Postmodern Finance Part 1 – Wall Street: A History of Thought and Thoughtlessness

This is going to be the first in a multi-part series on what I see as the current state of the investment management business, how we got here, and how our firm views and does things differently compared to most of our peers. I’m going to make the case that most of the practices commonly used today to manage portfolios for individuals are based on a combination of outdated rules-of-thumb and flawed applications of financial theory, and that these leave investors woefully underserved. Central to my story is how traditional Wall Street forces and the academic ideas of Modern Portfolio Theory have evolved together to create what is today a highly commoditized financial services industry, one that likes to pretend that all investors are basically the same. Taking a bit of poetic license, I will argue that the oversimplifications of Modern Portfolio Theory that treat people and their portfolios as undifferentiated commodities can be greatly improved upon by taking a postmodern approach to portfolio management[i] that recognizes the multifaceted ways investors differ in their beliefs, preferences, constraints, and abilities and how their choices affect the market and optimal investment strategy in a dynamic way.

A Brief History of Legalized Gambling

Today, it is commonly accepted that everyone should save for their future, and that a good portion of their savings should be invested in common stocks and other risky assets. These days over half of Americans own stocks, usually through mutual funds in their 401(k)s or other retirement plans. The financial sector plays an increasingly large role in the economy and our daily lives, and the study of finance as a science occupies a venerated role in academia, attracting some of the world’s best and brightest minds in its attempt to understand and influence the role of capital in society.

It was not always like this. Before the 1950s finance attracted little scholarly attention, and the popular opinion of the financial markets was that they were casinos for the rich and foolish, with Wall Street bankers and brokers collecting the rake. This view had a good deal of merit.

Aaron Brown describes in his book The Poker Face of Wall Street how in the early days, gambling and finance were naturally intertwined. The early stock markets were to fund speculative colonial ventures (the first publicly traded corporation was the Dutch East India Company, the famous spice trade monopoly) of the sort that attracted frontiersmen who tended to have an affinity for card-playing. As the New World was settled, local governments and chartered corporations often raised funds by issuing “bonds” that more resembled lottery tickets than the stable investments we typically associate with the word today. Though the foundations of corporate law and equity ownership date back to the Medieval ages, early stock traders generally gave little thought to the underlying economics of the companies they bought and sold; “long-term investor” was not yet part of the vernacular, and most stock trades were speculative bets in search of a quick profit.

The first financial markets were founded by gamblers, more or less accidentally, who were mostly interested in finding new ways to bet with one another. That the system they created happened to be the best way to allocate capital to the newly forming enterprises of the early days of the industrial revolution was mostly a happy coincidence.

Though investing in the stock market has, on average, been solidly profitable as far back as we can tell, it’s unlikely that the “average” investor enjoyed much of those returns in these early days. Trading commissions and management fees were much higher, and brokers enjoyed significant information advantages over their customers, which they often exploited through means of varying legal and ethical dubiousness.

That Wall Street enriches itself at the expense of its customers is an old adage. This is not so much because Wall Street was always engaging in outright fraud or deception so much as it, like a casino, has been willing to sell misplaced optimism, to benefit from the gambler’s fallacy and the triumph of hope over reason. The 1940 book Where are the Customers’ Yachts? by Fred Schwed takes its title from a joke dated back to the 1870s: a traveler to New York is walking by the harbor and is shown the impressive yachts of some Wall Street bankers, and then the yachts of some Wall Street brokers. The naïve traveler then asks, “And where are the customers’ Yachts?” In the book, Schwed compares the Wall Street man to the croupier at a roulette table. But, he explains, the croupier “…does not claim that he knows something about the order in which the numbers will come up. He just sees to it that the bets are properly paid off and that the house isn’t gypped…” Wall Street, more than just filling the role of clearinghouse for traders’ bets, makes its money by selling prophecy. In this, the Wall Street man perennially fools both his customer as well as himself, according to Schwed. “The Broker influences the customer with his knowledge of the future,” he writes, “but only after he has convinced himself. The worst that should be said of him is that he wants to convince himself badly and that he therefore succeeds in convincing himself – generally badly.” Schwed was skeptical of the ability of supposed experts to forecast the markets, seeing them as just as fundamentally unpredictable as the spin of the roulette wheel. In this, he was ahead of his time and anticipated the scientific theories on markets that would come decades later. Considering the culture of gambling that finance arose from, though, the metaphor was apt.

Finding Value

Though few investors in the early days much concerned themselves with the goings-on in the companies they were invested in, the fact is that financial securities are tied to real world enterprises that are creating something of value (usually, at least), so they ought to be worth something. But what? It wasn’t until we were a couple decades into the 20th century that the first real insights came to light.

One of the first to lay down a theory of valuation was the famous investor Benjamin Graham. Graham encouraged investors to think of themselves as partners in the businesses of the stocks they bought, and determine the worth of a company based on the consistency of its profits and the quality of its assets, without regard to the price the market was currently paying for its shares. His 1934 book Security Analysis was among the first of its kind, and ushered in a new discipline of investing based on the notion of scrutinizing a company’s income statements, balance sheet, and other fundamental data to determine its intrinsic value.

Graham saw the market as a chimera made of countless individuals making decisions based partly on reason and partly on emotion. He thought, as a result, that at any one time, the market was a “voting machine,” that is, a popularity contest for the hottest issues, but over the long run was a “weighing machine” that tended to converge to the true fundamental value of the underlying enterprises involved. In his bestselling 1949 book The Intelligent Investor, intended for laypeople, he anthropomorphized the market in a famous parable:

Imagine that in some private business you own a small share that cost you $1,000. One of your partners, named Mr. Market, is very obliging indeed. Every day he tells you what he thinks your interest is worth and furthermore offers either to buy you out or to sell you an additional interest on that basis. Sometime his idea of value appears plausible and justified by business developments and prospects as you know them. Often, on the other hand, Mr. Market lets his enthusiasm or his fears run away with him, and the value he proposes seems to you a little short of silly… You may be happy to sell out to him when he quotes you a ridiculously high price, and equally happy to buy from him when his price is low. But the rest of the time you will be wiser to form your own ideas of the value of your holdings…

Graham made a successful career out of buying stocks whose market price was below his estimate of intrinsic value. He trained and employed another investor early in his career by the name of Warren Buffet, who also had some success with this approach. Graham’s approach to the market eventually came to be known as “value investing,” a topic I will return to in a later post.

Contemporaneous with the practitioner Benjamin Graham, the academic economist John Burr Williams was among the first to put forth a theory of asset valuation. In his 1938 thesis The Theory of Investment Value, he laid out a mathematical model in which the intrinsic value of an investment is the present value of all its future cash flows. Central to this theory is what would become one of the foundational ideas of finance: the time value of money. The time value of money is a concept that addresses the fact that all else equal, we would rather have an amount of money now rather than the same amount in the future, and the sooner the better. This is not simply because we may be able to invest that money in the meantime, or because inflation may make future dollars worth less (though these factors may both increase the time value of money), but is a result of the fact that as finite, mortal beings, we are fundamentally impatient, and would rather have access to opportunities in the present than in the future. Thus, in order to delay gratification, we must be tempted by an even greater reward in the future. I won’t give up $100 today for $100 a year from now, but perhaps I will for $105 in a year’s time, and if not that then perhaps for $110. The time value of money then refers to how dollar amounts are to be compared across the present and future. In order to compare apples to apples, economic values that lie in the future must be discounted to their equivalent present value, based on some rate at which a person values her time; this is known as a discount rate.

Williams’ idea then, was that an investment should be worth the sum of all the future cash payments the asset would ever make, discounted back to the present using a discount rate that was appropriate for the investor’s time value of money. For a stock, these cash flows are the dividends, and this process is known as the dividend discount model, which today is taught in every introductory finance class.

While Graham and Williams made the first steps to elevating the study of finance to a science, they still did not thoroughly answer the most basic question that faces every investor: how do I build a portfolio of investments that properly balances risk and return? Certainly the concept of diversification is nothing new (the proverb “don’t put all your eggs in one basket” dates back to at least the early 1700s), but ideas on what sorts of investments were appropriate for what investors in which proportions were mostly a matter of intuition or rule of thumb prior to the 1950s, and tended to change over time. In the 1920s blue-chip industrial stocks were considered appropriate for “widows and orphans,” but two decades later 90% of Americans polled were opposed to owning any common stocks because they were “not safe” or “a gamble.” In The Intelligent Investor Benjamin Graham gives portfolio policy a wide berth: “We have suggested as a fundamental guiding rule that the investor should never have less than 25% or more than 75% of his funds in common stocks, with a consequent inverse range of between 75% and 25% in bonds.” Around the same time as he wrote this there emerged the “100 minus your age” rule, which holds that the percentage of his portfolio an investor allocates to stocks should be found by subtracting his age from the number 100. Rules like these have the merit of being simple, but lack a strong theoretical justification.

Markowitz and Modern Finance

In the early 50s, Harry Markowitz was an economics student at the University of Chicago. He was interested in using mathematics to describe the stock market, and had studied the ideas of John Burr Williams, but found they lacked the crucial element of risk and uncertainty that faces the investor. In 1952 he published his Ph.D. thesis; simply titled “Portfolio Selection,” it started a revolution in finance and launched an entirely new field of scientific inquiry known today as Modern Portfolio Theory.

Like many theories, Markowitz’s insight was so powerful because it gave theoretical rigor to an idea that had been known about for ages. Essentially, Markowitz provided a mathematical justification for diversification, and with it, a framework for evaluating risk.

Markowitz understood that an investor is concerned chiefly with the return an asset will provide, but that this return is uncertain. He assumed that an asset can be described using concepts from probability theory: its expected return, or the return that is most probable, its variance (a measure of how widely the returns may fall around their expected value), and its correlation with other assets (a measure of how similarly or differently two assets behave). Using these statistics from each asset in the portfolio one can then find the expected return and risk of the overall portfolio.

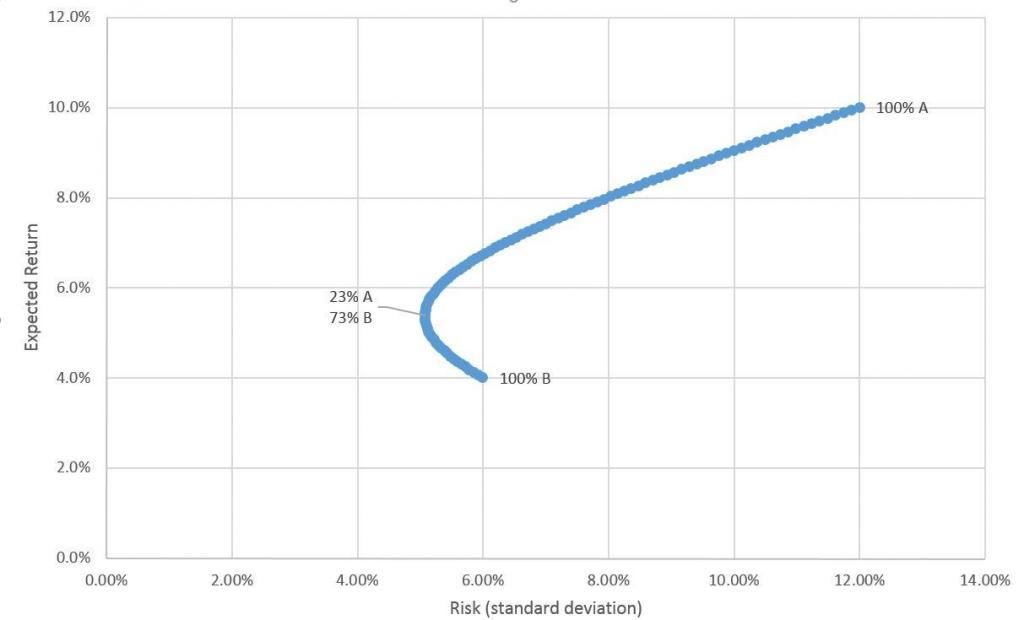

The expected return of the portfolio is simply the weighted average of the expected return of each asset in it. For example, if a portfolio holds 75% of asset A and 25% of asset B and the expected return is 10% for asset A and 4% for asset B, then the expected return for the portfolio is (0.75 * 10%) + (0.25 * 4%) = 8.5%.

The magic comes in when determining the risk of the portfolio. Because assets aren’t perfectly correlated with each other (some are up when others are down), combining them in a portfolio makes its risk less than the sum of its parts. The exact calculation is given by the formula:

Using the two assets above as an example and assuming a -25% correlation, solving for each possible combination of the two gives the following nonlinear relation:

Notice something interesting happens as we move away from a 100% allocation to the safer asset B and add some of riskier asset A. The expected return increases, and the risk actually decreases. This is because although asset A is more volatile (has higher variance) than asset B, its swings will often offset those of asset A, leading to smoother overall portfolio returns. In this example, risk is minimized with a 23% allocation to A and a 73% allocation to B. This means that merely holding asset B is strictly inferior to owning this allocation; even very risk-averse investors seeking portfolio safety should prefer to diversify with asset B.

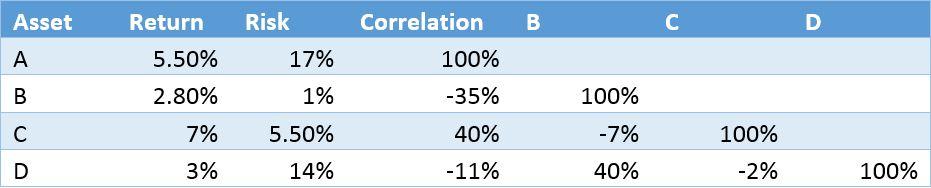

That’s the two asset example. As we add more assets the possible number of portfolio allocations explodes, but the risk and return of any portfolio can still be found with the above formula. Consider a 4 asset example with the following characteristics:

The chart below plots the risk and return of these four assets, as well as a few portfolios consisting of various combinations of the 4. Point E is an even combination of 25% each. Notice again the expected return is the average of the four, while the risk is significantly less than the average.

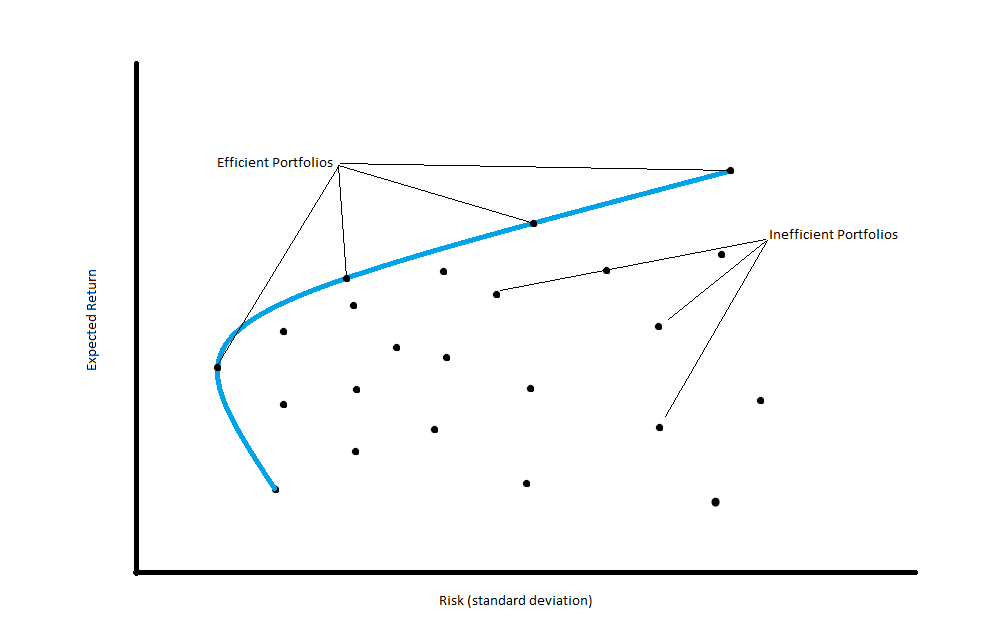

Compare portfolio E to portfolio F. Portfolio F has the same risk as portfolio E, but has a higher expected return. Similarly, Portfolio G has the same expected return as E, but a much lower amount of risk. In fact, I found these portfolios by using a mathematical optimization algorithm to maximize the expected return subject to certain risk level (for portfolio F) or to minimize the risk subject to a certain return level (for portfolio G).

Again, a rational investor should prefer portfolio F or G to portfolio E. They provide a strictly superior risk/return tradeoff compared to E. Portfolios F and G are examples of efficient portfolios. That is, for a given level of risk, they offer the greatest possible expected return.

As we increase the number of assets under consideration, there are a potentially infinite number of possible portfolios, but they will all fall under a convex line shown in the chart below. This line is known as the efficient frontier and describes all the possible combinations that maximize return for a given risk level, from the least risky portfolio all the way to the highest return portfolio. In Markowitz’s model, an investor will wish to choose a portfolio that lies somewhere along the efficient frontier, with the exact point depending on his risk tolerance. All portfolios that fall below the efficient frontier have an inefficient and undesirable risk/return tradeoff that can be improved upon.

Though Markowitz shed light on the power of diversification, his early insights were highly technical and of little practical importance. Though solving the portfolio optimization problem by hand with two or three assets is doable, and remains a staple test question on finance undergraduate exams, doing it with the dozens of securities that are typically in a real investor’s portfolio requires significant computational resources, something that were in short supply in the 1950s.

In the next post we will see how when economists made a few key assumptions about the way investors behave, they were able to transform Markowitz’s technical treatise into a revolutionary way of thinking about the markets, starting a movement that now commands trillions of dollars and effects how everyday investors around the world manage their money.

[i] Previous researchers beat me to the punch of riffing off Modern Portfolio Theory by coining Postmodern Portfolio Theory, but this extension mostly just addresses the existence of non-normal distributions in security returns, something that was known as early as the 1960s and that, in my opinion, isn’t really all that interesting. My usage of the word postmodern here I think is more in keeping with its use in literature and other settings, where it refers to approaches that adopt multiple perspectives as sources of truth.

2024 Disclosures

RHS Financial is an SEC registered Investment Advisory Firm and distributes this presentation for informational purposes only. This presentation ( hitherto referred to as the presentation throughout this disclosure), blog post, infographic, slide deck or whatever form of informational modality the reader wishes to describe this as is provided for informational purposes only and should not be construed as investment advice in any way.

We believe the information, including that obtained from outside sources, to be correct, but we cannot and do not guarantee its accuracy in any way. RHS Financial uses information from outside sources to develop graphs, charts, infographics, etc. to enhance this presentation and while we believe the information from these outside sources, to be correct, we cannot and do not guarantee its accuracy in any way,

Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors who may be employees of but do not necessarily reflect the views of RHS Financial as a company. There can be no guarantee that developments will play out as forecasted. The information in this presentation is subject to change at any time without notice. This presentation contains “forward-looking statements" concerning activities, events or developments that RHS Financial expects or believes may occur in the future. These statements reflect assumptions and analyses made by RHS’s analysts and advisors based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond RHS Financials’ control, they are no guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements. In a nutshell; these are our best guesses and please don’t assume they are fact.

Mentions of specific securities, investment products, investment indices, companies or industries should not be considered a recommendation or solicitation. Data and analysis does not represent the actual or expected future performance of any investment or investment product Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This post may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with RHS Financial and does not sponsor, endorse or participate in the provision of any RHS’ services, or other financial products. Index information contained herein is derived from third parties and is proffered to you unaltered as we derived it from the third party.

RHS Financial, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where RHS Financial, LLC and its representatives are properly licensed or exempt from licensure. This presentation is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place.

If the client is deemed suitable and agrees, RHS may employ leveraged strategies for these clients. Leverage attained through margin on a client’s account can add additional risk. While RHS tends to seek to improve return with theses strategies by applying leverage to less risky indexes, there is no guarantee that that RHS will lower risk or improve returns.

RHS Financial. 4171 24th St. Suite 101 San Francisco, CA 94114