How Much Investment Risk Should I Take?

When you engage a financial advisor, enroll in a 401(k) at your workplace, or initiate a new investment strategy, one of the pivotal questions often posed is about your “investment risk tolerance.” Understanding your risk tolerance – a crucial aspect in an investor’s capacity and willingness to endure potential losses in pursuit of greater future gains – is typically a determining factor in establishing your strategic asset allocation. This allocation, which is the specific blend of stocks, bonds, and cash forming the core of your portfolio, hinges significantly on evaluating your investment risk tolerance.

However, when addressing the fundamental query of personal investing – “How much investment risk should you take?” – most individuals, including many professionals, still predominantly depend on subjective assessments and conventional heuristics. These methods, while popular, may not comprehensively address the nuances of investment risk management.

Here at RHS Financial, we have devised a superior way of evaluating and applying investment risk. If you are interested in the data behind much of this article read our white paper here. And if you want to see how these ideas can improve your ability to be financially free schedule a free 15-minute consultation with us using THIS link.

Challenges with current methods of getting investment risk right

The most prevalent approaches are age-based rules and personal attitude questionnaires. Age-based rules, like the longstanding formula of holding “100 minus your age in stocks,” allocate stocks and bonds based on the investor’s age. This rule operates on the assumption that younger investors, having a longer time horizon, can afford greater exposure to investment risk and therefore should allocate more towards stocks. Conversely, older or retired investors, focusing on capital preservation, should incline more towards bonds. Such age-based strategies have become the cornerstone of target-date retirement funds, now a staple in 401(k) plans, where the investment mix shifts from riskier stocks to safer bonds and cash as the retirement date nears.

However, it’s evident that these target-date funds and age-based guidelines offer a one-size-fits-all solution, failing to consider an individual investor’s unique circumstances and goals. This oversight might lead to suboptimal investment risk management.

Another widely used method to measure risk tolerance is through personal attitude questionnaires. These questionnaires attempt to discern an investor’s psychological inclination towards financial risk by assessing their loss aversion and gain-seeking behavior. Although these questionnaires might align an investor’s portfolio with their comfort level, they may not necessarily address their financial needs in a holistic manner. While unlikely to result in wildly inappropriate recommendations, there’s little assurance that these methods are precisely optimal in managing investment risk.

In summary, while traditional methods of determining investment risk tolerance and asset allocation have their merits, they might not always provide the most tailored or effective strategy for individual investors. A more nuanced approach to investment risk management that considers personal circumstances and financial goals is essential for creating a truly personalized investment plan.

The better approach to investment risk

Investors typically have a primary goal when choosing a strategic asset allocation: to minimize the risk of failing to meet their financial needs, such as running out of money in retirement. A secondary objective often involves maximizing their expected total wealth. For instance, if two portfolios (A and B) have an equally high probability of success, but portfolio B generates significantly more wealth on average, then B is the preferable choice.

To refine this process, our team at RHS Financial has embraced a sophisticated approach to investment risk management: the Monte Carlo tree search. This method not only simulates a vast array of potential market outcomes but also evaluates a broad spectrum of strategic decisions that could be made along the way. It then identifies the choices that yield the most favorable outcomes by specific metrics. This approach is akin to AI systems used in strategic games like chess or go, where the AI predicts several moves ahead to position itself optimally.

Let’s apply this to a practical scenario involving investment risk tolerance. Consider a young investor, Alice, with a 70-year investment horizon. Here’s how our application works:

- We simulate 5,000 potential return sequences for stock and bond markets over the next 70 years.

- For each possible stock-bond portfolio mix (in increments of 10%), we calculate the returns in each of the 5,000 market scenarios.

- We input Alice’s current financial status, her savings plan, retirement age, and expected retirement withdrawals. The system then assesses her portfolio value across various mixes and market conditions.

- Finally, we analyze all potential end-states to determine which asset allocation decision leads to the most beneficial outcome. This result traces back to the initial allocation decision, forming our recommended asset allocation for Alice.

Our application at RHS Financial is designed to provide clients with a personalized investment risk tolerance assessment. By simulating thousands of market return scenarios, it employs Monte Carlo tree search to craft a customized asset allocation glide path. This path not only offers an immediate strategic allocation but also outlines its likely future adjustments. Such a tailored approach to investment risk management significantly enhances the probability of meeting our clients’ financial goals.

Through examples like Alice’s, it’s clear how a nuanced and dynamic approach can lead to more effective investment risk tolerance strategies, aligning closely with individual needs and maximizing the chances of financial success.

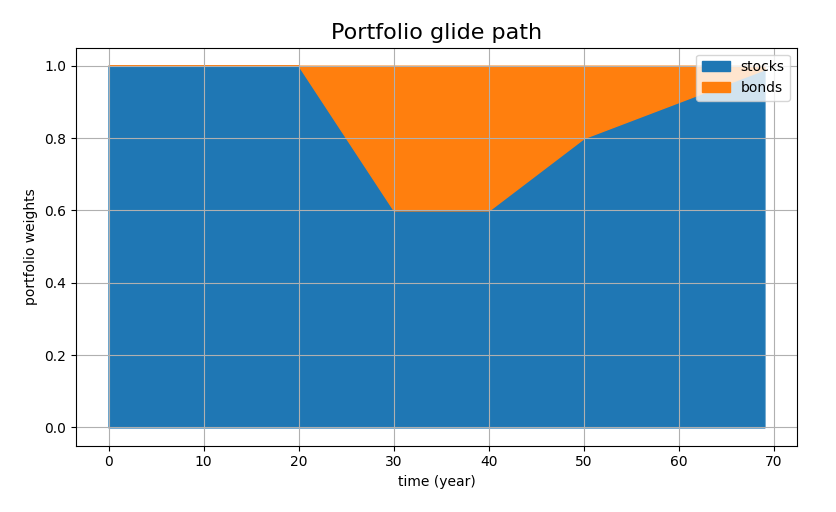

Two Alice’s

Let’s revisit our investor, Alice, who is at the outset of her career with a 70-year investment horizon. Initially, without investible assets, Alice plans to save $10,000 annually, increasing her savings to $40,000 by retirement. She aims to withdraw $60,000 annually from her portfolio during retirement. Utilizing our sophisticated software, we’ve crafted a personalized glide path for Alice’s investment journey, focusing on optimal investment risk management.

At the start, the software advises Alice to invest entirely in stocks, leveraging her long-term horizon and high investment risk tolerance. As she approaches retirement, the allocation gradually shifts towards bonds, becoming more conservative. This transition might seem similar to target-date funds, but the nuanced differences are crucial. Post-retirement, in a surprising twist, the glide path advises a gradual return to a full stock allocation by the end of her life. This counterintuitive strategy is a key outcome of our thorough investment risk analysis.

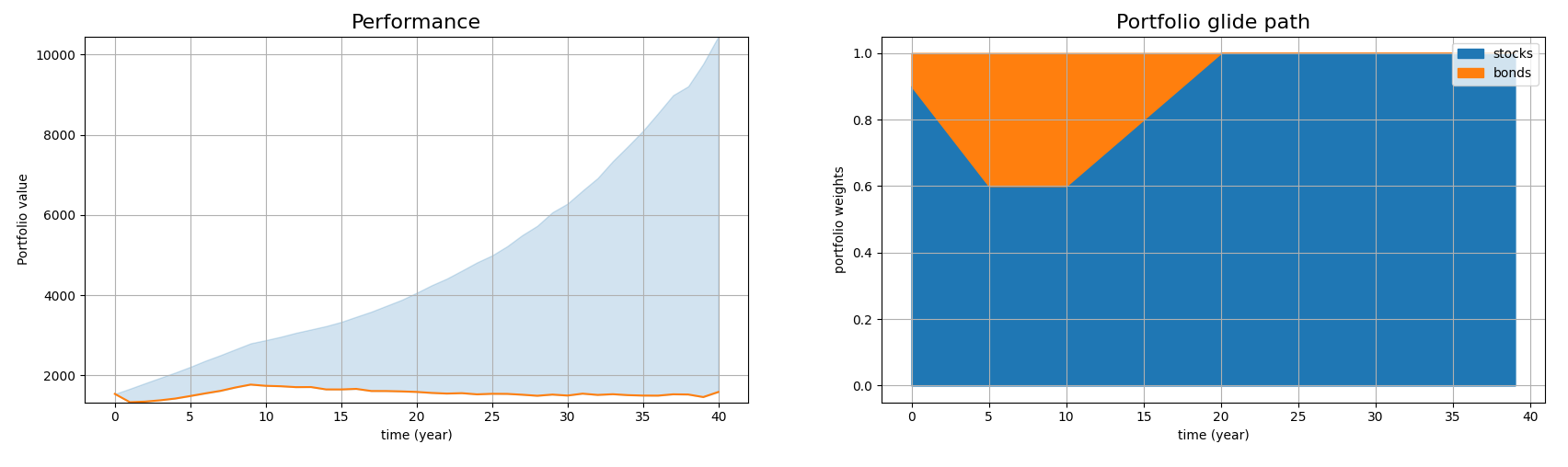

To illustrate this personalized approach, we plot Alice’s wealth projection under various scenarios. In the median scenario, her wealth continues to grow post-retirement, as investment returns outpace her withdrawals. Even in the less favorable 5th percentile scenario, Alice retains a substantial portion of her wealth. The application aims to maximize the “probability of success” – in Alice’s case, a 98.5% likelihood of financial sufficiency throughout her 70-year horizon. This metric is vital for effective investment risk tolerance planning.

However, our tool is not a one-time solution. Life changes and market fluctuations necessitate iterative consultations with the tool, particularly around major life events like retirement. Let’s fast forward 30 years. If Alice’s portfolio has grown as predicted, the revised recommendation may now suggest a higher stock allocation than initially planned, reflecting her improved probability of success and continued high investment risk tolerance.

Conversely, if Alice’s portfolio underperforms or she saves less than expected, the tool adjusts its recommendations accordingly. A more conservative strategy might be suggested, decreasing stock allocation to safeguard her financial future. This dynamic adjustment is a crucial aspect of personalized investment risk management.

This tool revolutionizes the approach to determining an investor’s risk tolerance and asset allocation. It provides nuanced, individualized strategies that can significantly diverge from standard target-date fund recommendations. By continuously adapting to an investor’s unique financial journey, our tool offers a sophisticated and tailored solution to managing investment risk and ensuring financial stability.

Interesting findings about investment risk

Our tool’s analysis challenges traditional notions of investment risk tolerance and asset allocation, particularly as it relates to age and retirement. Contrary to common belief, the main risk with stocks isn’t their inherent volatility, but the sequence-of-returns risk – most critical around retirement. This risk actually diminishes as one moves further from the retirement date – whether forwards or backwards in time – which means that risk tolerance doesn’t always decline with age.

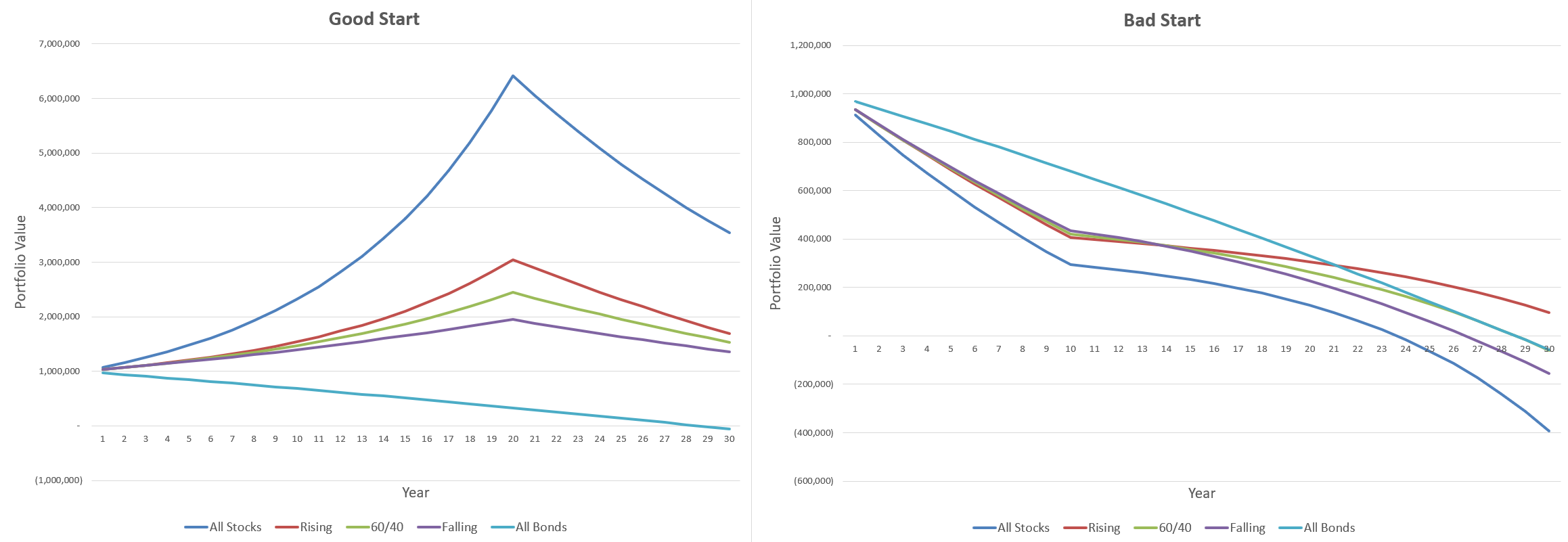

To illustrate this sequence-of-returns risk and how increasing equity exposure in retirement actually decreases risk, let’s consider a retiree with a $1 million portfolio, planning to withdraw $40,000 annually. We’ll explore two scenarios – “Good Start” and “Bad Start”. In the Good Start scenario, stocks earn 12% every year for the first 20 years and -5%/year in the last decade. The Bad Start scenario is reversed, with the negative decade up front and positive returns in the 20 years after. In both cases, bonds earn 1% constant real returns every year. For both scenarios, we evaluate the performance of five strategies: holding 100% stocks, 100% bonds, a constant 60/40 portfolio, a falling equity glidepath that starts at 60/40 and reduces stock exposure by 1% per year, and a rising equity glidepath that starts at 60/40 and increases stock exposure 1% per year.

Good Start Scenario:

- Scenario Description: Here, the retiree experiences strong stock market performance in the early years of retirement.

- Impact of Conservative Strategy (All Bonds): Although bonds are traditionally viewed as less risky, in this scenario, a purely bond-based portfolio may not keep pace with the withdrawal rate. The initially strong stock market performance means that a more aggressive strategy, with higher equity exposure, would have benefited the retiree. Being overly conservative, in this case, leads to the gradual depletion of funds, as the returns from bonds are not sufficient to sustain the portfolio in the long run.

- Optimal Strategy: A dynamic strategy, starting with a balanced mix but gradually increasing equity exposure, would capitalize on the early market gains, thereby sustaining and growing the portfolio despite regular withdrawals. This strategy results in the second-highest terminal wealth after an all-stock strategy.

Bad Start Scenario:

- Scenario Description: Contrarily, in this scenario, the retiree faces a declining stock market in the initial years.

- Impact of Early Equity Exposure: An aggressive allocation with high equity exposure becomes detrimental here. The early market downturn significantly reduces the portfolio value, and continued withdrawals further deplete it. By the time the market recovers, the portfolio is too diminished to benefit from the upswing.

- Optimal Strategy: In this case, a dynamic strategy that starts conservatively, with a higher bond allocation, and then shifts towards equities as the market begins to recover, would protect the portfolio during the initial downturn. As the market improves, increasing equity exposure would enable the portfolio to recover and grow, ensuring the retiree’s financial needs are met throughout retirement. This strategy is the only one in this scenario that successfully sustains withdrawals over the entire 30-year period.

While the average return of the stock market was the same in both cases, what mattered for the ultimate outcome of our investor was not how bad the risk of the market was, but when it occurred. Exposure to equity bear markets early in retirement was devastating, exposure to bear markets late in retirement was inconsequential. The strategy that best navigates this sequence-of-returns risk is one that is most conversative at the exact point of retirement and then becomes more aggressive as time goes on. A rising equity glide path in retirement generally outperforms traditional approaches whether markets do well or poorly in the early stages of retirement and is therefore generally favored by our Monte Carlo tree search approach.

Our application’s findings suggest several key insights:

- Increase in Stock Allocation Post-Retirement: Contrary to common practice, most investors should increase their stock allocation after retirement. This approach effectively navigates the sequence of returns risk.

- Timely and Decisive Risk Downshift: As retirement approaches, a rapid and significant shift to a more conservative portfolio is often necessary to mitigate the concentrated sequence of returns risk.

- Wealth and Equity Allocation: Investors with substantial wealth can afford – and indeed should consider – a higher equity allocation, while those with lesser means might also need a high equity exposure to meet their financial goals.

- The ‘Goldilocks U-turn’ in Asset Allocation: A sustainable financial trajectory usually features an asset allocation glide path that resembles a U-turn – higher equity exposure in youth and old age, with a conservative approach around retirement.

- Greater Equity Risk Than Traditionally Recommended: On average, investors might benefit from a higher allocation to equities than typically suggested by conventional age-based rules or standard target-date funds.

In conclusion, our tool offers an innovative perspective on strategic asset allocation and investment risk management. By tailoring recommendations to individual circumstances and adapting to changes over time, it challenges traditional approaches and potentially enhances financial outcomes for investors at any life stage.

If you want to see how these ideas can improve your ability to be financially free schedule a free 15-minute consultation with us using THIS link.

2024 Disclosures

RHS Financial is an SEC registered Investment Advisory Firm and distributes this presentation for informational purposes only. This presentation ( hitherto referred to as the presentation throughout this disclosure), blog post, infographic, slide deck or whatever form of informational modality the reader wishes to describe this as is provided for informational purposes only and should not be construed as investment advice in any way.

We believe the information, including that obtained from outside sources, to be correct, but we cannot and do not guarantee its accuracy in any way. RHS Financial uses information from outside sources to develop graphs, charts, infographics, etc. to enhance this presentation and while we believe the information from these outside sources, to be correct, we cannot and do not guarantee its accuracy in any way,

Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors who may be employees of but do not necessarily reflect the views of RHS Financial as a company. There can be no guarantee that developments will play out as forecasted. The information in this presentation is subject to change at any time without notice. This presentation contains “forward-looking statements" concerning activities, events or developments that RHS Financial expects or believes may occur in the future. These statements reflect assumptions and analyses made by RHS’s analysts and advisors based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond RHS Financials’ control, they are no guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements. In a nutshell; these are our best guesses and please don’t assume they are fact.

Mentions of specific securities, investment products, investment indices, companies or industries should not be considered a recommendation or solicitation. Data and analysis does not represent the actual or expected future performance of any investment or investment product Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This post may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with RHS Financial and does not sponsor, endorse or participate in the provision of any RHS’ services, or other financial products. Index information contained herein is derived from third parties and is proffered to you unaltered as we derived it from the third party.

RHS Financial, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where RHS Financial, LLC and its representatives are properly licensed or exempt from licensure. This presentation is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place.

If the client is deemed suitable and agrees, RHS may employ leveraged strategies for these clients. Leverage attained through margin on a client’s account can add additional risk. While RHS tends to seek to improve return with theses strategies by applying leverage to less risky indexes, there is no guarantee that that RHS will lower risk or improve returns.

RHS Financial. 4171 24th St. Suite 101 San Francisco, CA 94114