Postmodern Finance Part 6: Don’t Bet Your Life On It

In this series, I have been arguing that differences between investors – such as the differences in their willingness to use leverage, their susceptibility to biases, and their tax statuses – lead to implications that go beyond the cookie-cutter personal finance advice that has become all but omnipresent today. Increasingly, investors are told just to buy a few index funds – more stocks when you’re younger and more bonds when you’re older – and be done with it.

And why should younger investors hold more stocks than older ones? Because, so the thinking goes, stocks are riskier, risk is the only thing that determines return, and younger investors have more time to work off a potential bear market.

In fact, economists have long puzzled over just how much of a reward the risky stock market offers over risk-free cash. According to a famous calculation by economist Greg Mankiw, the historical risk-adjusted return of the stock market over cash is like the choice between a guaranteed $51,300 and a 50/50 bet paying either $50,000 or $100,000, it would seem almost crazy not to take the risk.

But risk is in the eye of the beholder. The ups and downs of the stock market do not take place in a vacuum. Rather, the stock market tends to fall when other things are going down as well: economic growth, employment, wages, housing prices, hemlines… So it’s not merely the fact that you can lose money in the stock market that makes it risky, it’s that it’s just when you might need your money back the most that the stock market might give you back the least.

Not everyone, however, is equally affected by the ebb and flow of the business cycle. The classic example is of the stockbroker versus the tenured professor of finance. One could imagine the same sort of person becoming either one or the other (I faced a similar choice myself), and the two will have a lot of the same sorts of knowledge and skills. But a stockbroker’s salary is likely to rise and fall right alongside the market; he may therefore conclude, both reasonably and ironically, that he shouldn’t put much money in stocks, in case of leaner times. The tenured university professor, on the other hand, enjoys a virtually guaranteed lifetime income. So long as she lives within her means, a stock market crash is literally of mere academic interest to her, and so she may feel comfortable putting the entirety of her wealth in it.

We can take this logic further. Below are a few modest proposals on how investors may choose to make their portfolio look different than others’ based on their job, where they live, and currency they use.

Bet Against Your Boss

The risks of the job market are highly related to the stock market, and all the more so for those stocks in the industry you work in. While there’s no reason to suspect that any given industry will deliver higher returns over the long run, there is good reason to suspect that poor stock performance in a given industry will coincide with layoffs and wage freezes. For that reason, rather than investing in an index fund that includes the entire market, all else equal it would be preferable for workers to exclude the industry they work in from their portfolios, especially in highly cyclical lines of work like energy, mining, and construction.

Unfortunately, what we more often see is the opposite: investors frequently try to pick winning stocks from those industries that they are most familiar with, thinking (almost always erroneously) that their industry know-how will turn into market-beating success. Employers all too often make this problem worse by offering their own company stock as an investment option in their 401(k) plan. Though it’s less common than it used to be, 39% of employers still offer company stock in their 401(k)s, and 12% even have the audacity to make contribution matches with company stock. It seems that every time there is a high-profile corporate bankruptcy, we inevitably find workers forced to learn the lesson of diversification the hard way, as they find themselves without a job or a nest egg.

In perhaps no other industry do we see this unintentional doubling down on risk as much as the one closest to us here in San Francisco: technology. Equity compensation, whether through stock options, restricted stock units, or employee stock purchase plans, is an extremely common and significant form of income in the tech industry, leaving many people in the field with heavy positions in their employer. What’s more, many tech workers have an even greater zeal for buying other tech companies, hoping always of course to find the next Google or Amazon or AOL (well, maybe not that last one, but it’s always hard to tell ahead of time).

Can tech workers still get the benefits of equity compensation without being unduly exposed to the tech industry? Actually, yes. Though an imperfect solution for concentrated holdings in a single stock, high net worth investors may wish to short-sell the technology sector through futures in order to hedge the risk of their human capital. Particularly when done as part of a strategically levered portfolio, hedging one’s industry out of their investments may give an investor greater ability to tailor their balance of risk and return to better suit them. The hard part is getting the investment community to get on board with even considering human capital. The idea of short-selling is anathema to index-advocates one-size-fits-all mentality, and most traditional managers remain too narrowly focused on absolute return numbers to think of how their investments interact with their client’s life.

Sell Your Neighbors Short

Homeownership has long been considered the pinnacle of financial responsibility, but as the housing bubble and bust of last decade showed, it is not without its risks. Buying a house and having a mortgage represents a very large, non-diversified, levered bet on a single asset, one that is subject to the vagaries of the local economy. Though it is universally accepted that homeowners should insure their house against fire and other acts of God, virtually no one insures against the financial risks of their house. This is unfortunate, because, again, it is especially at those times that housing prices are depressed that homeowners are likely to find their investment portfolios down, and their job security at risk, something that many learned the hard way a few years ago.

Again, whether or not an investor owns their home or rents may impact what mix of investments they want to hold. For the same amount of risk tolerance, homeowners may wish to own more bonds, to diversify their home equity risk. They may even wish to consider short-selling their own neighborhood as a hedge. In 2006, the Chicago Mercantile Exchange, working with the Nobel-prize winning economist Robert Shiller, began trading of futures contracts based on housing prices in 10 major US cities as well as a national composite. Shiller has stated that he hopes these markets enable individuals to better manage the risk of this essentially important and intimate asset in our lives. So far, financial institutions have not warmed up much to the idea of hedging your home.

Again, whether or not an investor owns their home or rents may impact what mix of investments they want to hold. For the same amount of risk tolerance, homeowners may wish to own more bonds, to diversify their home equity risk. They may even wish to consider short-selling their own neighborhood as a hedge. In 2006, the Chicago Mercantile Exchange, working with the Nobel-prize winning economist Robert Shiller, began trading of futures contracts based on housing prices in 10 major US cities as well as a national composite. Shiller has stated that he hopes these markets enable individuals to better manage the risk of this essentially important and intimate asset in our lives. So far, financial institutions have not warmed up much to the idea of hedging your home.

Borrow from Foreigners

An interesting wrinkle in the efficient markets approach to investing comes from currencies. An important component of the risk of investing in foreign assets is that of the exchange rate on the currency they are denominated in. But while foreign currencies can add to the risk of an investment, they do not contribute to its long-run return.

The upshot of this is that holding a market-capitalization weighted index of all the world’s assets, with all its foreign currency exposure, is not generally efficient, and some amount of currency hedging is probably optimal.

The upshot of this is that holding a market-capitalization weighted index of all the world’s assets, with all its foreign currency exposure, is not generally efficient, and some amount of currency hedging is probably optimal.

This is an idea that actually has caught on with investors recently. Even Vanguard, long the champion of plain vanilla, has recommended investors apply some currency hedging to their investments, and their popular core international bond fund (part of the target date retirement series allocation) is fully hedged. Meanwhile, currency-hedged equity ETFs have exploded in recent popularity in the last few years (although this is probably just another example of investors recklessly chasing performance).

Though currency hedging is likely to catch on and have positive risk-reducing properties for many investors, I am actually more interested in its potential for return-enhancement. Although no currency can be expected to consistently appreciate or depreciate against another, at any given time interest rates vary across currencies: some higher, some lower. For decades sophisticated investors have taken advantage of this fact by borrowing in currencies with low interest rates and lending in currencies with high rates, a strategy known as the carry trade. The carry trade has historically been a profitable strategy, and seems to be partly compensation for assuming global macroeconomic risk (high interest rate currencies often depreciate against low rate ones during recessions), although its risk-adjusted returns have been quite attractive.

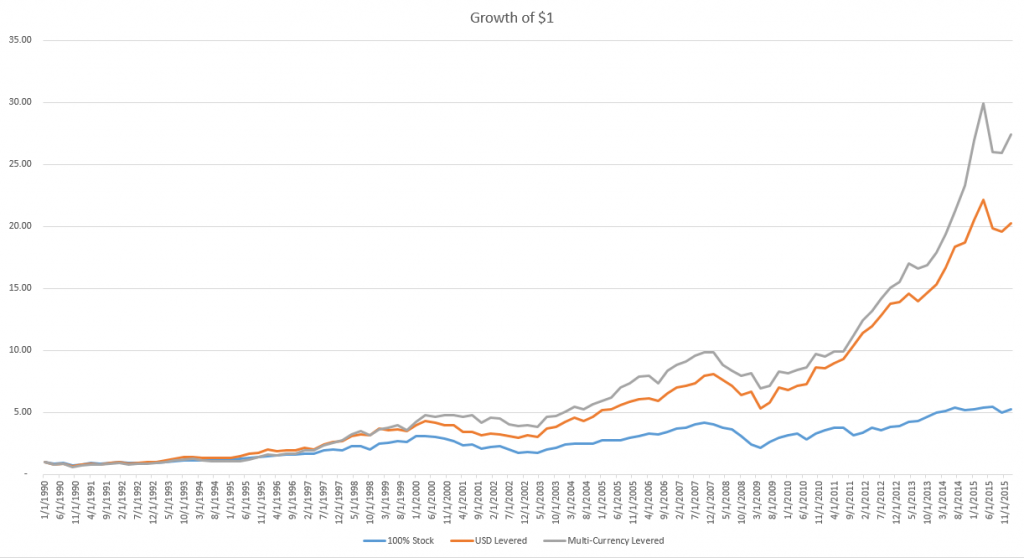

We at RHS Financial are big fans of strategically applying leverage to improve risk-adjusted returns. But why restrict ourselves to just US dollars as our funding source? Below I look at the historical returns to the following three strategies:

1. 100% Stock. Invested completely in stocks with no leverage (specifically the MSCI World index, an index of stocks from developed market countries around the world, including the US)

2. USD Levered. Invested 100% in world stock and 100% in long-term US treasury bonds (100% leverage), with a borrowing rate equal to 1 month US LIBOR. (Rebalanced quarterly)

3. Multi-Currency Levered. Invested 100% in world stock and 100% in long-term US treasury bonds (100% leverage), borrowing 33.3% each from the 3 currencies with lowest current local 1 month LIBOR (or equivalent) out of a universe of 10 developed market currencies. (Rebalanced quarterly)

Between 1990 and 2015 developed market stocks have delivered an annualized return of 6.5%. Not bad, but a 2x levered portfolio invested equally in stocks and bonds did nearly twice as good, at 12.1% a year, with nearly equal risk. Finally, our multi-currency strategy, which borrowed from the three cheapest currencies each quarter, took advantage of its lower average borrowing rates and earned 13.4% per year, with slightly smaller drawdowns in the last two major bear markets.

Between 1990 and 2015 developed market stocks have delivered an annualized return of 6.5%. Not bad, but a 2x levered portfolio invested equally in stocks and bonds did nearly twice as good, at 12.1% a year, with nearly equal risk. Finally, our multi-currency strategy, which borrowed from the three cheapest currencies each quarter, took advantage of its lower average borrowing rates and earned 13.4% per year, with slightly smaller drawdowns in the last two major bear markets.

Now, needless to say, these strategies are not for everyone. But that is sort of the point. The degree to which investors may want to engage in hedging and speculative strategies such as these will depend on a multitude of factors that do not avail themselves to a simple risk-tolerance quiz. Financial professionals should be able to adapt their solutions to their clients, not the other way around. Next time we will take the topics in this series full circle and look towards how we should think about financial planning in the postmodern framework.

Disclosures: This post is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place. Please contact us at your earliest convenience with any questions regarding the content of this post. For actual results that are compared to an index, all material facts relevant to the comparison are disclosed herein and reflect the deduction of advisory fees, brokerage and other commissions and any other expenses paid by RHS Financial, LLC’s clients. An index is a hypothetical portfolio of securities representing a particular market or a segment of it used as indicator of the change in the securities market. Indexes are unmanaged, do not incur fees and expenses and cannot be invested in directly.

2024 Disclosures

RHS Financial is an SEC registered Investment Advisory Firm and distributes this presentation for informational purposes only. This presentation ( hitherto referred to as the presentation throughout this disclosure), blog post, infographic, slide deck or whatever form of informational modality the reader wishes to describe this as is provided for informational purposes only and should not be construed as investment advice in any way.

We believe the information, including that obtained from outside sources, to be correct, but we cannot and do not guarantee its accuracy in any way. RHS Financial uses information from outside sources to develop graphs, charts, infographics, etc. to enhance this presentation and while we believe the information from these outside sources, to be correct, we cannot and do not guarantee its accuracy in any way,

Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors who may be employees of but do not necessarily reflect the views of RHS Financial as a company. There can be no guarantee that developments will play out as forecasted. The information in this presentation is subject to change at any time without notice. This presentation contains “forward-looking statements" concerning activities, events or developments that RHS Financial expects or believes may occur in the future. These statements reflect assumptions and analyses made by RHS’s analysts and advisors based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond RHS Financials’ control, they are no guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements. In a nutshell; these are our best guesses and please don’t assume they are fact.

Mentions of specific securities, investment products, investment indices, companies or industries should not be considered a recommendation or solicitation. Data and analysis does not represent the actual or expected future performance of any investment or investment product Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This post may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with RHS Financial and does not sponsor, endorse or participate in the provision of any RHS’ services, or other financial products. Index information contained herein is derived from third parties and is proffered to you unaltered as we derived it from the third party.

RHS Financial, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where RHS Financial, LLC and its representatives are properly licensed or exempt from licensure. This presentation is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place.

If the client is deemed suitable and agrees, RHS may employ leveraged strategies for these clients. Leverage attained through margin on a client’s account can add additional risk. While RHS tends to seek to improve return with theses strategies by applying leverage to less risky indexes, there is no guarantee that that RHS will lower risk or improve returns.

RHS Financial. 4171 24th St. Suite 101 San Francisco, CA 94114