Maximize Your Tech Equity: Offer Acceptance to Long-Term Growth

A hot topic within the Silicon Valley tech professionals’ circles is total comp. If you want to read debates about the subject, go no further than TeamBlind.com. There, you’ll read how people define total comp, along with lively discussions about how people determine if their total compensation package is fair.

Most agree that total comp is generally seen as your base salary + bonus + equity. However, most people don’t agree on what is fair. Especially when it comes to equity. If you are evaluating taking a job at a start-up, series E company, or a publicly traded mega-firm, then you need to know if your total comp package includes a fair share of equity.

Once you have received an equity grant, your journey to make the most of it starts. You have to navigate important decisions around exercising, selling, or holding during events such as lockups, tenders, IPOs, and decisions influenced by external and internal factors. Your financial future often depends on these important, strategic decisions.

RHS Financial is a leading Bay Area financial advisor specializing in this exact dilemma. The core of our business is to provide fiduciary advice and sophisticated financial planning that allows Silicon Valley tech professionals the tools to properly evaluate and manage their compensation packages and the tax ramifications that come with them.

In this blog, we will provide you with ways to evaluate if your equity compensation offer is competitive and how to decide what you should do with your equity once you actually have it.

How Tech Executives Evaluate Their Equity Compensation

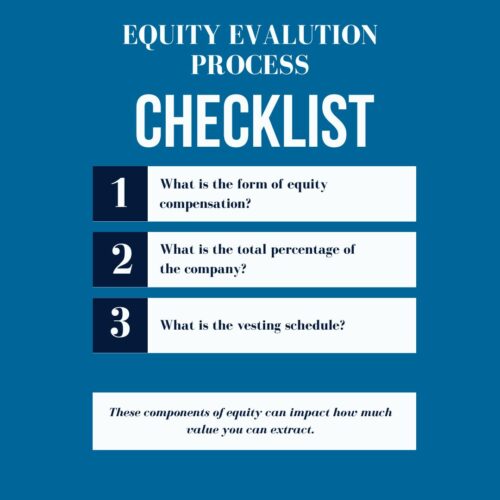

The equity evaluation process consists of understanding what you are getting and how it compares to your peers. As you are evaluating your offer you will want to have a good grasp on these two components and use them for negotiating.

Several components of equity can impact how much value you can extract.

1. Form of Equity Compensation:

- Restricted Stock Awards: RSAs are usually awarded to the earliest-stage employees. It’s common to be offered thousands of shares for pennies on the dollar. If you are awarded RSAs, you should file an 83(b) election within 30 days with the IRS. This will allow you to capture most of the value through capital gains rather than ordinary income.

- ISOs vs NQSOs: Depending on the stage of the company you may be offered stock options. ISOs are usually preferable to NQSOs for their tax benefits. However, per IRS rules, a company can only offer you so much in ISOs. When possible, negotiate for as many ISOs as you can. Ask if early exercising is allowed at the company and use it if you can to avoid Alternative Minimum Tax (AMT) on ISOs.

- RSUs: Restricted stock units RSUs are basically W2 income. The value can fluctuate depending on the market perception of the company. RSUs are typically awarded at publicly traded companies or those about to go through an IPO. If the company is not public, you may consider asking for NQSOs instead. RSUs will generate a tax bill on the IPO, and if there is a blackout period, you may not be able to sell to cover taxes for six months. In which period the stock price could drop.

2. Total Percentage of the Company:

- Early Stage Company: Total percentage matters if you are a founding employee or on the ground floor initially. The chances of you seeing liquidity with your equity in the near future are very low. So you want to make sure that if and when it eventually happens, you get a sizable payoff. Understand that you will likely experience dilution as the company raises funds. Don’t be afraid of dilution and not owning 1% of the company when it goes public. Dilution is natural and usually increases the value of your stock.

- Late Stage and Public: If the company is in later rounds, then the total percent of the company matters less than the valuation. At this stage, your compensation is evaluated purely on its current and short/mid-term monetary potential.

3. Vesting Schedule:

- Vesting schedules: Most follow a four-year schedule with a one-year cliff. You may see your equity vesting over five years. You may also see your equity vesting every year instead of every quarter or every month. Less time to fully vest and more frequent vesting is better.

- Legal Considerations: If you want to learn more about what to look out for in an equity grant document, read THIS blog. However, I will summarize some key points:

- Clawbacks: A legal clause that may force you to sell your shares back to the company in certain situations, such as getting laid off or quitting before an IPO or acquisition. Worse yet, full forfeiture due to violation of any other legal clauses in the equity grant agreement.

- Right of First Refusal: Rights of first refusal are common in most equity grant agreements, but their use varies. Specifically, you want to know if you can sell your shares to other third parties before the company becomes public. This is important for early-stage companies. You may see the value of your shares skyrocket, but no liquidity on the horizon. In this case, you may want to sell in a secondary market, assuming your equity grant agreement allows you to do so.

- Double Trigger Acceleration Upon Change of Control: The more important you are to the company, the likelier you can negotiate that your vesting will accelerate in the case of a merger or an acquisition in which you are terminated.

- Date of the Grant: If you get hired you don’t always get your grant awarded right away. Make sure you negotiate the grant date as early as possible. This is especially important if you are awarded stock options and the exercise price depends on fair market value. If the fair market value goes up between your hire date and grant award date, such as in the case of a new financing round, then your tax benefits and value will be worth less.

Evaluating your equity compensation is the first step in negotiating intelligently. You will want to negotiate based on the stage of the company, industry standards, and how you perceive the opportunity and your value.

At earlier-stage companies, cash-strapped founders may offer more equity instead of cash base and bonuses. If you are joining a start-up in its formative years, you can evaluate your decision as both a venture capitalist and a founder yourself. Ask yourself these questions:

- Is this a good long-term investment?

- Are they solving the most pressing problem?

- Is this the trending or potentially trending vertical of tech?

- Is the team capable of delivering a successful product to market?

You will also want to evaluate what value you will bring to the team and the company.

Can you make a difference that will make your equity eventually worth something? From there, you can decide whether to ask for more equity instead of cash or vice versa.

At later stages of the company, industry standards of compensation will be a more reliable way to evaluate your total compensation and equity.

Here are great resources to help you evaluate your offer(s):

- Ask your peers using Teamblind.com, but be wary of biased and jealous answers

- Use Wellfound and Teamblind tools.

- Use attorneys like Mary Russell from Stock Option Counsel to help you evaluate and negotiate.

Finally, consider talking with a San Francisco Bay Area financial advisor to understand any personal finance and tax implications of your equity grant.

Tech Executive Equity Compensation: Exercise, Keep, or Sell

Now that you have secured the best possible equity grant, you will have some additional decisions to make.

Exercising

If you have Incentive Stock Options (ISOs), you may consider doing an early exercise. This will allow you to save significantly on taxes later as you transform ordinary income into capital gains or avoid alternative minimum taxes.

If you have Restricted Stock Awards, you will want to file an 83(b) election with the IRS. Coincidently, a similar document as for the early exercise on ISOs. This will allow you to recognize the income on the shares at a much lower price, assuming the company does well, and start the long-term capital gains timer.

If you have Non-Qualified Stock Options, you may consider waiting to take full advantage of the time value and wait for the equity to appreciate.

As always, we recommend that you work with a qualified Bay Area CERTIFIED FINANCIAL PLANNER ® Professional who specializes in helping tech employees sort through the complexities of managing stock compensation.

Hold or Sell

Deciding to hold or sell your equity is a personal decision and evaluation of your financial situation. If the company is not publicly traded, you may not even have a choice to sell.

Here is the checklist of questions to ask yourself:

- How important are my short-term and long-term goals? Are they must-have or nice to have? If they don’t get accomplished, will it jeopardize your future? Less important goals allow you to take more risk and hold more equity.

- Do I have other assets that can accomplish these important goals? If so, then you can hold more of your employer’s stock.

- How old am I? If you have your entire career and years of earnings before you, consider taking a bigger gamble. Consider selling more if you have responsibilities such as children, and think more about retirement as you age.

- What percent of my entire wealth is my equity? If it’s the majority, you may consider selling some shares.

- Are you bullish or bearish on the future of the company? Try not to be blinded by your enthusiasm or depressed by your distaste for your job.

- How sophisticated of an investor are you? Do you understand the risk of investing in one company? Are you familiar with market cycles? Do you have hedging strategies in place? If you are uncomfortable with these topics, consider having a lower concentration of employer stock in your portfolio.

The path from evaluating and negotiating your offer to finally managing your equity is significant, and filled with challenges. However, it’s also potentially transformative. With the right knowledge and resources, you’re set up for success in this exciting venture.

Why Partner With RHS Financial?

Since 2009, the RHS Financial team has been helping tech professionals manage their wealth with a purpose. We specialize in helping you understand the ins and outs of your equity compensation while helping you build sustainable wealth.

Connect with us here to learn about our wealth management services for Silicon Valley tech professionals.

2024 Disclosures

RHS Financial is an SEC registered Investment Advisory Firm and distributes this presentation for informational purposes only. This presentation ( hitherto referred to as the presentation throughout this disclosure), blog post, infographic, slide deck or whatever form of informational modality the reader wishes to describe this as is provided for informational purposes only and should not be construed as investment advice in any way.

We believe the information, including that obtained from outside sources, to be correct, but we cannot and do not guarantee its accuracy in any way. RHS Financial uses information from outside sources to develop graphs, charts, infographics, etc. to enhance this presentation and while we believe the information from these outside sources, to be correct, we cannot and do not guarantee its accuracy in any way,

Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors who may be employees of but do not necessarily reflect the views of RHS Financial as a company. There can be no guarantee that developments will play out as forecasted. The information in this presentation is subject to change at any time without notice. This presentation contains “forward-looking statements" concerning activities, events or developments that RHS Financial expects or believes may occur in the future. These statements reflect assumptions and analyses made by RHS’s analysts and advisors based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond RHS Financials’ control, they are no guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements. In a nutshell; these are our best guesses and please don’t assume they are fact.

Mentions of specific securities, investment products, investment indices, companies or industries should not be considered a recommendation or solicitation. Data and analysis does not represent the actual or expected future performance of any investment or investment product Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This post may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with RHS Financial and does not sponsor, endorse or participate in the provision of any RHS’ services, or other financial products. Index information contained herein is derived from third parties and is proffered to you unaltered as we derived it from the third party.

RHS Financial, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where RHS Financial, LLC and its representatives are properly licensed or exempt from licensure. This presentation is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place.

If the client is deemed suitable and agrees, RHS may employ leveraged strategies for these clients. Leverage attained through margin on a client’s account can add additional risk. While RHS tends to seek to improve return with theses strategies by applying leverage to less risky indexes, there is no guarantee that that RHS will lower risk or improve returns.

RHS Financial. 4171 24th St. Suite 101 San Francisco, CA 94114