Am I Making Mega-Backdoor Roth IRA Mistakes?

If you’ve accumulated substantial wealth from your employment at a tech firm, you likely know about the mega-backdoor Roth strategy for its tax efficiency and ability to grow your retirement savings. This strategy, available in your 401(k), can be incredibly beneficial when used correctly.

However, there are common mistakes that can cost you hundreds of thousands in tax-free savings. As financial planners working with tech professionals in San Francisco, we frequently see these errors. Most of the big Bay Area tech companies offer a mega-backdoor Roth, but many people we talk with don’t understand all of the ins and outs of a mega-backdoor Roth.

In this article, I’ve outlined some key mistakes that tech professionals make with mega-backdoor Roths and how our team of San Francisco CERTIFIED FINANCIAL PLANNERS™ help you avoid costly mistakes that could impact you for years to come.

If you want to maximize your mega-backdoor Roth, feel free to reach out to us and schedule a 15-minute consultation using this link.

Understanding the Difference Between a Roth and a Mega-Backdoor Roth

Before we get into too much detail, we wanted to clarify the difference between a Roth and a mega backdoor Roth.

A Roth IRA is an individual retirement account that allows you to contribute after-tax dollars, with the benefit of tax-free growth and tax-free withdrawals in retirement.

Contribution limits for a Roth IRA are relatively low, and there are income restrictions on who can contribute:

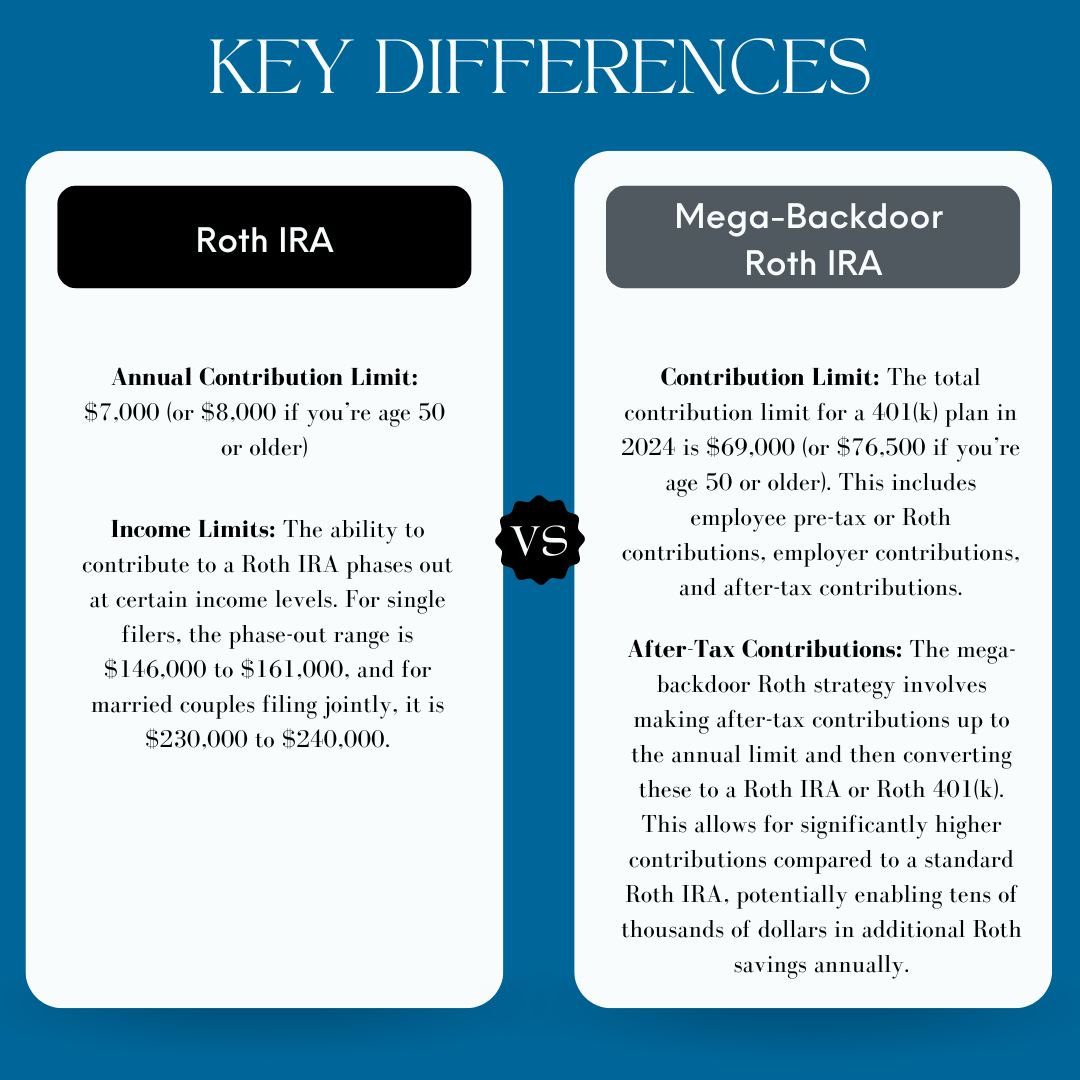

- Annual Contribution Limit: $7,000 (or $8,000 if you’re age 50 or older)

- Income Limits: The ability to contribute to a Roth IRA phases out at certain income levels. For single filers, the phase-out range is $146,000 to $161,000, and for married couples filing jointly, it is $230,000 to $240,000.

A mega-backdoor Roth IRA, on the other hand, is a strategy that allows individuals to make much larger Roth contributions through their employer’s 401(k) plan. This involves making after-tax contributions to a 401(k) and then converting those contributions to a Roth IRA or Roth 401(k), bypassing the standard contribution and income limits associated with a traditional Roth IRA:

- Contribution Limit: The total contribution limit for a 401(k) plan in 2024 is $69,000 (or $76,500 if you’re age 50 or older). This includes employee pre-tax or Roth contributions, employer contributions, and after-tax contributions.

- After-Tax Contributions: The mega-backdoor Roth strategy involves making after-tax contributions up to the annual limit and then converting these to a Roth IRA or Roth 401(k). This allows for significantly higher contributions compared to a standard Roth IRA, potentially enabling tens of thousands of dollars in additional Roth savings annually.

Do You Actually Have a Mega-Backdoor Roth?

The first mistake many people make is not knowing even if they have access to the mega-backdoor feature. There are some key indicators that you should be aware of. To see if you have access to this feature, you’ll more than likely need to access your retirement plan’s portal.

Navigate to the “Contributions” tab and see if you are able to set up an “after-tax savings” rate. After-tax savings are different from the Roth contribution, although they are both made after taxes have been imposed on your pay.

If you don’t see the “after-tax savings” setting, your next best bet is to contact your retirement plan administrator. The plan administrator is the company where your 401k is being held. This could be Fidelity, Vanguard, Empower, Schwab, or similar providers, such as Human Interest or Sharebuilder 401k.

Finally, remember that whether you have the mega-backdoor Roth feature or not does not depend on your plan administrator. It entirely depends on your employer. Part of their decision includes meeting participation tests set by the IRS and the inclusion of benefits for employee retention.

If you don’t have the mega-backdoor Roth feature, it never hurts to let your voice be heard. So reach out to HR or leadership and request it.

Mistake #1: You May be Underestimating the Impact of a Mega-Backdoor Roth

When you place investments in a taxable portfolio, the benefit is that you can withdraw the contributions at any time.

I have now heard this statement one too many times: “I don’t want to have too much saved for my retirement.” In my 11-year career, I have never met a retired person who felt they had too much in their retirement accounts!

However, if you fear losing access to your money, let me explain just how powerful the mega-backdoor benefit is and the flexibility you can leverage.

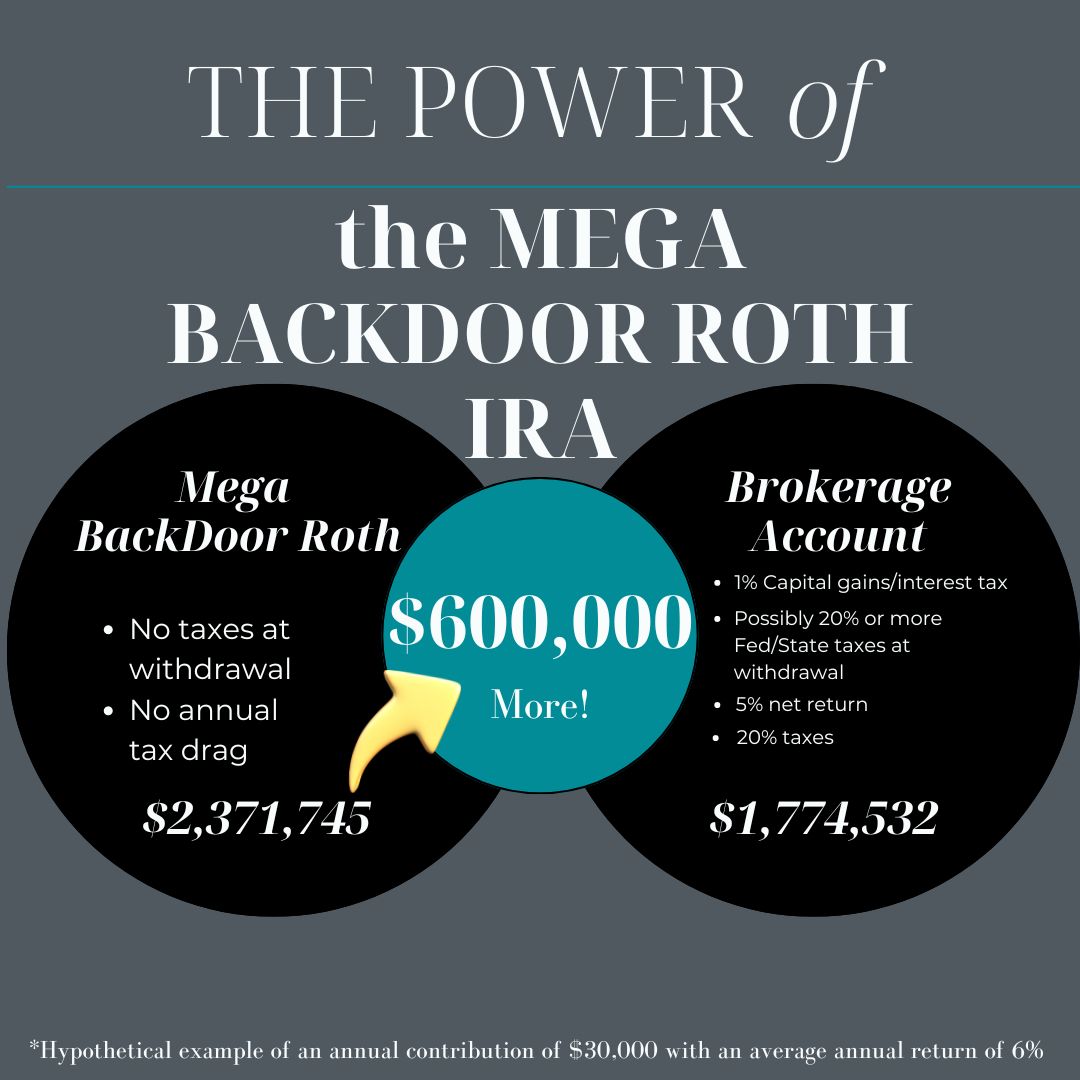

The tax benefit of investing money tax-free and being able to spend it tax-free is immense. For illustration purposes, let’s compare the difference between a brokerage account and a mega-backdoor Roth for saving purposes.

Let’s say you save $30,000 a year for 30 years with an average annual return of 6%. In a taxable brokerage account, you might pay a conservative 1% of your returns in capital gains and interest tax annually. Additionally, when you eventually withdraw your assets, you could pay another 20% or more in federal and state taxes.

Brokerage Account:

After 30 years, considering a 5% net return after taxes and another 20% tax upon withdrawal, you would end up with approximately $1,774,532.

Mega-Backdoor Roth:

Alternatively, with a mega-backdoor Roth IRA, which has no annual tax drag and no taxes upon distribution, you would accumulate about $2,371,745.

Even though these scenarios are all hypothetical, it shows that using this strategy would give you an extra $600,000 in your lifetime.

You can take out contributions at any time with no penalty. This means that over 30 years if you contribute $30,000 per year, you can have access to up to $900,000 with no concern of penalties or taxes. You just can’t pull out your growth until you are 59.5 years old.

This allows you a large pool of assets in case of emergencies or a desire to retire early.

Mistake #2: You Are Not Setting Up Your Contributions Correctly

The first step in creating a mega-backdoor Roth is the setup process, which can often be confusing

Remember that mega-backdoor Roth and Roth contributions are not the same.

- You will need to contribute to the “after-tax” portion of your 401k.

- Roth contributions are the same as pre-tax contributions: $23,000 as of 2024.

Mistake #3: You Are Not Completing the Conversion

The biggest mistake you can make when dealing with a mega-backdoor Roth is missing the conversion process. It’s critical to know that a mega-backdoor Roth strategy is not complete or effective until you complete the conversion.

A 401k can technically have three pools of money when you retire:

- Pre-Tax

- Roth

- After-Tax

Only a Roth IRA offers tax-free distributions. Pre-tax and after-tax contributions will both result in taxes on the growth, which is taxed as ordinary income.

It is very important that you complete the conversion process, otherwise, the growth from your mega-backdoor Roth strategy will eventually be taxed at ordinary income rates, which have historically been higher than capital gains rates, undermining its benefits.

To maximize the benefits, you must complete the conversion quickly to avoid taxes and the pro-rata rule. When setting up the mega-backdoor Roth, you’ll have several options:

- Some 401(k) plans allow you to check a box on your contribution screen to set up automatic conversions.

- You can call your 401(k) administrator and request them to set up automatic conversions.

- In some cases, such as with Empower, you might need to call each time you want to convert your after-tax contributions. Because calling in can be time-consuming, you might opt to do this once or twice a year. However, this could result in some taxes on the growth portion of your conversion.

As a CERTIFIED FINANCIAL PLANNER ® in San Francisco who works with tech professionals in the Bay Area, I’ve seen various clients use these options. Other options may be available, so be sure to check with your specific plan administrator.

Mistake #4: You Are Not Calculating the Impact of Your Match Correctly

The final mistake I see often as a San Francisco financial planner is that tech employees don’t calculate the after-tax contribution correctly. This usually happens to highly compensated employees who don’t understand how the employer match amount is calculated.

Many tech employers opt to match your retirement contributions. Your employer match is calculated up to a maximum income of $345,000 as per IRS rules, typically based on your base salary.

Here’s an example to help you calculate your contribution for a mega-backdoor Roth.

Suppose you are 45 years old (so the catch-up amount doesn’t apply), with a base salary of $400,000, and you receive a 50% match on the first 10% of your salary (a 5% match).

For 2024, your maximum pre-tax or Roth 401(k) contribution is $23,000. Your match is calculated as $345,000 * 5% (due to the IRS limit) = $17,250. The total allowable 401(k) contribution for 2024 is $69,000.

To calculate your after-tax contribution:

- Add your pre-tax/Roth contribution and your employer match: $23,000 + $17,250 = $40,250

- Subtract this total from the overall limit: $69,000 – $40,250 = $28,750

- Divide this number by your total salary to find the percentage for your after-tax contribution: $28,750 / $400,000 = 7.2%

So, you would enter 7.2% in your after-tax contribution entry field.

Lastly, remember that your backdoor Roth conversions are separate and do not count toward this total. If you are also doing backdoor Roth conversions and maxing your mega-backdoor Roth, these should be calculated separately.

Example of a Mega-Backdoor Process at Fidelity

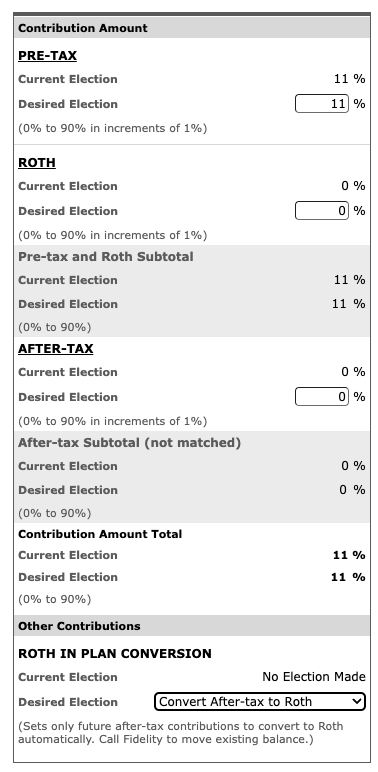

Lastly, I wanted to show you an example of the mega-backdoor Roth process at Fidelity:

Here, you can see the Fidelity contribution window. The pre-tax represents the regular 401k contribution, which provides a deduction on current taxes, and a Roth contribution, which allows you to distribute money tax-free.

If you are under the age of 50, these first two tabs accumulate to a maximum contribution of $23,000 in 2024.

The after-tax contribution window is the first step in the mega-backdoor Roth where the percent would be calculated net

of your regular contribution and your match.

Finally, at the bottom, you can see an in-plan conversion option. To finish this process, you need to elect to convert after-tax to Roth.

Unfortunately, every platform has a different conversion process that may not be as straightforward as this example above.

If you need assistance with a mega-backdoor Roth conversion, we invite you to connect with us using THIS link.

With over 15 years of experience, our team of CERTIFIED FINANCIAL PLANNERS ® has helped tech professionals in the Bay Area get the most out of their 401ks.

2024 Disclosures

RHS Financial is an SEC registered Investment Advisory Firm and distributes this presentation for informational purposes only. This presentation ( hitherto referred to as the presentation throughout this disclosure), blog post, infographic, slide deck or whatever form of informational modality the reader wishes to describe this as is provided for informational purposes only and should not be construed as investment advice in any way.

We believe the information, including that obtained from outside sources, to be correct, but we cannot and do not guarantee its accuracy in any way. RHS Financial uses information from outside sources to develop graphs, charts, infographics, etc. to enhance this presentation and while we believe the information from these outside sources, to be correct, we cannot and do not guarantee its accuracy in any way,

Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors who may be employees of but do not necessarily reflect the views of RHS Financial as a company. There can be no guarantee that developments will play out as forecasted. The information in this presentation is subject to change at any time without notice. This presentation contains “forward-looking statements" concerning activities, events or developments that RHS Financial expects or believes may occur in the future. These statements reflect assumptions and analyses made by RHS’s analysts and advisors based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond RHS Financials’ control, they are no guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements. In a nutshell; these are our best guesses and please don’t assume they are fact.

Mentions of specific securities, investment products, investment indices, companies or industries should not be considered a recommendation or solicitation. Data and analysis does not represent the actual or expected future performance of any investment or investment product Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This post may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with RHS Financial and does not sponsor, endorse or participate in the provision of any RHS’ services, or other financial products. Index information contained herein is derived from third parties and is proffered to you unaltered as we derived it from the third party.

RHS Financial, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where RHS Financial, LLC and its representatives are properly licensed or exempt from licensure. This presentation is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place.

If the client is deemed suitable and agrees, RHS may employ leveraged strategies for these clients. Leverage attained through margin on a client’s account can add additional risk. While RHS tends to seek to improve return with theses strategies by applying leverage to less risky indexes, there is no guarantee that that RHS will lower risk or improve returns.

RHS Financial. 4171 24th St. Suite 101 San Francisco, CA 94114