Dual Citizenship: Pros/Cons, How, Investments

Dual citizenship or owning multiple passports is not just for international spies. It has become a popular financial goal for many of the wealthy and the ultra-wealthy. Tech billionaires like Peter Thiel and former Google CEO, Eric Schmidt, are amongst those securing something called a citizenship by investment.

A citizenship by investment is a much bigger flex than a fancy sports car or a nice Rolex. Why, because it also has many legitimate appeals to it, including geopolitical diversification, connection to your heritage, amongst many other reasons we will outline here.

If you are worried about political elections or the current living environment in the US, you are not alone. According to a law firm, Henley & Partners, American’s outnumber every nationality when it comes to securing a second citizenship.

With top destinations offering citizenship by investment like Portugal, Malta, Greece, and Italy you may be wondering what it takes to secure a second passport.

In this article, we will cover the pros and cons of dual citizenship, how the process of getting a golden visa, residency, and eventual citizenship works, and what some of your investment options may be.

In this article we will mention Pela Terra. An investment firm that is making access to Portuguese golden visa in a straightforward manner and providing an investment option that can be a great alternative to investing in real estate. We are not here to qualify the “returns” of an investment like this, and our fiduciary status precludes us from getting any kickbacks, but when we come across something unique like this, we just can’t help but write about it. We are not endorsing this firm or its investment opportunity, but if you are interested in learning more about getting a golden visa, they may be a resource for you.

Pros of Dual Citizenship

Dual citizenship benefits are varied. Some are very tangible, and some are subjective. Before you start wondering how to get dual citizenship it is important to consider why you would even want it.

- Sense of security: The big motivator for most is an insurance against political instability. This is the stated driver behind Peter Thiel’s and Eric Schmidt’s investment into dual citizenship. For some this feels like less of a luxury and more of a lifesaver. The ability to leave and go as political environments change, or natural disasters occur, or even potentially markets crashing is the peace of mind many are looking for.

- Flexibility to come and go: Dual citizenship provides you travel freedom and, in some cases, allows you to avoid visas. In the case of increasing global tension and the challenge of being welcome abroad, a second passport provides additional flexibility.

- Ability to work abroad: The flexibility of a golden visa, and eventual dual citizenship, is unmatched for those looking to work abroad. Allowing you to avoid dealing with expiring work permits.

- Ability to start a business: If you are entrepreneurial in nature, then a dual citizenship can provide you the access to international markets. In the EU, you receive access to the Schengen Area and the 27 European countries that are part of it.

- Allows you to retire in another country: You will be able to plant your retirement roots in the country of your choice. Stay as long as you like, rather than navigate visa restrictions that are time based.

- Right to own property: A dual citizenship, allows you to buy a home in any of the 27 countries that make up the EU.

- Ability to vote: If you are going to retire, work, or start a business in another country you may want to have your voice heard.

- Access to education and healthcare: In EU countries, you will have access to often superior and lower cost, if not free, healthcare and their educational systems.

- Cheaper cost of living: If you live on the West or East Coast, then the cheaper cost of living overseas may be the selling point. Portugal, for example is considered one of the cheapest western European countries to live in.

- Citizenship for your loved ones: Most citizenship by investment programs offer citizenship to your children and other dependents.

- Cultural education: Traveling and living somewhere are completely different experiences. The best way to embrace another culture is to live there. You haven’t really experienced local culture until you are taking public transportation and shopping for groceries!

Cons of Dual Citizenship

A citizenship by investment and dual citizenship isn’t all upside. There are tangible downsides and common misunderstanding that needs to be addressed:

- Does not provide tax benefits: If you live on either of the coasts then it is likely you are in a high tax bracket. Frustration with the US tax code can leave you searching for alternatives. Unfortunately, a dual citizenship is not the answer you think it may be. United States taxes on global income. Irrelevant of the tax code and rate that you may pay overseas. If you pay more taxes in your second country, then you may receive tax deductions/credits in the US but only up to the amount that you would have originally paid as a US tax payer. And not always. US has tax treaties but with only certain countries. And if you think you can ditch your US tax residency, think again. There is an exit tax. Finally, a dual citizenship will require you to have two tax filings, and your US tax filing and reporting requirements are going to be more complicated.

- Problem with legacy planning: If you are wealthy and intend to leave a large amount of wealth to your heirs you will need to be very careful about which country you choose for dual citizenship. In some countries such as England, the inheritance tax starts at very low dollar amounts and is based on your global assets. Other countries don’t recognize trusts, making your estate planning wishes harder to execute. However, there are countries out there, like Portugal that have a 0% inheritance tax, allowing you to take full advantage of the US estate tax code with large exemptions.

- Duty to fulfill military obligation: Some countries require you to fulfill military obligations. This may be a bigger issue for your children than you.

- Barrier to some US jobs: US jobs that require government security clearance may prohibit you from holding dual citizenship.

- Can be “expensive”: Technically speaking, a citizenship by investment program should be just that, an investment. However, depending on the country of choice, these investment options can feel nothing more than an expense. That is why in countries like Portugal, with access to funds such as Pela Terra, that provide a properly structured investment option, makes a big difference in the full benefit a dual citizenship can provide.

How to get Dual Citizenship

The question of how to get dual citizenship will be answer very differently depending on which country you select. We will share with you the basic outline of citizenship by investment programs and share with you what we believe to be the easiest country to get citizenship in Europe.

A citizenship by investment does not automatically get you a second passport or a dual citizenship. It allows you to establish residency in the country, provides for a golden visa, and starts the process towards getting dual citizenship.

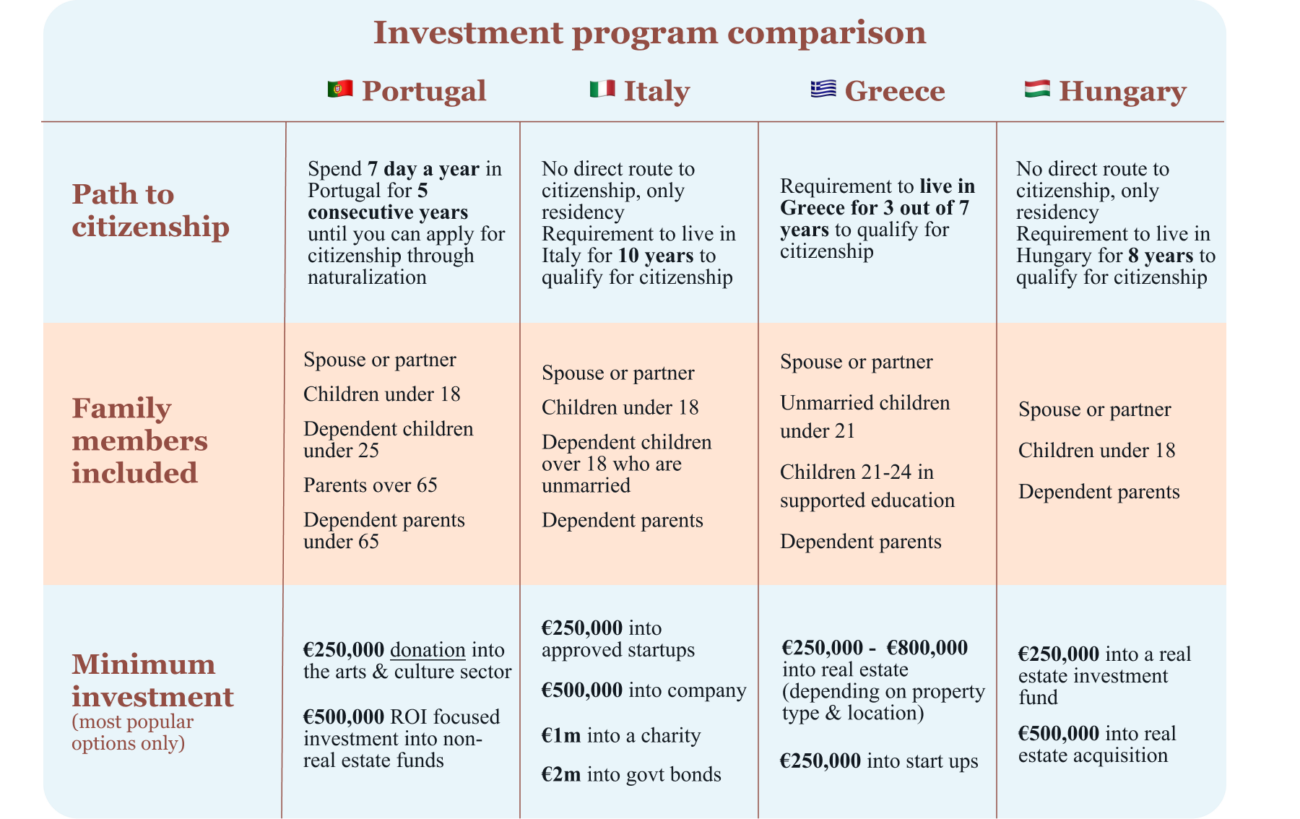

In almost every case, you will need to live in your country of choice and prove residency. As an example, Malta requires you to live there anywhere from 12 to 36 months. Other countries, like Portugal, allow you to visit once every two years for 14 days.

Before you can establish residency, you need to make an investment. The investment will depend, once again, on the country of choice. In some countries you will need to make an additional donation and prove your family’s good health.

You will also be subject to due diligence of varying degree. Including criminal and background checks.

In every case, there are many steps, which include forms, filing deadlines and timelines, applications, and other administrative fees.

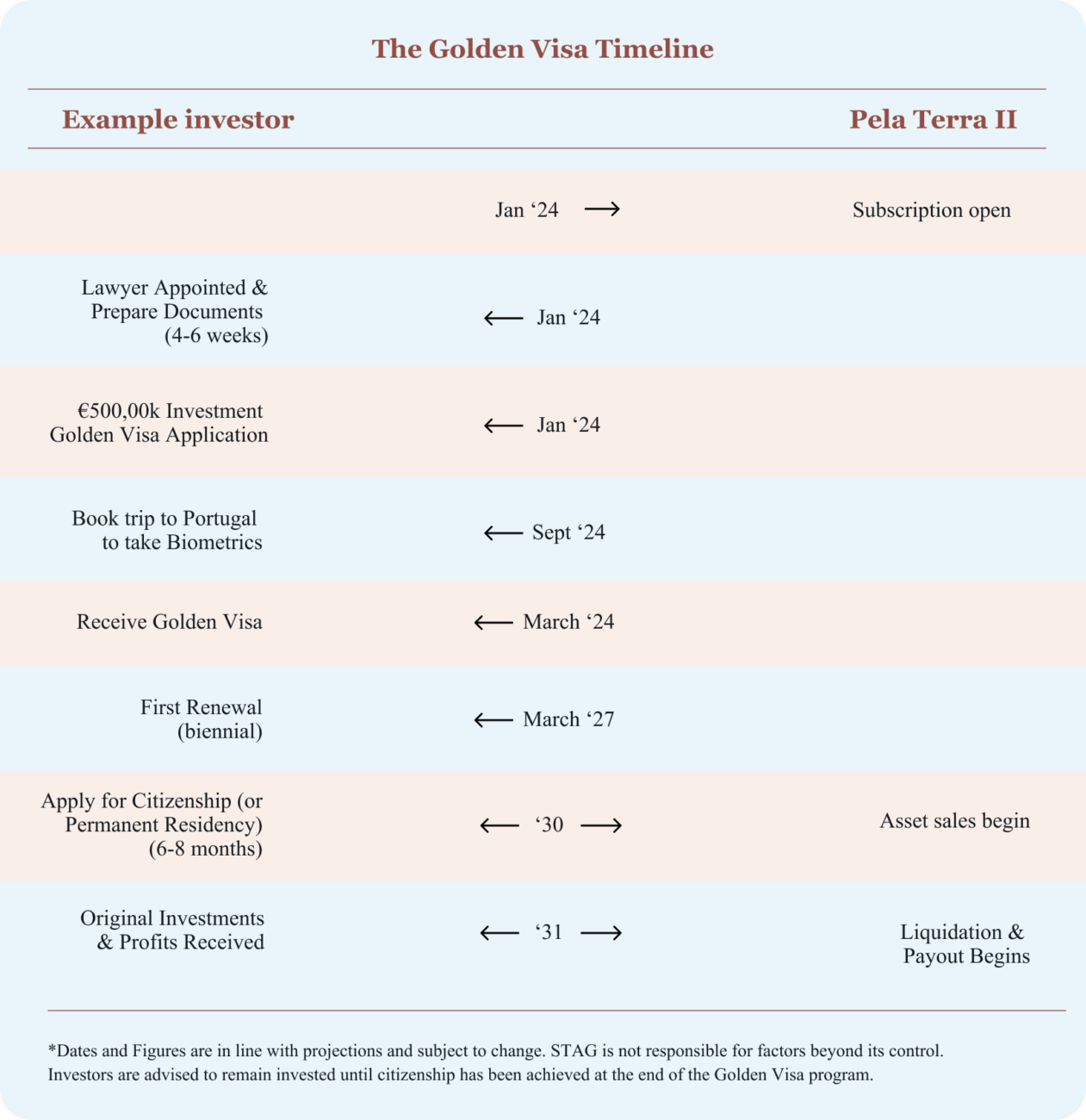

Based on different sources, a conservative timeline is about 6 months between the time you make an investment in the country and the time you receive residence.

Finally, after meeting the residency requirements for multiple years you can apply for a dual citizenship and your golden passport. This citizenship application can also be complex and vary. In cases such as Portugal it may require a basic language proficiency test.

Of all the countries we researched, it seems that Portugal may have the easiest residency requirement. Investment funds like Pela Terra make the residency and investment criterion relatively easy to meet. Portugal ranks as 3rd in Global Peace Index, due to its low crime rate and welcoming citizens, making it one of the most desirable passports and citizenships to attain.

With Pela Terra, you are expected to receive a golden visa within a year of investing, and ability to apply for a passport in 5 years. In that time frame you have the right to live and work in Portugal, and access to EU countries, as well as free health care and education in Portugal. Once you receive your dual citizenship those rights transfer to all EU countries.

Investment Options

Economic citizenship or citizenship by investment isn’t the same everywhere you go. The investment amount, the investment itself, and any additional requirements and costs vary greatly. As an example, Portugal’s citizenship by investment provides for flexibility and some restrictions you wouldn’t find in countries like Malta.

Typically, real estate is the first investment that comes to mind for many when they think of citizenship by investment. However, countries like Portugal are eliminating this as an option due to the negative effects it has had on the local populace. However, even if you could invest in real estate, it’s not always the best investment option. In the best-case scenario, you can play international landlord, trying to make this purchase into an actual investment. In the worst-case scenario, it sits there, accumulating dust and requiring upkeep.

The investment amounts can vary, anywhere from $250,000 in some Caribbean countries, to $500,000 euros in Portugal, to several million dollars in countries like New Zealand. As an example, Malta requires a $600,000 euro investment if you are willing to maintain residency for 36 months and $750,000 for a lower 12 month residency requirement.

Portugal is one of the few countries, that provides a flexible approach. You can invest in a fund, start a business and create 10 jobs, you can invest $500,000 euros in scientific research, or a $200,000 donation to artistic production or restoration of cultural heritage sites.

With such variety in investment sizes and types between countries, Portugal seems to make it more simple and straightforward with investment options that genuinely feel like investments.

If you are interested in exploring more about Portugal’s citizenship by investment through a fund like Pela Terra you can read their brochure HERE. Pela Terra’s fund is due to close 2025 and will be their last golden visa fund. This fund and the program can close sooner depending on the Portuguese government.

Extra Disclosures… we are not qualifying the investment quality, potential returns, tax ramifications, or risk of Pela Terra or agricultural investments. As a self-directed investor you should do your own due diligence. International investing, investing in private funds, and alternative assets like agriculture carry their own risk. We are not compensated and do not have any financial incentives for highlighting a fund like Pela Terra.

2024 Disclosures

RHS Financial is an SEC registered Investment Advisory Firm and distributes this presentation for informational purposes only. This presentation ( hitherto referred to as the presentation throughout this disclosure), blog post, infographic, slide deck or whatever form of informational modality the reader wishes to describe this as is provided for informational purposes only and should not be construed as investment advice in any way.

We believe the information, including that obtained from outside sources, to be correct, but we cannot and do not guarantee its accuracy in any way. RHS Financial uses information from outside sources to develop graphs, charts, infographics, etc. to enhance this presentation and while we believe the information from these outside sources, to be correct, we cannot and do not guarantee its accuracy in any way,

Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors who may be employees of but do not necessarily reflect the views of RHS Financial as a company. There can be no guarantee that developments will play out as forecasted. The information in this presentation is subject to change at any time without notice. This presentation contains “forward-looking statements" concerning activities, events or developments that RHS Financial expects or believes may occur in the future. These statements reflect assumptions and analyses made by RHS’s analysts and advisors based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond RHS Financials’ control, they are no guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements. In a nutshell; these are our best guesses and please don’t assume they are fact.

Mentions of specific securities, investment products, investment indices, companies or industries should not be considered a recommendation or solicitation. Data and analysis does not represent the actual or expected future performance of any investment or investment product Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This post may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with RHS Financial and does not sponsor, endorse or participate in the provision of any RHS’ services, or other financial products. Index information contained herein is derived from third parties and is proffered to you unaltered as we derived it from the third party.

RHS Financial, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where RHS Financial, LLC and its representatives are properly licensed or exempt from licensure. This presentation is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place.

If the client is deemed suitable and agrees, RHS may employ leveraged strategies for these clients. Leverage attained through margin on a client’s account can add additional risk. While RHS tends to seek to improve return with theses strategies by applying leverage to less risky indexes, there is no guarantee that that RHS will lower risk or improve returns.

RHS Financial. 4171 24th St. Suite 101 San Francisco, CA 94114