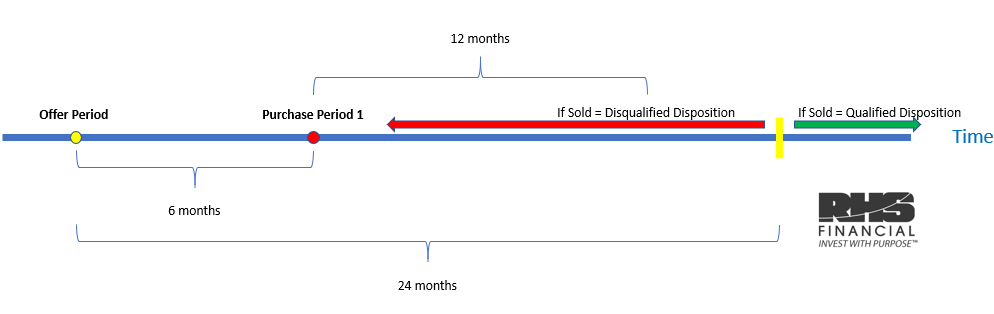

The offer period starts the 12-month window of activity. In which purchase periods occur every 6 months. If the offer period is in January then the first purchase date is in July and the second purchase date is in December.

Once the stock has been purchased it is mostly up to you to choose when to sell it. Most companies will have blackout periods and trading windows. You will need to abide by those rules.

Now that you know how the lookback period, the discount, and the key dates work let’s talk about the actual tax ramifications.

Once you have purchased your stock your decision of when to sell will result in either a disqualified disposition or a qualified disposition. Disposition is a sale, a transfer (out of your ESPP plan), or a gift.

In order to have a qualified disposition, you must sell your shares 2 years after the offer period and 1 year after the purchase.

ESPP Disqualifying Disposition

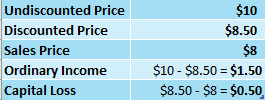

A disqualifying disposition is much easier to understand. Taxes on a disqualifying disposition have two components. The first component is the difference between your discounted purchase price and the undiscounted price of the stock. And the second component is the difference between the undiscounted price and the sales price.

In a disqualifying disposition, where you don’t meet the holding requirement, the difference between the purchase price and the undiscounted price of the stock is treated as ordinary income, just like your W-2 income. The difference between the undiscounted price and your sales price is treated as capital gains or loss.

In a disqualified disposition, even if you sell the stock at a loss you will still owe ordinary income tax on the discount value!

ESPP Qualified Disposition

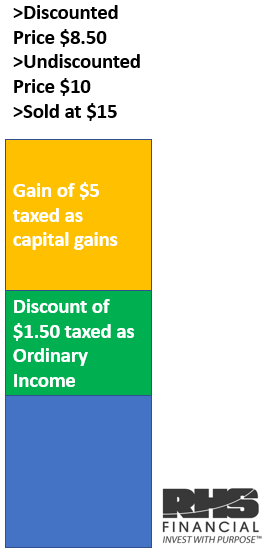

A qualifying disposition is more complex in its tax implications.

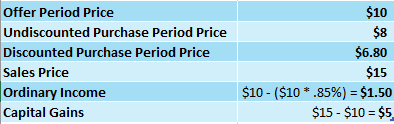

Your ordinary income will be dependent on the lesser of your gain (sales price – purchase price) or the purchase price discount. Unlike the disqualified disposition, the purchase price discount is based on the hypothetical discount price on the offer date. Whether your purchase price was calculated based on the offer date or the purchase date doesn’t matter. This is extremely important to understand!

Finally, the difference between the offer date price and the sale price will all be taxed as capital gains.

Should I participate in ESPP if I can afford it?

Alright, so now you know the basics and you are ready to dive in. If you can afford setting aside some of your paychecks is ESPP worth it? The bigger the discount your company offers you the better deal the ESPP is. If they offer you the lookback provision it’s even a better deal.

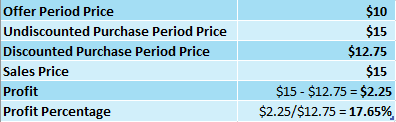

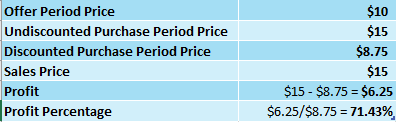

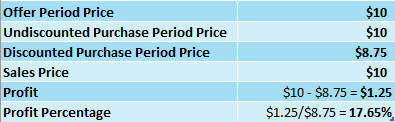

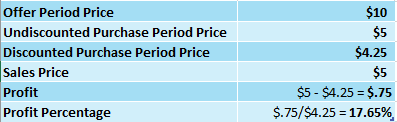

If you choose to sell your ESPP shares right away you will make money no matter if the stock price has gone up, down, or stayed flat. Let’s look at a few examples.

Even when the stock price has gone down, with a 15% discount, you automatically make a 17.65% profit. Since it doesn’t stay in the market for long, if at all, this is a great return for a relatively “risk-free” investment.

At the very least you should consult with your financial advisor to figure out your cash flow and see if you can take advantage of an ESPP.

Should I participate in ESPP if I have a 401k?

Speaking of “risk-free” investments and the profits they bring, one of the best benefits employers can give you is a 401k match. If your employer, for example, matches you 5% of your total salary then that is an instant 100% return that has been accomplished risk-free. There are no investments out there like that.

When it comes to balancing your 401k with your ESPP you should always prioritize the match. If your intention is to sell your ESPP shares right away you should focus your attention on maxing out your ESPP next.

Even if you have a super-high tax rate between federal and state, let’s say hypothetically 50%, an instant return of 8.8%(17.65% * 50%) is phenomenal.

Should I participate in ESPP if I have RSUs?

ESPP isn’t the only way you can participate in your employers’ success. It is very common for high-value employees to have a combination of RSUs and ESPPs. If your intention is to accumulate your employers’ shares there is a clever way you can pair RSUs and ESPPs.

In a prior article, I wrote that RSUs are simply wage income in the form of company shares. Once your RSUs vest there are no additional tax benefits for holding them. This is not the case for ESPP shares due to ESPP tax rules and ESPP qualifying disposition.

If you intend to accumulate shares of your employer consider selling your RSUs as they vest and instead accumulate ESPP shares. This way you will naturally hit the qualifying disposition as you continue to hold employer shares.

Should I participate in ESPP if I have a lot of my employers’ stock?

ESPP tax rules provide for opportunities to swap shares that you currently have and the shares that you just received via the ESPP. However you may have come into possession of your employers stock, chances are likely that the cost basis at which you have received them varies. If the price of shares has fluctuated over your accumulation period you may have shares that have a gain, a loss, or are basically flat.

Consider selling some of your existing shares and replacing them with newly accumulated shares of ESPP.

When you meet the holding requirement, the tax rules state that everything will be taxed as long term capital gains based on the difference between the offer price and the sales price.

Therefore consider this prioritization schedule for swaps:

- Existing shares that are at a capital loss. You can use this to offset other capital gains and deduct up to $3,000 off your ordinary income.

- Shares that have no gains. No gains equals no taxes.

- Shares that have a cost basis higher than the purchase price of your ESPP shares. You are swapping a higher tax bill for a lower one.

Should I participate in ESPP if I am saving up for a big purchase?

ESPP shares have a great “risk-free” return, net of your taxes when you trigger an ESPP disqualifying disposition. If you have the discipline and the ability to sell them ASAP they are great for short-term/mid-term savings goals.

Imagine being able to save $25,000 a year for a down payment but getting an automatic 17.65% return. This is so much higher than any rate of return a bank can offer you.

While you should be able to answer “Should I participate in ESPP?” don’t hesitate to reach out to your financial advisor and get the help you need.

2024 Disclosures

RHS Financial is an SEC registered Investment Advisory Firm and distributes this presentation for informational purposes only. This presentation ( hitherto referred to as the presentation throughout this disclosure), blog post, infographic, slide deck or whatever form of informational modality the reader wishes to describe this as is provided for informational purposes only and should not be construed as investment advice in any way.

We believe the information, including that obtained from outside sources, to be correct, but we cannot and do not guarantee its accuracy in any way. RHS Financial uses information from outside sources to develop graphs, charts, infographics, etc. to enhance this presentation and while we believe the information from these outside sources, to be correct, we cannot and do not guarantee its accuracy in any way,

Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors who may be employees of but do not necessarily reflect the views of RHS Financial as a company. There can be no guarantee that developments will play out as forecasted. The information in this presentation is subject to change at any time without notice. This presentation contains “forward-looking statements" concerning activities, events or developments that RHS Financial expects or believes may occur in the future. These statements reflect assumptions and analyses made by RHS’s analysts and advisors based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond RHS Financials’ control, they are no guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements. In a nutshell; these are our best guesses and please don’t assume they are fact.

Mentions of specific securities, investment products, investment indices, companies or industries should not be considered a recommendation or solicitation. Data and analysis does not represent the actual or expected future performance of any investment or investment product Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This post may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with RHS Financial and does not sponsor, endorse or participate in the provision of any RHS’ services, or other financial products. Index information contained herein is derived from third parties and is proffered to you unaltered as we derived it from the third party.

RHS Financial, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where RHS Financial, LLC and its representatives are properly licensed or exempt from licensure. This presentation is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place.

If the client is deemed suitable and agrees, RHS may employ leveraged strategies for these clients. Leverage attained through margin on a client’s account can add additional risk. While RHS tends to seek to improve return with theses strategies by applying leverage to less risky indexes, there is no guarantee that that RHS will lower risk or improve returns.

RHS Financial. 4171 24th St. Suite 101 San Francisco, CA 94114