Postmodern Finance Part 2 – The Index Fund Revolution

This is part two in my series on our current state of knowledge in wealth management, how we got here, and what we can do better. For part one click here.

Suppose you are shopping for a new car, or a fancy new electronic gadget of some kind. There are many different options of varying quality and cost, and you want to get the best your money can buy, so you do your research, going over consumer reports and online reviews. You compare the features of different products and try to assess the quality of different brands. Now suppose in the middle of all this trudging through technical data and claims that one was “awarded best in class” or another was “rated best value,” you come across one option that marketed itself solely on the fact that it was cheaper than most of the other options. It makes no claims to being better in any dimension other than cost; in fact, its producers don’t even feign an effort to make the product seem of superior quality, rather, they state that their product is as good as the average of everyone else’s. “But it’s a lot cheaper,” they hasten to add.

You might imagine that some very cost-conscious consumers would be attracted to this modest offering, but you’d probably be surprised if this product had more market share than any single one of its competitors and had been gaining on them at an increasing rate over the last 20 years. And yet, this sort of scenario is exactly what we have seen in the financial industry with regard to index funds. So what’s an index fund and why have they become so popular? These investments, which scarcely existed before the 90s but now command trillions of dollars, are truly one of the great examples of the ideas of economic theory getting applied to real-world problems. They are the direct result of the development of Modern Portfolio Theory, a world-changing set of ideas conceived in the mid-20th century at the University of Chicago and now taught around the world.

The Theory That Shook the World

In my last post I showed how Harry Markowitz used ideas from probability theory to build a solid mathematical framework for determining how an investor should allocate her portfolio among various investments in order to optimally balance the risk and expected return of her portfolio as a whole. The key insight was that by diversifying among different assets, an investor can build a portfolio that’s risk is less than the sum of its parts, and that by using techniques of mathematical optimization, we can show that certain portfolios are “efficient” (offer the best possible expected return for a given amount of risk) while others are inferior or inefficient (their risk or return characteristics can be improved upon) and that a rational investor should prefer an efficient portfolio.

There were a couple very practical problems with Markowitz’s solution: the first was that performing the necessary calculations to find the set of efficient portfolios among the few dozen assets in a typical investor’s portfolio (much less the many thousands that are out there trading in the market) requires intense computation, way beyond what was possible in the 50s or 60s when the theory was developed (it can be done nowadays on an ordinary computer using a program such as Excel, but even still if you try to use more than a hundred assets or so the calculation can take several minutes and might crash your computer if you try to do anything else at the same time.)

The second problem was that the solutions it gave were highly sensitive to the inputs provided – the expected return, variance, and correlation of all the assets under consideration. The theory gave no guidance on how to estimate these variables, they were simply assumed. It turns out that the measures of risk – variance and correlation – are reasonably stable over intermediate periods of time, so an investor can assume the riskiness of an asset over the recent past will continue into the near future. An asset’s expected return, on the other hand, was much harder to grasp. Returns vary widely over long periods of time, so using past returns was futile.

Because of this Markowitz’s portfolio theory attracted little notice from practitioners at the time. Even economists weren’t sure what to make of it at first. The famous economist economist Milton Friedman, who served as Markowitz’s Ph.D. advisor, supposedly even argued that Markowitz’s thesis was just an exercise in theoretical statistics and not really economics, so they couldn’t grant him a Ph.D. in the subject.

Economists are usually interested in the idea of equilibrium. Similar to how a scientist may use thermodynamics to explain the equilibrium heat or pressure of a tank of gas whose individual particles are evenly distributed due to their random collisions, economists seek to describe how supply and demand set equilibrium prices as a result of all the interactions of the firms and individuals that make up an economy.

In the early 1960s several economists came across Markowitz’s work and independently worked out the implications of what its application would look like in equilibrium. The basic idea goes like this: it doesn’t really matter if individual investors can determine the expected returns on different assets; the market itself will solve the problem. Because, all else equal, investors prefer less risky assets to more risky ones, they will tend to bid up the prices of the former and down the prices of the latter. As prices adjust, so too will the assets’ expected returns, until eventually they converge onto a linear relation where an asset’s expected return is exactly proportional to its risk[1].

I have just stated an idea known as the Efficient Market Hypothesis. In my opinion, it’s one of the most important ideas not just of economics, but in the history of human thought, so it bears some hammering out:

Why is it so rare that we quickly find a free parking spot right where we need it or a hundred dollar bill on the sidewalk? It’s because there are many people who also want that free parking spot or hundred dollar bill, they are in the same time and place as you, and they’re also keeping their eyes peeled for such attractive opportunities. As a result, quick profits (monetary or otherwise) are usually scooped up immediately. As economists like to say, money is rarely left on the table. When we apply this logic to the financial markets, it has special implications. Suppose it was somehow known that the stock market always went up on Thursday. If that were the case, then investors would rush to buy stocks on Wednesday. As more and more investors flooded into the market, they would push prices up until there was no longer any upside left on Thursday.

Of course, no one expects to make money in the stock market based just on what day of the week it is, but many people believe they can make great returns just by buying “good” companies and avoiding “bad” ones. Clearly there there are certain companies that are at the top of their game and have plenty of growth opportunity, while other ones are unprofitable and in stagnant or dying industries, so by merely doing a little research to determine which stocks belong to the former and which ones to the latter an investor can beat the market and earn handsome profits, the thinking goes. Not so, according to the Efficient Market Hypothesis, for if it is commonly understood that Company A will rapidly grow its earnings over the next few years, and Company B will make weak or negative earnings, then investors will seek to buy Company A today and sell Company B, adjusting the prices and expected returns on each until one is no longer clearly a better deal than the other. Taken to its logical conclusion, the EMH asserts that all prices immediately adjust to all relevant information, and because a la Markowtiz investors are concerned with maximizing their return and minimizing their risk, that means that in an efficient market the only thing that should predict an asset’s return is how risky it is, and the only way for an investor to increase the return on his portfolio is to take more risk. Analyzing a company’s financial statements, conducting industry analysis, forecasting economic growth – none of that makes any difference, the only thing that matters is risk.

Having thus eviscerated traditional notions of prudent investment management, the early pioneers of Modern Portfolio Theory then went one step further and stated that the first problem of Markowitz’s portfolio theory – calculating the efficient frontier of optimal portfolios – was moot. There was only one optimal portfolio that all investors should hold: the entire market itself. Key to this conclusion was the idea of a risk-free rate that all investors could borrow and lend at (usually assumed to be the rate on short-term government bonds i.e. T-Bills). Given this and a few other assumptions, it can be shown that in an efficient market, a portfolio that holds every single asset in the world in the same proportion as its value in the market (so that if US stocks make up 10% of the world’s wealth and Japanese stocks make up 5%, then the portfolio allocates 10% to US stocks and 5% to Japanese stocks) has the highest possible ratio of return to risk. If an individual investor wants to accept less risk and return as the overall market she will still place her entire investment portfolio in the market portfolio, but hold some fraction of her wealth in cash invested at the risk free rate. Conversely if and investor wants to take on more risk and return than the overall market he will borrow at the risk free rate and put the entirety of his wealth, plus the borrowed sum into the market portfolio. Thus, the tradeoff between risk and return on a portfolio becomes a function of a simple straight line found by determining the tangent line between the risk free rate and the market portfolio (called the Capital Asset Line). The concept can be shown graphically like so:

From Theory to Practice

The new science of Modern Portfolio Theory made the bold prediction that trying to pick undervalued stocks was a waste of time, the only thing that mattered was risk, and everyone should hold the same portfolio. But what did the facts have to say?

In 1972 three economists performed one of the earliest empirical studies of the market, trying to determine how risk and return were related. They looked at every stock that traded in the US between 1931 and 1965 and measured how its recent riskiness predicted its future return. Sorting the results by deciles, a clear linear relation held.

The relation was a little “flatter” than the theory predicted (this will become important later), but overall the data matched the model. Risk and return were positively related, the theory was a success!

The next year Princeton economist Burton Malkiel published A Random Walk Down Wall Street, which sought to popularize the Efficient Market Hypothesis and other ideas coming out of modern finance. A national bestseller, the book also famously showed that on average, professional money managers running mutual funds could not beat a market benchmark such as the S&P 500 Index. Malkiel wrote that while at any given time there are plenty of mutual fund managers that have outperformed the market recently, this is merely the random result of good luck, and does not predict that they will continue to outperform. Indeed, he found, looking at the best performing mutual funds at several different points in the past, they went on to subsequently perform no better than the market on average.

Near the end of the book Malkiel calls for a new way to invest:

What we need is a no-load, minimum management-fee mutual fund that simply buys the hundreds of stocks making up the broad stock-market averages and does no trading from security to security in an attempt to catch the winners. Whenever below-average performance on the part of any mutual fund is noticed, fund spokesmen are quick to point out “You can’t buy the averages.” It’s time the public could.

He would not have to wait long. In 1974 John Bogle founded a new mutual fund company called Vanguard, and in 1975 launched the Vanguard 500 Index Fund. The first index fund available to the general public, it was unique in the investment industry at the time for stating that it would make no attempt to beat its benchmark, the S&P 500; it would merely keep up with it. And because that meant it wouldn’t have to trade nearly as much or conduct costly research and due diligence, it could charge a much lower fee to its investors.

Vanguard was not exactly an overnight success. The fund raised a measly $11 million in its initial public offering and was nearly cancelled. But Bogle persisted and assets slowly trickled in. By 1986 they launched their second fund: a bond market index fund. Index funds slowly gained traction over the years and accelerated in the late 90s with the launch of the first Exchange Traded Funds (ETFs) – index funds that trade like stocks. By the turn of the millennium index funds made up just under 10% of all assets invested in equity funds. Since then they have more doubled that share.

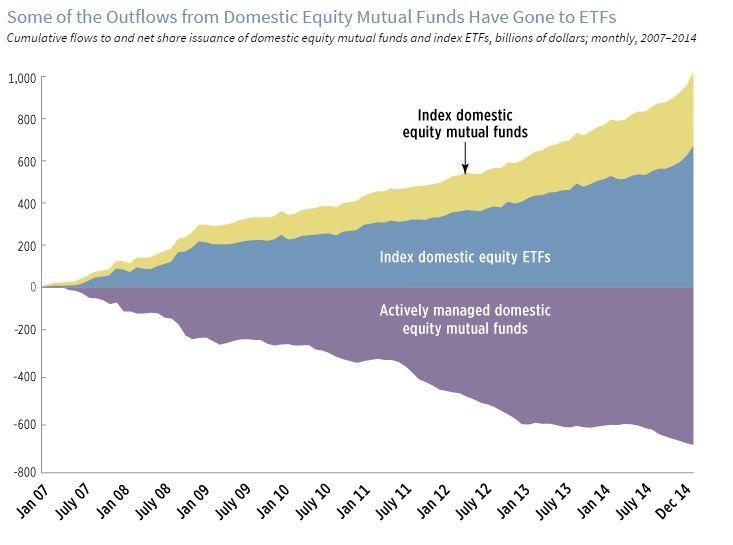

In recent years there has been an exodus out of traditional actively managed mutual funds and into index mutual funds and ETFs.

Vanguard is now the 2nd largest asset manager in the world, with approximately $3 trillion under management. BlackRock is number 1 with $4.5 trillion and State Street is in third with $2.5 trillion. All three have the majority of their assets under management invested in index mutual funds and ETFs, products that compete on the basis of their low cost and high liquidity, as opposed to any prospect of outperforming the market. The index fund revolution has ushered in a great race to the bottom in the asset management industry, with the spoils going to giants that can scale their operations to service trillions of dollars at the lowest cost possible by providing commodified solutions to the most investors possible.

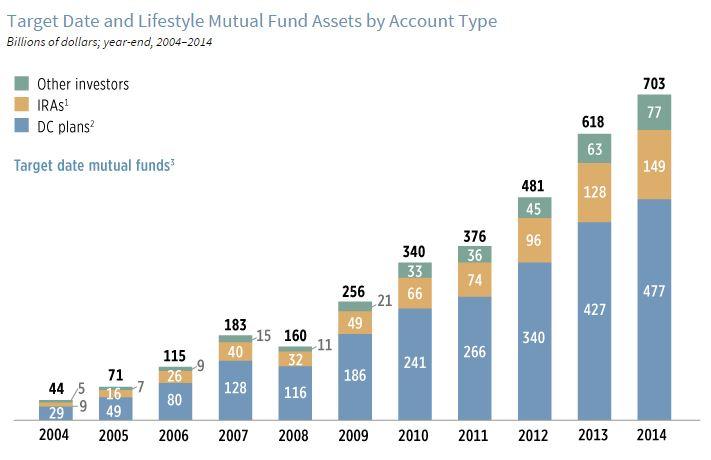

In 2003 Vanguard took the logic of index investing one step further by launching its series of Target Retirement Funds. These funds are intended to be a one-size-fits-all solution to investors, with each fund designed to be held by an investor who will be retiring on or near a certain year, such as 2035. They invest in a handful of underlying domestic and international stock and bond index funds and gradually adjust the stock/bond mix to become more conservative as the investor nears retirement (and presumably has a lower tolerance for risk). Since then target retirement and other all-in-one-solution funds have become a magnet for assets, especially in 401(k) plans, where they have often become the default investment option for participants.

In the early 2010s (the teens? the tens? what are we calling this decade?) a handful of startups began sprouting up offering automated investment solutions to investors using index ETFs to build portfolios for individual investors. Dubbed “Robo-Advisors” by the industry, these newcomers attempt to provide many of the services of a traditional financial advisor algorithmically and at lower cost. Similar to target retirement funds, they build a portfolio for the investor out of index funds and regularly rebalance it, gradually shifting to more conservative investments as the investor ages, while also offering some ancillary services such as basic tax management. Startups Betterment and Wealthfront have led the way with these technologies, but recently incumbents Vanguard and Charles Schwab have responded with their own robo-advisor offerings. Whether this new breed of investment solutions will be won out by the old guard or the young blood remains to be seen, but one thing that is almost certain is that index investing and low-cost commodity solutions will continue to gain ground against the old way of doing business on Wall Street.

Questioning Modernity

You have probably caught on by now that there is a catch. After all, this blog is not being written by a Vanguard or some other provider of index funds. So what is the flaw in this modern investment paradigm, so universally beloved by academics, financial journalists, Warren Buffet, and millions of ordinary investors?

Recall from above that if the central tenants of Modern Portfolio Theory are true, then every investor should hold the exact same portfolio, the market portfolio of all the assets in the world proportionate to their weight, with positive or negative allocations to the risk free asset to adjust their risk/return profile. It says nothing about switching from stocks to bonds as one gets older. The proponents of index funds have performed a bit of sleight of hand in proselytizing the theories that are supposed to support their investment solutions. While an index fund represents the market portfolio within the narrow confines of the particular asset class it represents (such as US stocks, or investment grade bonds), they generally represent only a sliver of the marketable wealth of the world’s stocks, bonds, commodities, and real estate. As far as I know, there currently exists no investment solution that combines index funds together to form the true global market portfolio, much less one that adjusts its risk/return by using leverage or cash, and so in a sense, the world still have never seen an actual index fund. Index fund advocates sneer at the traditional active manager who buys Google or sells Microsoft in an attempt to outperform the S&P 500, but they do not blink at the proposal to sell stocks and buy bonds in order to reduce risk with age, even though according to the assumptions of their theory, there is no logical difference between these two decisions!

“The assumptions of their theory.” This is something I glossed over a bit above, and wish to return to it now. The intellectual edifice of Modern Portfolio Theory rests upon a handful of key assumptions, from which everything I have expounded upon here flows from. These assumptions are as follows (paraphrased from my CFA textbook):

- All investors are concerned solely with the risk and return of their portfolio and wish to hold a portfolio that lies on the Markowitz Efficient Frontier.

- All investors can borrow and lend unlimited amounts at the risk-free rate (i.e. the rate on treasury bills).

- All investors are rational and all hold the same beliefs about their investments.

- There are no taxes, transactions costs, or inflation.

- There is only one currency and all investors consume the same basket of goods.

Suffice it to say, every one of these assumptions is a little unrealistic. Over the next several posts I will be exploring what the implications are when we no longer assume each of these axioms is true. For now, notice how each of these assumptions paints investors as all basically the same, homogeneous agents conducting sterile transactions in the impersonal capital markets, like particles of gas colliding in a tank. It is no coincidence that the quintessential investment solution in this modern view of finance is the index fund, a one-size-fits-all commodity to be produced and sold at the lowest possible cost. For the rest of this series I will be exploring how investors are different, in their goals, their limitations, and their beliefs, taking the postmodern approach that all these differences are valid and truth, in finance, is not static.

[1] More precisely, there is supposed to be a linear relation between an asset’s expected return and it’s beta. Beta is the standard measure of risk in portfolio theory, measured as the covariance of an asset’s returns with the market portfolio’s, divided by the variance of the returns of the market portfolio. Throughout this post when I write about the riskiness of an asset, I am referring to its beta.

2024 Disclosures

RHS Financial is an SEC registered Investment Advisory Firm and distributes this presentation for informational purposes only. This presentation ( hitherto referred to as the presentation throughout this disclosure), blog post, infographic, slide deck or whatever form of informational modality the reader wishes to describe this as is provided for informational purposes only and should not be construed as investment advice in any way.

We believe the information, including that obtained from outside sources, to be correct, but we cannot and do not guarantee its accuracy in any way. RHS Financial uses information from outside sources to develop graphs, charts, infographics, etc. to enhance this presentation and while we believe the information from these outside sources, to be correct, we cannot and do not guarantee its accuracy in any way,

Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors who may be employees of but do not necessarily reflect the views of RHS Financial as a company. There can be no guarantee that developments will play out as forecasted. The information in this presentation is subject to change at any time without notice. This presentation contains “forward-looking statements" concerning activities, events or developments that RHS Financial expects or believes may occur in the future. These statements reflect assumptions and analyses made by RHS’s analysts and advisors based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond RHS Financials’ control, they are no guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements. In a nutshell; these are our best guesses and please don’t assume they are fact.

Mentions of specific securities, investment products, investment indices, companies or industries should not be considered a recommendation or solicitation. Data and analysis does not represent the actual or expected future performance of any investment or investment product Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This post may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with RHS Financial and does not sponsor, endorse or participate in the provision of any RHS’ services, or other financial products. Index information contained herein is derived from third parties and is proffered to you unaltered as we derived it from the third party.

RHS Financial, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where RHS Financial, LLC and its representatives are properly licensed or exempt from licensure. This presentation is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place.

If the client is deemed suitable and agrees, RHS may employ leveraged strategies for these clients. Leverage attained through margin on a client’s account can add additional risk. While RHS tends to seek to improve return with theses strategies by applying leverage to less risky indexes, there is no guarantee that that RHS will lower risk or improve returns.

RHS Financial. 4171 24th St. Suite 101 San Francisco, CA 94114