Understanding NQSO vs ISO: A Comprehensive Guide

Stock options are a common form of equity compensation that can meaningfully impact the future of your wealth. To make the most of them, you need to understand the subtle but important differences between ISO and NQSO.

The main difference between Non-Qualified Stock Options (NQSO) and Incentive Stock Options (ISO) is in how they are taxed. This difference can influence your choices significantly. On top of that, the concepts of leverage, time, and participating in potential gains while having some downside protection or exercise price add layers of complexity, making it feel like a double-edged sword.

Understanding the importance of timing is crucial for getting the most out of the tax treatment and leverage in NQSOs and ISOs.

As a San Francisco wealth management firm specializing in helping tech employees manage their wealth, we’ll use this blog to share some of the strategies and tips you can use to make the most of NQSOs and ISOs.

Leverage

One of the key benefits of stock options is leverage, which comes in two forms

- First, you have time to decide whether to invest actual money and participate in the gains. The longer you have to make this decision, the more leverage you have. ISOs and NQSOs typically give you ten years before they expire, giving you plenty of time to see how the stock price performs.

- Second, there’s the “unlimited” upside potential. When the gap between the market price and the exercise price is zero or very small, there’s a lot of untapped potential or leverage. As the stock price rises, this potential is realized, making the value of the stock options clearer and reducing the leverage.

Non-qualified stock options benefit the most from this leverage because exercising and holding them does not provide additional tax benefits. You can take full advantage of time to see where the stock price goes and decide when that potential is maximized.

Incentive stock options, on the other hand, are trickier. You want to use the leverage to see where the stock price goes, but the longer you wait, the bigger the gap gets, increasing the chance you’ll face the Alternative Minimum Tax (AMT) and other AMT-related issues.

If you want to make the most of your equity compensation, then use THIS link to set up a time to chat with us.

Simple taxes on NQSO and ISO

When you exercise Non-Qualified Stock Options (NQSO), the difference between the stock and exercise prices is treated as wage income, which means it’s subject to employment taxes, like FICA. NQSO taxes are withheld at 22% for any equity or bonus income under a million dollars, which is probably lower than your actual tax rate. So, saving some money for next year’s tax bill is a good idea. If you keep any shares after exercising, they’ll be taxed under regular capital gains rules.

ISOs are slightly more complex because there is a tangible tax benefit to holding them past exercise. First, when you exercise, you don’t pay ordinary income tax on the spread, unlike NQSOs. Then, if you hold the shares for one year after the grant and one year after the exercise, the difference between the exercise price and the market price will be considered long-term capital gains. Any gains you may or may not have after the exercise will also be counted as long-term capital gains. This benefit may be very tangible if you are in a high-income tax bracket.

Complex Taxes on ISO’s

ISOs might seem slightly more complex than NQSOs, but there’s a situation where complexity jumps. When you exercise ISOs, the untaxed spread between the market and exercise prices is considered a “preference item” for AMT. You might trigger AMT even though you don’t pay ordinary income taxes at exercise.

AMT is a prepayment of taxes that you should be able to recoup through AMT tax credits. However, there are many reasons this might not happen. The worst-case scenario is holding onto your stock for favorable tax treatment, and the stock price drops. This could leave you with a large tax bill, no way to pay it, and no hope of recovering the AMT tax.

A common mistake when filing for AMT credits is not considering the AMT Cost Basis adjustment, which is considered a negative AMT adjustment. This is the key to not getting double-taxed and getting the most out of the AMT Tax Credit. Here is a good article on AMT Credits and the AMT Cost basis adjustment.

Finally, remember that you can only own ISOs as an employee. If you leave your company, you will have 90 days to exercise ISOs, or they will convert to NQSOs per IRS rules. This pressure to exercise needs to be paired with a careful analysis of AMT.

To avoid scrambling at the last minute, continue reading below for ways to maximize your NQSO and ISOs.

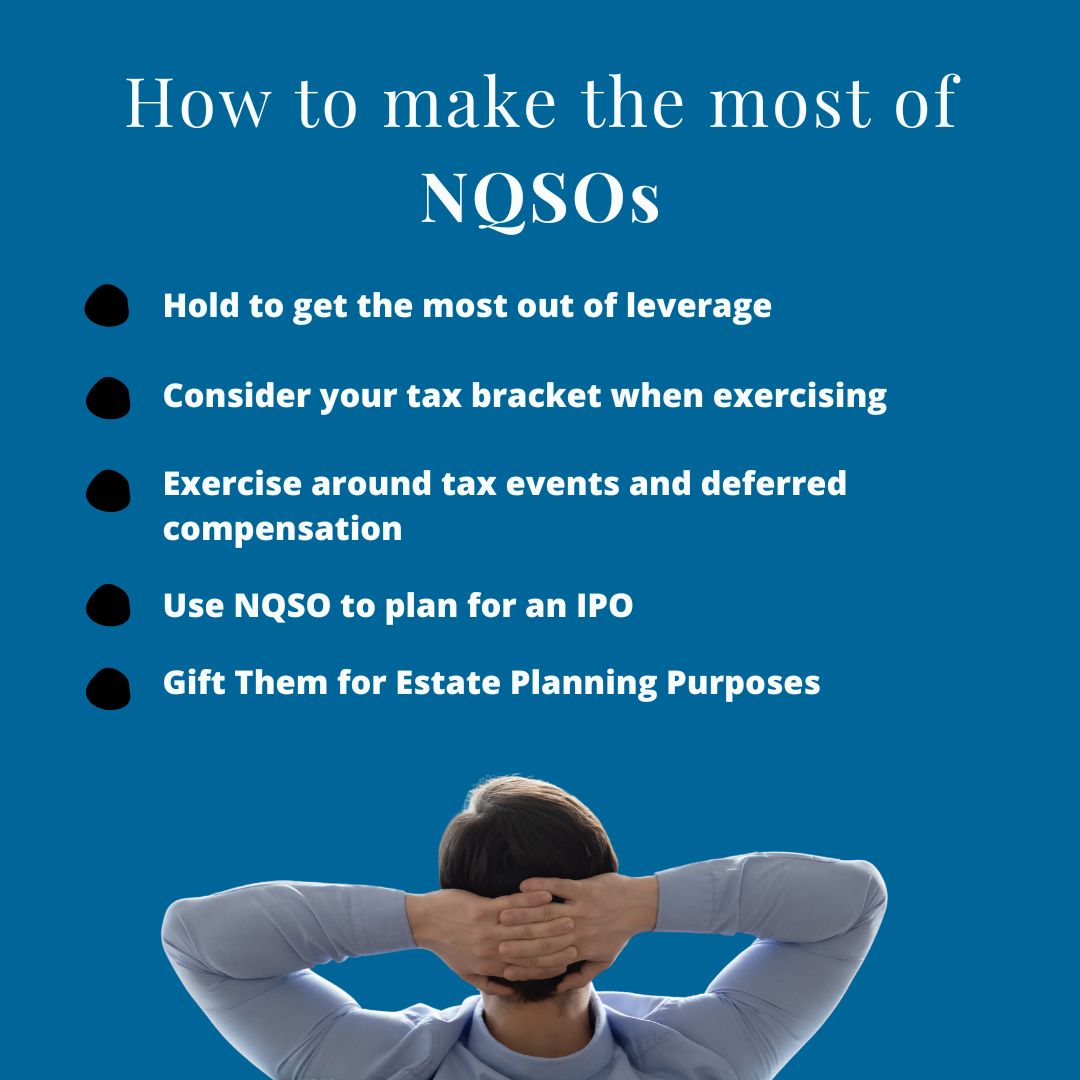

How to make the most of NQSOs

NQSOs are much more straightforward in terms of how they are taxed, so there are fewer decisions to make. Below are some of my favorite ways to maximize your non-qualified stock options:

- Hold to get the most out of leverage

As mentioned above, there are no benefits to holding your NQSOs post-exercise, and you don’t lose them if you leave your employer. You get the full benefit of the 10-year exercise window. The biggest advantage of non-qualified stock options is that you can wait and see how the stock performs without any capital committed or at risk. Make the most of this benefit, but remember to exercise them before they expire!

- Information Ratio AKA Spread vs. Time Left

The above advice comes with a caveat. Holding to the last minute isn’t necessarily the most intelligent way to approach NQSOs.

Stock options that are publicly traded are valued through the Black-Scholes method, a complicated formula to determine the price of the stock option. This pricing mechanism isn’t available when you are granted employer options. However, there is a ratio called the Information Ratio that certain tools provide that provides you insight into the “value” of your NQSO.

If you don’t have access to these tools, you only need to understand the balance between the spread and how much time is left. As the spread widens due to the stock’s appreciation and the time to expiration decreases, the information ratio becomes larger, and vice versa. The larger the information ratio, the better it is to exercise the options and sell the stock.

Keep this in mind: if your stock price is significantly above the exercise price and you are getting close to expiration, you are better off exercising and selling.

- Consider your tax bracket when exercising

One of the nice things about stock options is that you can choose when to recognize income. This means that if you have a good idea of your income, you can exercise enough to avoid jumping into another tax bracket.

- Exercise around tax events and deferred compensation

If you expect a lot of capital gains from selling ISO shares, existing stock, or property in one year, you might not want to exercise NQSOs since it could bump up your ordinary income tax rate. Consider any big bonuses, a one-year cliff on RSUs, or other significant income events you might have.

Conversely, if you have deferred compensation, you can always sign up to defer a large part of your income to exercise NQSOs at a lower tax rate.

- Use NQSO to plan for an IPO

If you are hired in anticipation of an IPO, you will likely be granted RSUs and, if you are lucky, some NQSOs. The biggest downside of RSUs during an IPO is that they will vest on the day of the IPO; however, due to a blackout period of six months, you are going on a wild roller coaster ride. In this period, the stock price can decrease significantly. If your tax bill is marked at the IPO higher price but your ability to sell and pay taxes doesn’t occur until six months at a much lower price, you can be put in a challenging spot.

However, with NQSOs, you control when your taxes are recognized and when you sell to pay those taxes. So, if you are evaluating what to exercise, sell, and when, consider holding on to your NQSOs if you anticipate an IPO.

- Gift Them for Estate Planning Purposes

NQSOs make a powerful estate transfer tool. If you are an executive, an early employee, or a founder, and your net worth is going to be significant in your lifetime, then this may be one of the best ways to reduce your estate taxes for two reasons:

- When you transfer NQSOs, you’re still responsible for the tax bill, even if someone else exercises them. This might not sound great, but it helps maximize the money leaving your estate. You could exercise the options and pay the taxes before transferring the shares, but your beneficiary has less money. Instead, they get the full value of the NQSOs if you pay the taxes when they exercise them.

- Second, gifting NQSOs before they even vest can allow you to significantly discount the value due to the risk that they may never vest. This makes NQSOs an effective estate planning tool.

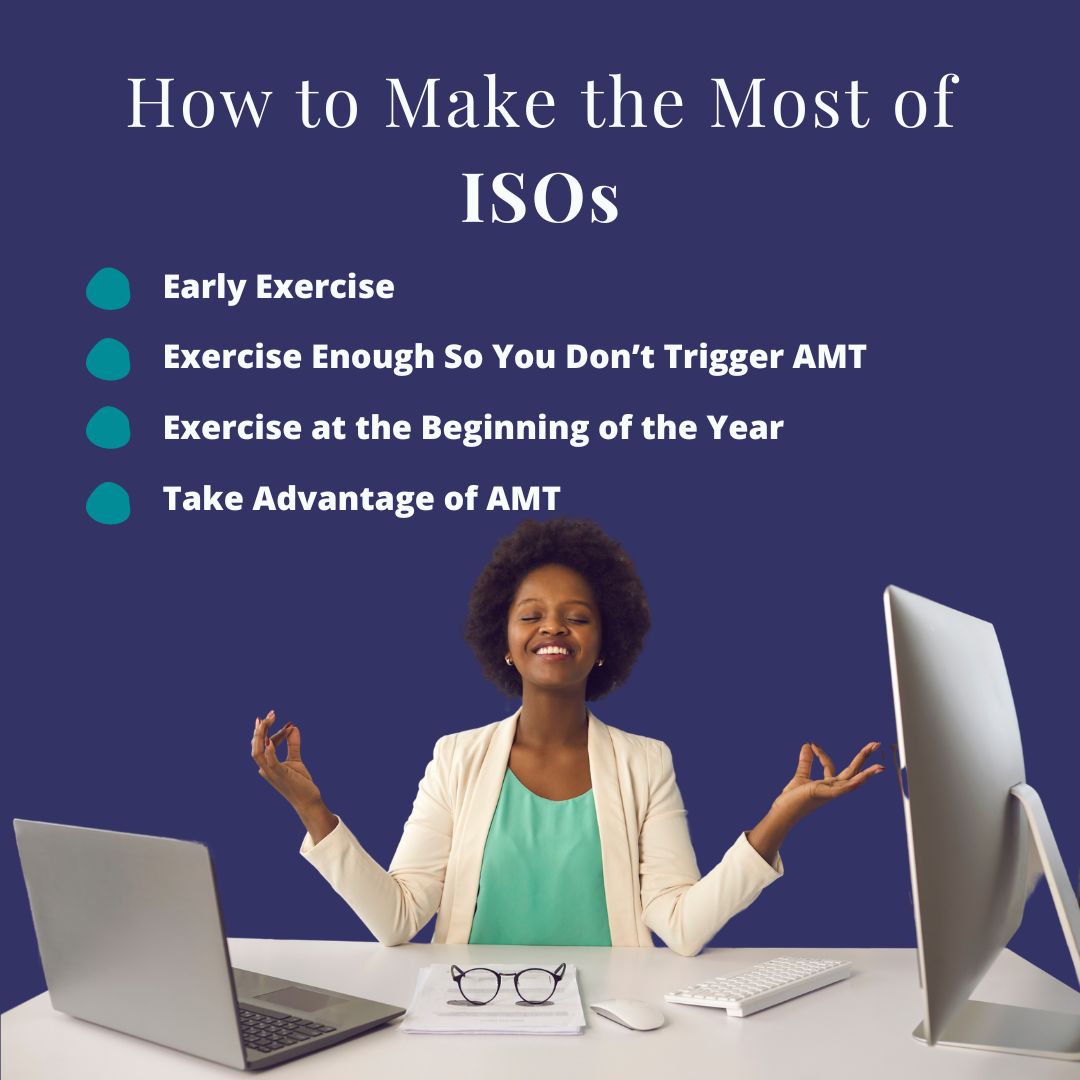

How to Make the Most of ISOs

Due to their complex tax rules, Incentive Stock Option strategies are much more complicated and hotly debated than NQSOs. There are many strategies; I will share just a fraction of what is possible here.

If you want to evaluate your situation, learn how to capitalize on your ISOs, navigate the ISO tax treatment, then schedule a free consultation with us using THIS link,

- Early Exercise

An early exercise is the golden strategy for ISOs. It allows you to exercise the shares in advance of their vesting. This means you can start the capital gains treatment clock while the spread between the exercise and market prices is low, thus avoiding AMT.

However, this strips the ISOs of the inherent leverage they provide to wait and see. And it is no better than “buying” the stock outright. Furthermore, you are tying up capital that potentially will never pay out. You need to be thoughtful of your entire financial situation before following through.

Not all is lost, though. Your company will repay your exercise price if you leave before your exercised shares vest.

- Exercise Enough So You Don’t Trigger AMT

A second best to an early exercise is figuring out exactly how much you can exercise without recognizing AMT. This requires estimating your tax bill and how much you can exercise before triggering AMT. This is not a simple calculation, and neither is it exact. Your best chance is to complete this analysis closer to the end of the year once you better understand what income will look like.

You could run two tax filings through Turbo Tax, work with your tax advisor, or speak to your San Francisco financial advisor. We have a couple of tools that we can use to make these estimates for our clients.

Once you know how much your “preference item for AMT,” your spread, can be before AMT is triggered, you can calculate the number of options to exercise. Do this yearly, and you will slowly accumulate shares that benefit from the long-term capital gains treatment.

However, if you do this years after your grant and the spread is very large, it can barely make a dent before your options expire.

- Exercise at the Beginning of the Year

Unlike the prior advice, another option is to exercise at the beginning of the year. If you exercise in January, you will receive a couple of benefits:

- First, if your stock is publicly traded, you can see if it appreciates by the end of the year. If it drops in value, you may sell it before December 31st to create a disqualified disposition but eliminate any chance of AMT.

- Second, if things go according to plan, you can sell the shares in January of the following year, recognize long-term capital gains, have enough money to pay AMT, and hopefully trigger the negative AMT adjustment for the following year to use the AMT credit.

- Take Advantage of AMT

If you’re going to trigger AMT, make the most of it. Since AMT happens when there’s a difference between Alternative and Ordinary tax regimes, it could be a good time to recognize some ordinary income taxes. A smart move might be to exercise some NQSOs without incurring extra taxes. Similar to deciding how many ISOs to exercise, you should use tax software or talk to your tax advisor to get a clear estimate of how much ordinary income you can recognize.

Summary

There are tangible differences between NQSOs and ISOs that need to be considered when trying to maximize both. The differences have everything to do with the ISO and NQSO tax treatment. Understanding how taxes work here and how they apply to your unique situation is the science. Making decisions based on your expectations and comfort with risk is the art.

If you need help with your ISOs, NQSOs, or any other form of equity compensation, please use THIS link to reach out to us.

2024 Disclosures

RHS Financial is an SEC registered Investment Advisory Firm and distributes this presentation for informational purposes only. This presentation ( hitherto referred to as the presentation throughout this disclosure), blog post, infographic, slide deck or whatever form of informational modality the reader wishes to describe this as is provided for informational purposes only and should not be construed as investment advice in any way.

We believe the information, including that obtained from outside sources, to be correct, but we cannot and do not guarantee its accuracy in any way. RHS Financial uses information from outside sources to develop graphs, charts, infographics, etc. to enhance this presentation and while we believe the information from these outside sources, to be correct, we cannot and do not guarantee its accuracy in any way,

Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors who may be employees of but do not necessarily reflect the views of RHS Financial as a company. There can be no guarantee that developments will play out as forecasted. The information in this presentation is subject to change at any time without notice. This presentation contains “forward-looking statements" concerning activities, events or developments that RHS Financial expects or believes may occur in the future. These statements reflect assumptions and analyses made by RHS’s analysts and advisors based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond RHS Financials’ control, they are no guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements. In a nutshell; these are our best guesses and please don’t assume they are fact.

Mentions of specific securities, investment products, investment indices, companies or industries should not be considered a recommendation or solicitation. Data and analysis does not represent the actual or expected future performance of any investment or investment product Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This post may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with RHS Financial and does not sponsor, endorse or participate in the provision of any RHS’ services, or other financial products. Index information contained herein is derived from third parties and is proffered to you unaltered as we derived it from the third party.

RHS Financial, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where RHS Financial, LLC and its representatives are properly licensed or exempt from licensure. This presentation is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place.

If the client is deemed suitable and agrees, RHS may employ leveraged strategies for these clients. Leverage attained through margin on a client’s account can add additional risk. While RHS tends to seek to improve return with theses strategies by applying leverage to less risky indexes, there is no guarantee that that RHS will lower risk or improve returns.

RHS Financial. 4171 24th St. Suite 101 San Francisco, CA 94114