The Fossil Fuel Industry Will Probably Collapse This Decade

It’s 2020! We’re officially living in the future! And if retro sci-fi stories are any guide, that means abundant, clean, cheap energy for everyone. In 1954 the chairman of the US Atomic Energy Commission declared to great fanfare that the nuclear age would bring with it “electrical energy too cheap to meter”, ushering in a wave of techno-optimism for the post-war era. Unfortunately, the atomic energy revolution never really panned out, and by the 1970s everyone seemed to resign themselves to the fact that fossil fuels were an inescapable aspect of our modern economy, an attitude that has stuck with us ever since. But times are finally changing; 70 years after we first dreamed of powering our society with the limitless energy of the sun, we are now finally on the eve of achieving it. The 2020s will be the decade of the Great Energy Transition, and the end of fossil fuels as we know it. This transition will bring with it momentous changes to financial markets, the economy, our politics, and our quality of life. It’s going to be a lot of fun to watch.

Just a little less than three years ago, I wrote on this blog that we may be on the verge of a permanent bear market in fossil fuels. In it I predicted that the recent financial woes in the coal, oil, and gas industries would likely only continue as the costs of switching to renewable energy were becoming exponentially more economical – not an especially common view among financial market professionals at the time, I might add. But even I have been surprised by how dramatic the changes have been since writing that in 2017. Let’s start our review of the last three years with my most basic claim: has the fossil fuel industry continued to lose ground in the financial markets?

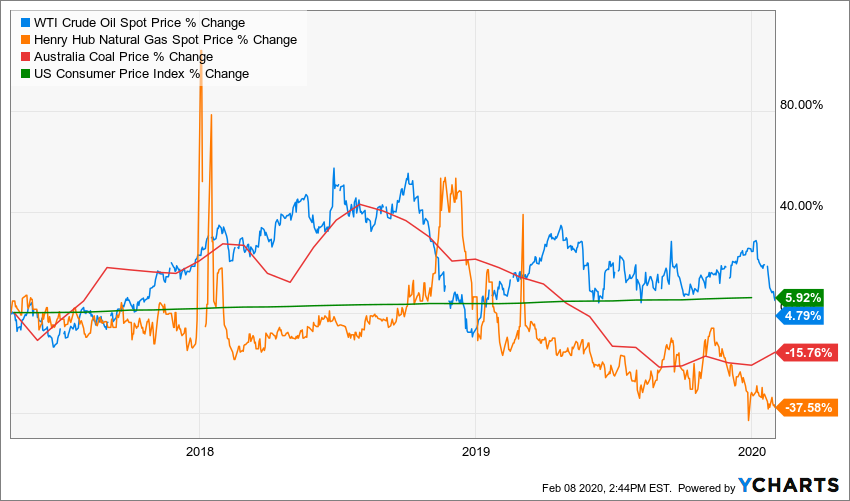

Yes. Below I plot the benchmark prices for oil, natural gas, and coal compared to general price inflation from the date I published my last article through the end of January 2020.

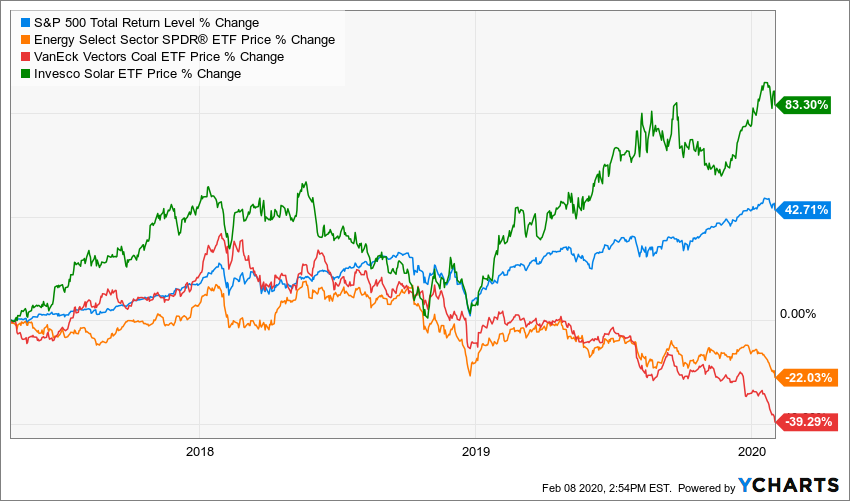

Though highly volatile as always, the price of crude oil has failed to keep up with inflation over the past three years. Natural gas and coal prices have fallen in absolute terms. Lower fuel prices could also just be a matter of more efficient extraction, however, so how are the actual producers of these commodities doing? Next, I plot the performance of the S&P 500 over the same period vs. that of the oil & gas industry (as proxied by the SPDR ETF XLE) and the coal industry (as proxied by the Van Eck ETF KOL), as well as the performance of their clean energy competition, the solar industry (as proxied by the Invesco ETF TAN).

While the aggregate stock market has continued its decade-plus long bull market mostly unabated over this period, investors in traditional energy resources have lost money – a lot of money. Meanwhile, the solar energy industry (and the clean energy industry in general) has continued to gain ground, delivering outsized returns to investors.

What’s driving these market dynamics? Three major forces are at play right now in the energy market: the accelerating improvements in renewable energy efficiency, the move towards sustainability among institutional investors, and the adoption of public policies aimed at mitigating climate change and other environmental concerns. These forces are now mutually reinforcing and will work to shift our society away from fossil fuels and towards clean energy this decade, probably much faster than almost anybody is anticipating.

If you want to learn how to take advantage of these trends in your portfolio schedule a call with us HERE.

Renewable Revolution

For decades, the cost effectiveness of solar power (and to a lesser extent, wind power) technology has been increasing exponentially. For years this was of mostly academic interest as renewable sources were still far more expensive than conventional fossil fuel energy sources. But in recent years costs have fallen to the point where they are now often lower than power from coal or gas-fired plants and falling further still. In my 2017 article I pointed to news from September 2016 in which Abu Dhabi ditched plans to build a gas-fired electric power plant and instead built a solar power plant that would deliver electricity at a world-record low price of 2.42 cents per kilowatt-hour, about half what they estimated natural gas would have cost them. Not to be outdone by their UAE neighbor, last October Dubai announced they were building a new world-record breaking solar power plant that will deliver electricity at just 1.7 cents per kilowatt-hour, a 30% cost reduction in three years.

They won’t hold the record for long. Every few weeks now news is coming out of some new solar installation passing regional or worldwide cost-cutting milestones. Closer to home, Los Angeles’ utility commission recently approved a new solar plant that will deliver 300 megawatts of energy at 3.962¢/kWh (by comparison, electric power from natural gas usually costs about 8¢/kWh in the US). Importantly, that price tag includes energy storage as well, meaning the plant will be able to deliver energy to LA residents day and night. This solution overcomes one of the last remaining obstacles to switching to renewable energy: reliability. The sun doesn’t always shine and the wind doesn’t always blow, but if the combined cost of generation and storage is cheap enough, that doesn’t matter, renewables will be able to undercut fossil fuels any time of the day or year.

Unsurprisingly, as renewables get cheaper, people buy more of them. In 2000, wind and solar energy together accounted for a negligible 32 Terawatt-hours of global energy production. In 2018 that had grown to 1,854 TWh, a 56-fold increase in 19 years. Over that period, wind energy production grew at an annual rate of 22.8% per year. Solar was 41.5% per year. Of course, that’s still just a tiny sliver of overall energy production.

As of 2018, solar and wind energy only account for 3% of global energy, with fossil fuels contributing over 84%, which is probably why most people don’t perceive the future of fossil fuels as changing very much and worry about the potentially devastating environmental consequences that may imply. But that 3% is a nearly ten-fold increase in the slice of the pie compared a decade before. Renewable energy today looks a lot like the internet did around 1995: an interesting curiosity but surely nothing of great consequence, right? But if renewables keep gaining ground against fossil fuels at the same rate they have been so far this century, then by the end of the decade they will constitute nearly one third of our energy budget and fossil fuel usage will be declining in absolute terms and at an accelerating pace.

In fact, while we should always be cautious about projecting exponential trends into the indefinite future, I think this probably underestimates the amount of renewable energy penetration we’ll see by decade-end. So far, renewable energy has mostly been used for adding additional capacity to an electric grid. For this reason, most of the demand has actually come from the developing world, where demand for electricity is still rapidly increasing. But to really take a bite out of fossil fuels renewable power has to start replacing existing conventional power sources: coal and gas power stations and petroleum-powered transportation. This is what we’re starting to see take place.

As the cost of renewable energy falls lower and lower, it eventually makes economic sense to shut down a perfectly good coal-fired power plant and replace it with solar, or to scrap a perfectly good gas-powered car or truck and replace it with an electric one. We are just now approaching that tipping point. Last year, for example, PacifiCorp, a major electric power company operating in multiple western US states, announced that it would be closing 20 to 24 coal plants – some of them decades ahead of their scheduled retirement – and replacing them with 7 gigawatts of renewable energy capacity simply because it will save them money.

Speaking of money, let’s talk about the other major force at play in our impending energy revolution: institutional investors.

The Buck Stops Here

In my 2017 article I speculated that fossil fuel-related assets might be overvalued because the financial industry still seemed to be behaving as though we would just keep burning hydrocarbons at a steadily increasing pace forever and ever, which struck me as unlikely. Well apparently my blog is a lot more influential than I realized because the word is out, and the speed with which the financial industry has turned its back on conventional energy assets is stunning.

The financial industry’s efforts to decarbonize itself takes two forms: engagement and divestment. Engagement refers to efforts by financial actors to persuade or pressure the management of the companies they’re invested in to reduce their carbon footprint or otherwise adopt more environmentally friendly practices, often through their votes as shareholders. Engagement tries to use capital to change behavior. Divestment refers to the practice of selling holdings in carbon-intensive assets – primarily the coal and oil & gas industries – and refusing to make further investments, seeking to starve the targets of capital and force them out of the market.

In December 2017, Betty Yee, a board member of California’s public pension system CalPERS, launched Climate Action 100+, which has since become probably the largest and most ambitious investor engagement campaign ever created, whether climate-related or otherwise. The initiative was created as part of an of effort to coordinate institutional investors’ actions to “ensure the world’s largest corporate greenhouse gas emitters take necessary action on climate change” by “engaging companies to: curb emissions, improve governance and strengthen climate-related financial disclosures.” The initiative has since had over 370 institutional investors from around the world representing more than $35 trillion in assets under management sign up, including many of the biggest names in finance such as BlackRock, Fidelity, Invesco, PIMCO, UBS, Wells Fargo, and multiple public pensions, private foundations, and university endowments.

More than a vague declaration of PR-friendly platitudes, the Climate Action 100+ initiative has an extremely specific, action-oriented agenda to pressure major corporations into cleaning up their carbon footprint. The initiative created a list of 161 “focus companies” that together account for over 80% of global corporate greenhouse gas emissions to target their efforts towards. Many of these are the sort of oil & gas majors that you’d expect such as Exxon Mobil, BP, and Royal Dutch Shell, but they also include companies from transportation such as Ford, Toyota, and Boeing, consumer goods such as Nestle and Procter & Gamble, industrial goods manufacturers such as Dow and Caterpillar, and many others including 32 major electric utilities. For each industry, the initiative lays out a set of agenda items it wants its target companies to improve upon and a strategy for investors to get companies to comply, including by “voting for the removal of directors who have failed in their accountability of climate change risk.” In their first progress report published last year, Climate Action 100+ spells out their efforts and successes thus far as well as their agenda in the years to come in an extremely and data-driven manner, along with dozens of case studies of how institutional investors have successfully pressured companies to diversify into renewable energy sources, halt capital investment into carbon-intensive projects, commit to emissions-reduction targets (often with direct ties to remuneration), disclose in their financial statements their carbon footprint and climate risk exposure, and stop corporate lobbying efforts that work against the policy goals laid out in the Paris Agreement. The report is extremely informative and inspiring so I encourage interested investors to read it.

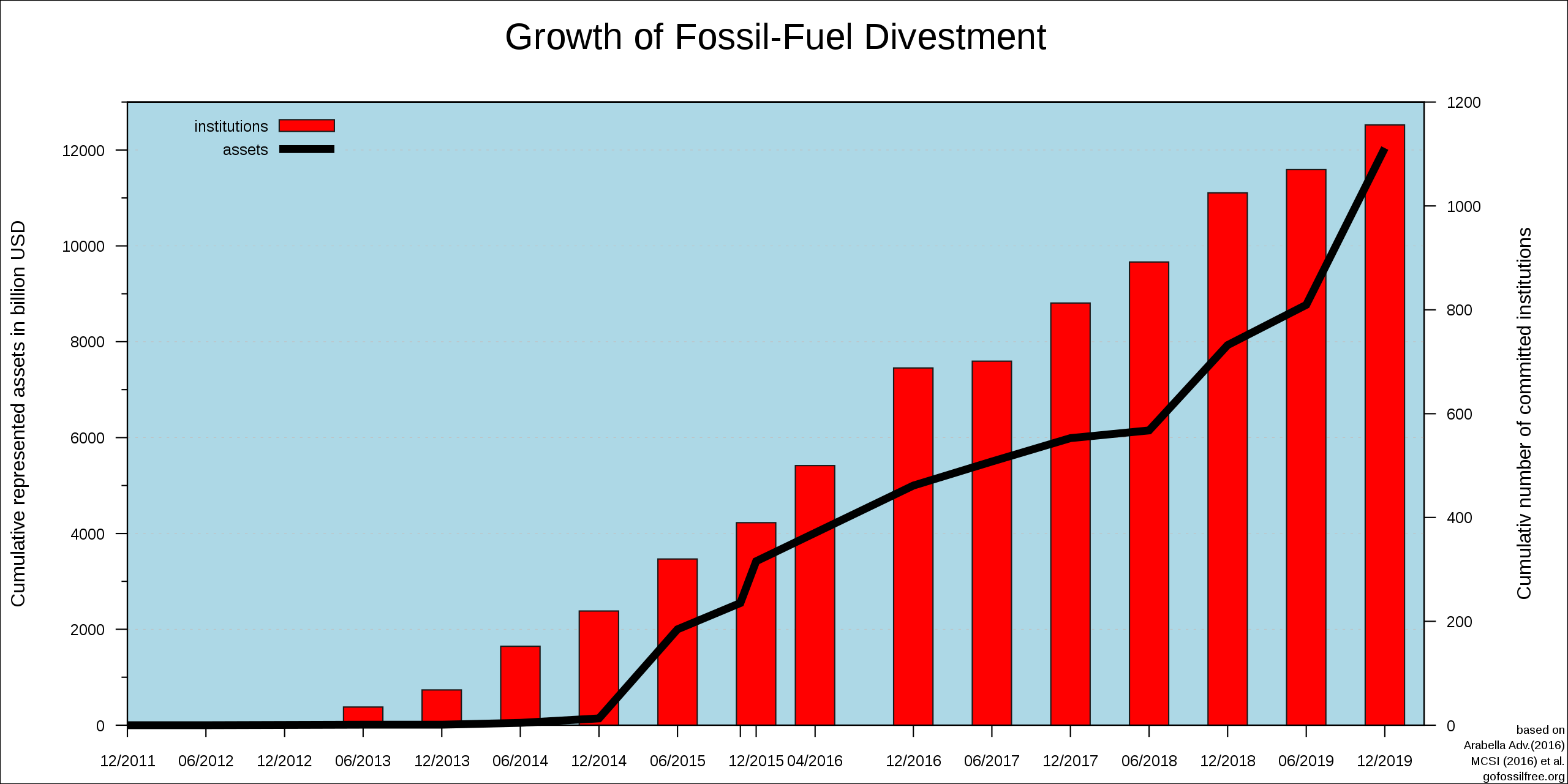

For some investors, engagement isn’t enough, they don’t want to support the fossil fuel industry with their capital at all. Fossil fuel divestment campaigns have rapidly accelerated since 2017. As of December 2019, over 1,200 institutions representing more than $12 trillion have divested from fossil fuels, according to Wikipedia.

Divestment scored its biggest win yet late last year with the announcement that Norway’s $1.1 trillion sovereign wealth fund will divest from oil & gas exploration & production companies. This news was of particular import not just because of the size of the Norwegian sovereign wealth fund, but due to the fact that Norway earned so much of its wealth due to its abundant oil reserves. Even those investors directly involved with fossil fuels are beginning to turn on them.

This situation is getting to the point where it might be creating a runaway feedback loop, a “run on the bank” on fossil fuel assets where even investors who don’t give a damn about the environment or climate change shun coal, oil, and gas companies because everybody else is. Enter Jim Cramer, the (in)famous host of CNBC’s Mad Money, who just a couple of weeks ago declared there’s no more money to be made in oil and gas stocks. Cramer made my above point very explicitly: “I am not here, though, to take political stands. My job is to help you try to make money. And the honest truth is I don’t think I can help you make money in the oil and gas stocks anymore… I’m done with fossil fuels … they’re just done. You’re seeing divestiture by a lot of different funds. It’s going to be a parade.” (Note that like most fiduciary financial advisors I think that Jim Cramer generally gives terrible advice, but I’m happy to still quote him when he makes my arguments for me.)

And sustainable investing is increasingly no longer just the purview of institutional investors. Investor action with respect to fossil fuels is itself part of a broader movement towards what has come to be called ESG investing (Environmental, Social, and Governance), which strives to align the interests of corporate management with those of the broader market, society, and the environment. ESG investing has exploded in popularity in recent years, and is now easily accessible to individual investors. In my next post I will give a practical rundown of the ESG investing landscape and how investors should think about sustainable and socially responsible investing decisions.

So fossil fuel companies are facing stiff competition from renewable energy technologies whose prices are falling exponentially, meanwhile their investors are either abandoning them or demanding they stop spending money on capital expenditures to maintain or expand their infrastructure, let’s turn to the third force pushing the conventional energy sector towards the edge of the cliff: governments.

Carbon Tax Man

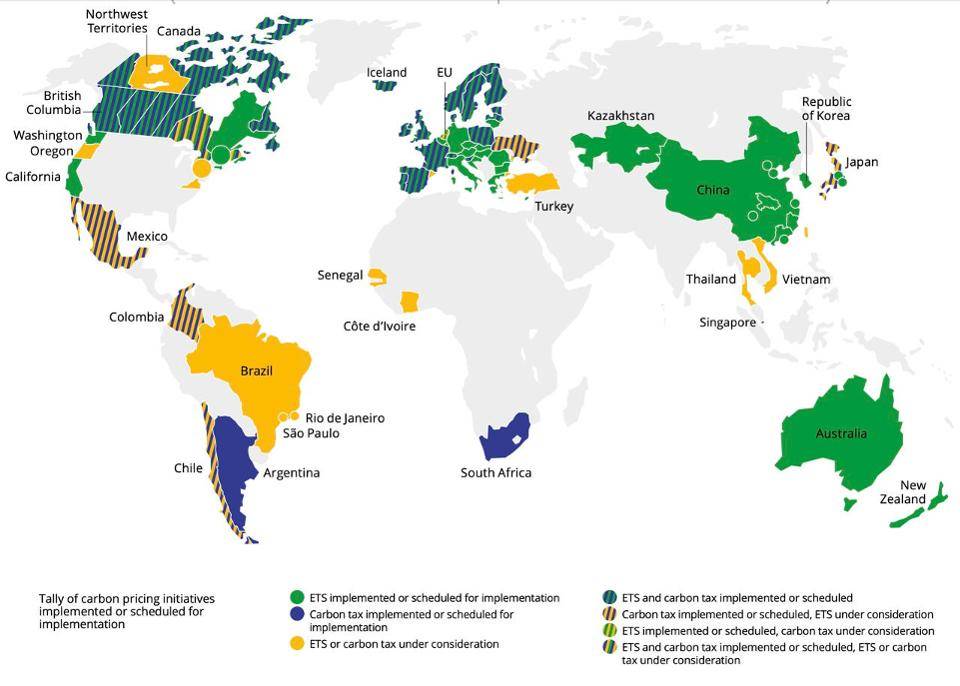

As renewable energy becomes cheaper and cheaper, governments around the world are taking increasingly aggressive actions to make fossil fuels more expensive – by taxing them. At least 40 national and sub-national governments around the world now have a carbon tax or carbon cap-and-trade system in place, with several more scheduled to implement one or officially considering it.

And the pace has been picking up in recent years. Since 2017 China, Singapore, Canada, South Africa, Mexico, and Chile have rolled out carbon pricing policies, and several countries have expanded previously existing programs. Here in the US, while environmentalists lamented the Trump administration’s decision to withdraw from the Paris Agreement in 2017, 13 US states representing 38.8% of US GDP have already passed carbon pricing laws, with several more being considered in other state legislatures.

And the pace has been picking up in recent years. Since 2017 China, Singapore, Canada, South Africa, Mexico, and Chile have rolled out carbon pricing policies, and several countries have expanded previously existing programs. Here in the US, while environmentalists lamented the Trump administration’s decision to withdraw from the Paris Agreement in 2017, 13 US states representing 38.8% of US GDP have already passed carbon pricing laws, with several more being considered in other state legislatures.

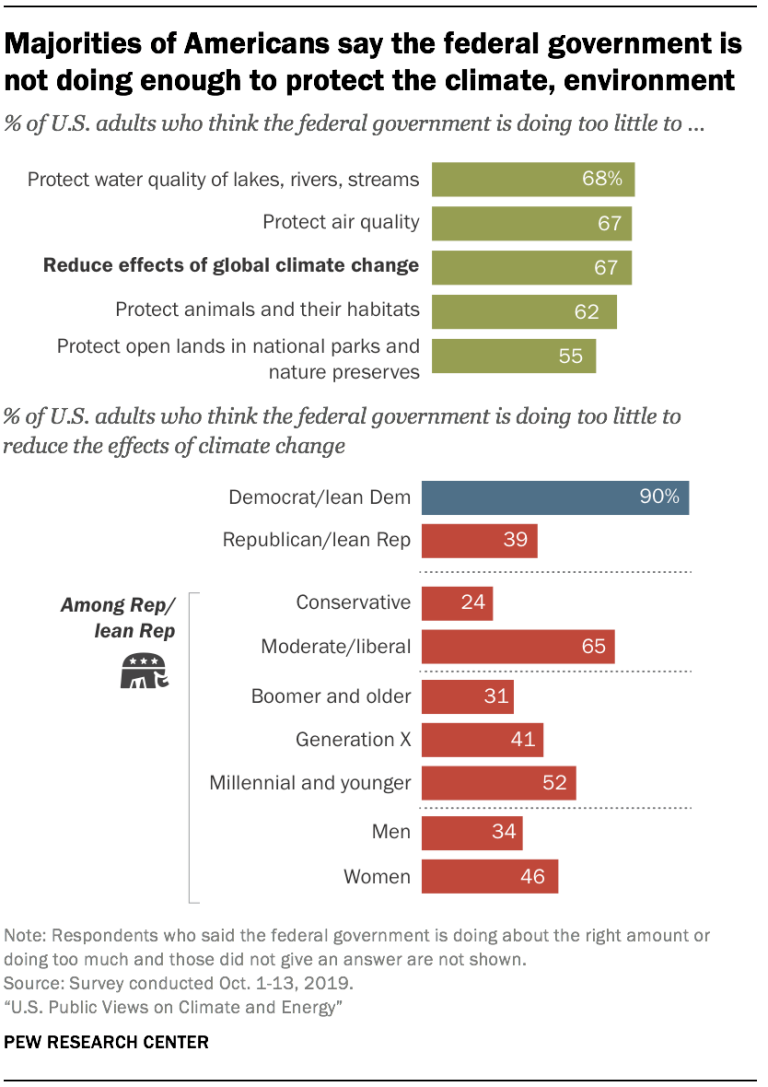

Public opinion is shifting towards favoring more aggressive climate policies. Last year Pew reported that super-majorities of Americans now believe the federal government should do more to mitigate climate change. Even among Republicans, majorities of younger and more moderate voters now favor federal action to reduce the effects of climate change.

SourceAnd this I think spells out the endgame for fossil fuels. These three forces – cheapening renewable energy, sustainable investment campaigns, and government policy – have now formed a mutually reinforcing loop that forms a noose tightening around the fossil fuel industry’s neck. It goes like this: cheap renewable energy reduces the economic dependence its consumers have on conventional energy sources and insulates them from the economic effects of a carbon tax or similar policies – think of a person who drives a Tesla and has solar panels on her roof; she doesn’t care if the government raises carbon taxes; she knows she won’t pay them – this increases the proportion of the population that favors carbon-reduction policies and the propensity of the government to pass such laws. These laws impose greater costs on fossil fuel companies, which hurts their returns to investors. Investors increasingly dump their holdings in the sector, raising the cost of capital for conventional energy companies – meanwhile, the institutional investors that are left are increasingly prohibiting the boards of these companies from even trying to lobby against such efforts. The higher cost of capital makes it even more difficult for coal, oil, and gas producers to stay competitive, so the relative attractiveness of renewables increases further still, and the cycle repeats itself.

SourceAnd this I think spells out the endgame for fossil fuels. These three forces – cheapening renewable energy, sustainable investment campaigns, and government policy – have now formed a mutually reinforcing loop that forms a noose tightening around the fossil fuel industry’s neck. It goes like this: cheap renewable energy reduces the economic dependence its consumers have on conventional energy sources and insulates them from the economic effects of a carbon tax or similar policies – think of a person who drives a Tesla and has solar panels on her roof; she doesn’t care if the government raises carbon taxes; she knows she won’t pay them – this increases the proportion of the population that favors carbon-reduction policies and the propensity of the government to pass such laws. These laws impose greater costs on fossil fuel companies, which hurts their returns to investors. Investors increasingly dump their holdings in the sector, raising the cost of capital for conventional energy companies – meanwhile, the institutional investors that are left are increasingly prohibiting the boards of these companies from even trying to lobby against such efforts. The higher cost of capital makes it even more difficult for coal, oil, and gas producers to stay competitive, so the relative attractiveness of renewables increases further still, and the cycle repeats itself.

Recursive feedback loops like the one I’ve just portrayed can be an extremely dangerous thing in the context of financial markets, something I’ve written about before in other contexts, sometimes leading to sudden, unforeseen, and spectacular collapses in the value of whole asset classes. Everything is in place for just such a crash in the fossil fuel market, all that is needed is a little common knowledge, say from some major institutional investors announcing they’re exiting the industry. Oh wait…

This might already be happening to the coal industry right now. Coal stocks are down over 30% over the last year during a bull market in stocks and despite still-increasing demand from places like China and other developing regions. Coal miners are filing bankruptcy left and right in America and at this rate there soon won’t be any left (you might say they’re sinking like a rock). The oil & gas industry is much larger and can hold out longer, but it still only comprises about 5% of total world stock market capitalization; big – but not too big to fail. I don’t know when it might happen – maybe in a few years, maybe in a few months – but if the oil & gas industry gets caught in the same spiral we could see the entire multi-trillion dollar sector completely devastated in a matter of months, weeks, or days. In such a scenario, the price of oil and gas might ironically increase in the short run due to supply-side effects, as companies are so broke they can’t even afford to drill. This would then make renewable energy then suddenly even more attractive. In a relatively short span of time we could see mass closures of gas-powered plants to be replaced with solar panels, and mass scraping of gas-powered vehicles to be replaced with battery-powered ones. I’m fairly confident that something like this will happen sometime this decade, and would estimate there is at least a 50% chance that by the end of the 2020s more than 50% of world energy production is generated from renewables (this is quite a bit higher than most people are forecasting, as nobody is really taking these feedback loops into account). If I’m wrong, take it up with me in 2030 and I’ll buy you a beer.

Not Too Much to Expect

What was that line again from up top about too cheap to meter? Let’s see that full quote now in context:

It is not too much to expect that our children will enjoy in their homes electrical energy too cheap to meter, will know of great periodic regional famines in the world only as matters of history, will travel effortlessly over the seas and under them and through the air with a minimum of danger and at great speeds, and will experience a lifespan far longer than ours, as disease yields and man comes to understand what causes him to age.

That sounds nice. Why don’t we do that?

Of course, a lot of that stuff has come true. Since Lewis Strauss uttered those words in 1954, hunger and poverty have fallen precipitously around the world, more people have access to transportation, life expectancy has increased, infectious diseases have declined, and we’re even starting to get a good idea about what causes us to age. Ever since the industrial revolution kicked off capitalism as we know it a couple hundred years ago, things have mostly been on the up-and-up for the human race. But capitalism was born with an original sin, one we have still not fully redeemed ourselves of: pollution. In early industrial Britain, factories spewed smog and soot into a blackened sky, substantially increasing mortality and morbidity in the nation’s industrial centers; similar hazards prevail today in China, India, and other countries early in the industrialization phase of development. And now globally the specter of climate change hangs over us all.

Economists, who by-and-large are quite fond of the idea of free markets, will tell you that in order for markets to function properly you need well-defined property rights. But there is a whole category of activities in which property rights are not well-defined known as externalities, costs from economic behavior that are imposed on third parties without their consent. The canonical example of a (negative) externality is pollution. I have a factory that makes widgets. I employ workers who voluntarily help me make widgets in exchange for a wage and I sell them to customers who voluntarily pay me money for them. Everyone wins! Except for the fact that my factory spews a bunch of sulfur dioxide into the air and poisons the neighborhood, whose inhabitants had no say in the matter.

There are a lot of bad criticisms of capitalism out there, but probably the most reasonable one is simply this: externalities are everywhere, and they matter a lot more than most proponents of the free market give them credit for, see exhibit 1: pollution. It’s not like pollution is a merely incidental feature of capitalism. The proximate cause to our modern age of industrial capitalism was basically a bunch of English merchants figuring out “Hey look at all the cool things we can do when we burn this black stuff!” But we stand now on the verge of practically eliminating pollution forever. This will be right up there with “ending slavery” on the list of great moral triumphs of our civilization, and we will make most of the progress in the coming decade.

The environmental benefits of switching to renewable energy are of course well-established and reported, so I won’t belabor those. But I do want to briefly point to two elements of the human condition that stand to greatly benefit from the coming energy transition: health and freedom.

I’m no political strategist, but I think it may have been a tactical mistake for the environmental movement to focus so much attention on climate change starting in the early part of the new century, as opposed to the health effects of air pollution. Climate change is a long-term problem whose effects are impossible to directly perceive, its subject to great uncertainty, and responsibility for it is widely diffused across the entire world: a nearly perfect recipe for human indifference. Other than its pernicious long-term greenhouse effect, carbon dioxide is an otherwise mostly benign molecule, and is a natural part of our ecosystem. But every tailpipe and smokestack on earth that emits CO2 also emits a cocktail of much more noxious chemicals with much more immediate and visible effects on human health: carbon monoxide, ozone, sulfur, ammonia, mercury, lead, coal plants even emit more radioactive uranium into the atmosphere than nuclear power plants do.

The more we learn about air pollution, the more we realize what a horror show it is. Researchers at the University of Chicago in 2018 measured it as the “single greatest threat to human health“, taking nearly 2 years off of global life expectancy, more than tobacco, alcohol, car accidents, or communicable diseases. In 2016 the World Bank estimated that air pollution costs the global economy over $5 trillion a year. While the problem is much worse in the developing world, those of us in rich countries aren’t free of the problem yet. People living in the same county as a coal power plant suffer much higher rates of mortality, and this leads to thousands or tens of thousands of premature deaths in the United States every year. The much more common case of living close to a busy freeway is also bad for you. Air pollution also makes us stupider. Umpires even make more mistakes on low-air-quality days, and even the stock market apparently does worse on more polluted days.

Cleaning up the air offers immediate and tangible benefits to people, and has historically enjoyed bipartisan support (remember that the US started the EPA under the Nixon administration and passed a successful sulfur-dioxide cap-and-trade law under George Bush Sr.). Fortunately, as renewable energy becomes ever more economical, nearly all of these sources of pollution will fall by the wayside, leading to one of the greatest boons to human health since penicillin.

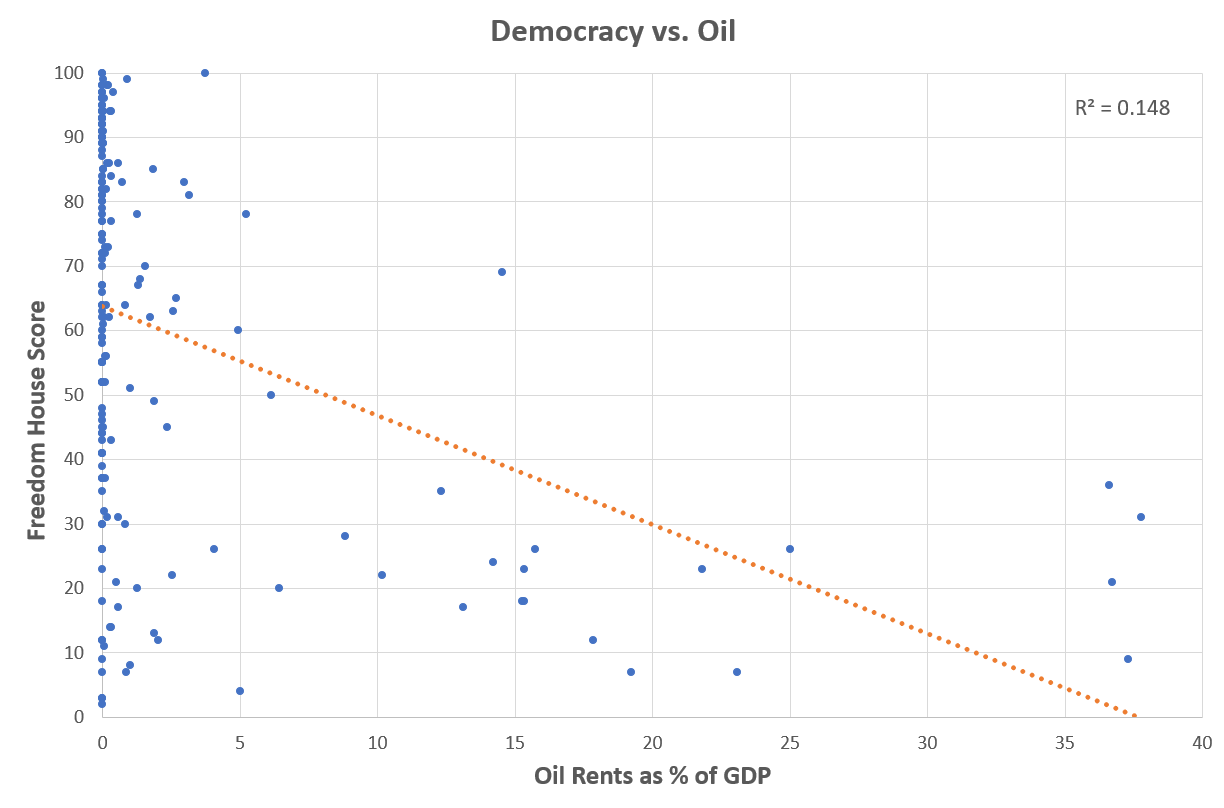

But perhaps even greater still will be the effect the energy transition will have on world freedom. This is clearly more speculative but hear me out. Liberty, like water, doesn’t appear to mix well with oil. Of the major oil exporting nations of the world, the great majority of them are autocratic regimes hostile to Western liberal democratic capitalism. Quantitatively, the relationship between democracy and oil doesn’t look good, it looks like this:

This is a graph comparing 194 nations’ score by Freedom House, which measures how democratic a country is, against how important oil is to its economy, as measured by the World Bank. There is a strong negative relationship; countries whose economies are more highly dependent on oil tend to have relatively low scores on political freedoms and civil liberties. The graph is a little messy because most countries fall on the zero line of the y-axis, they produce basically no oil. But the relationship is strongly statistically significant. This result is sometimes referred to as “resource curse” and has been strongly supported by academic research.

This is a graph comparing 194 nations’ score by Freedom House, which measures how democratic a country is, against how important oil is to its economy, as measured by the World Bank. There is a strong negative relationship; countries whose economies are more highly dependent on oil tend to have relatively low scores on political freedoms and civil liberties. The graph is a little messy because most countries fall on the zero line of the y-axis, they produce basically no oil. But the relationship is strongly statistically significant. This result is sometimes referred to as “resource curse” and has been strongly supported by academic research.

Think of some of biggest oil economies in the world: Russia, Saudi Arabia, Iran, Venezuela. These are all repressive, plutocratic regimes that tyrannize their citizens at home and antagonize democratic nations abroad. Of the 13 member nations of OPEC, only one – Kuwait – is classified by Freedom House as “partly free.” The rest are “not free.” This relationship is certainly not a coincidence. Oil wealth allows rulers to “buy off” would-be political rivals, reinforcing a ruling oligarchy whose interests are all united around oil extraction, as opposed to the pluralism and competing interests that define a healthy democracy. Such singular focus on extractive industry also retards innovation and thus economic growth. Countries with especially large oil resources relative to their population (like the smaller Gulf states) may be rich, but they have not set up their society for robust economic growth. Ambitious young people in these countries don’t start new companies, they get cushy jobs at the state oil company and suck up to the ruling elites.

But soon that will no longer be an option. As fossil fuels fall out of favor these countries will have to either reform themselves or face irrelevance in the global economy. Already we’re seeing a preview of this in Venezuela, whose regime is grasping at straws to stay in power, subjecting its citizens to a oscillating mix of tyranny and anarchy as the military struggles to maintain control. Venezuela is a contemporary case study in everything-you-shouldn’t-do-when-running-a-country, but no doubt a weaker oil market has been a major contributing factor in their downfall. In fact, many of these countries, such as Russia, Saudi Arabia, and Iran have all been arguably more politically volatile and aggressive since the 2014-2015 oil bear market than they were when oil prices were higher, say in the early years of this century. Things may get worse in these places before they get better. But I am hopeful, confident even, that they eventually will get better, that as the fossil fuel market collapses so too will dictatorships around the world, replaced by freer, cleaner societies.

In my next post, I will discuss what individual investors who are interested in helping accelerate the energy transition can do to participate in it. Stay tuned!

2024 Disclosures

RHS Financial is an SEC registered Investment Advisory Firm and distributes this presentation for informational purposes only. This presentation ( hitherto referred to as the presentation throughout this disclosure), blog post, infographic, slide deck or whatever form of informational modality the reader wishes to describe this as is provided for informational purposes only and should not be construed as investment advice in any way.

We believe the information, including that obtained from outside sources, to be correct, but we cannot and do not guarantee its accuracy in any way. RHS Financial uses information from outside sources to develop graphs, charts, infographics, etc. to enhance this presentation and while we believe the information from these outside sources, to be correct, we cannot and do not guarantee its accuracy in any way,

Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors who may be employees of but do not necessarily reflect the views of RHS Financial as a company. There can be no guarantee that developments will play out as forecasted. The information in this presentation is subject to change at any time without notice. This presentation contains “forward-looking statements" concerning activities, events or developments that RHS Financial expects or believes may occur in the future. These statements reflect assumptions and analyses made by RHS’s analysts and advisors based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond RHS Financials’ control, they are no guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements. In a nutshell; these are our best guesses and please don’t assume they are fact.

Mentions of specific securities, investment products, investment indices, companies or industries should not be considered a recommendation or solicitation. Data and analysis does not represent the actual or expected future performance of any investment or investment product Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This post may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with RHS Financial and does not sponsor, endorse or participate in the provision of any RHS’ services, or other financial products. Index information contained herein is derived from third parties and is proffered to you unaltered as we derived it from the third party.

RHS Financial, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where RHS Financial, LLC and its representatives are properly licensed or exempt from licensure. This presentation is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place.

If the client is deemed suitable and agrees, RHS may employ leveraged strategies for these clients. Leverage attained through margin on a client’s account can add additional risk. While RHS tends to seek to improve return with theses strategies by applying leverage to less risky indexes, there is no guarantee that that RHS will lower risk or improve returns.

RHS Financial. 4171 24th St. Suite 101 San Francisco, CA 94114