“Make it a Quadruple”

This month, the financial press has been abuzz with the latest case study in Wall Street’s storied history of feeding speculative frenzies: the quadruple-levered ETF. On May 2 the SEC approved a request to list two ETFs, the ForceShares Daily 4X US Market Futures Long Fund under the ticker UP, and the ForceShares Daily 4X US Market Futures Short Fund, under the ticker DOWN (I couldn’t believe those tickers weren’t already taken). These ETFs would seek to maintain 4x levered position, one long and one short, in the S&P 500, so that on a day when the S&P 500 was up 1%, UP would be up 4% and DOWN would be down 4%. Similar products already exists that seek 2x or 3x leverage; the primary innovation here is that “these go to eleven four.”

The near universal reaction to the announcement has been astonishment and ridicule: Are you really crazy enough to buy a quadruple-leveraged ETF? The absurdity of 4x-levered ETFs. Feds back to loving a well run lottery. 4x ETFs: an investment innovation no one needed. The move also marks a change of tune for the SEC; just last year the commission was considering adopting new regulations that would curtail the listing of levered ETFs, even outlawing 3x versions. It seems there must still be some there who aren’t keen on the idea, as just the other day the plot thickened and it was announced the SEC was having second thoughts about the controversial products. Whether or not UP or DOWN ever see the light of day, however, it’s worth emphasizing that these are terrible investment products, and given our generally positive attitude towards leverage in other contexts, it bears explaining what levered ETFs get wrong.

What levered ETFs are most notorious for is the fact that while they usually do a good job delivering their stated multiple on the underlying market over a given single day, this does not translate into the same multiple being achieved for periods any longer than that. This can lead to surprising results. If you are considering buying one of these funds, you may think to yourself, Markets generally go up over time. I’m willing to tolerate a lot of risk in the short run for better long run returns, so if the stock market gives good returns, why not double down (or triple or quadruple)?

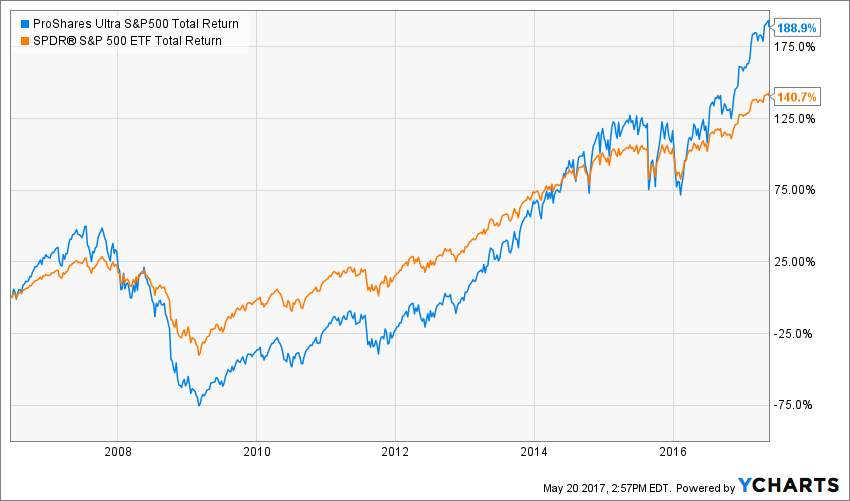

Unfortunately it doesn’t work this way. Observe the first levered ETF to launch in the US: the ProShares Ultra S&P 500 fund SSO in 2006, which seeks 2x the daily performance of the S&P 500, compared to an investment in a simple unlevered S&P 500 ETF.

SSO has delivered only slightly better long term performance than its unlevered counterpart (an annualized return of 10.21% vs 8.38%), and it took ten years for it to definitively pull ahead (a lead I won’t be surprised to see it lose come the next bear market). Why the discrepancy? While part of the issue is the greater costs involved in running a levered fund, the real culprit is the unyielding mathematical logic of compounding. Suppose we have two investors who each have a $100 investment: one in the S&P 500 and the other in a 2x levered S&P 500 fund. On day one stocks fall by 1%. Our first investor will now have $99 and the second will have $98. So far so good. But now consider what happens on day two and stocks go up by 1%. The investors will not be back to where they started. Rather, the first investor will now have 99 * (1 + 1%) = $99.99. The second investor, on the other hand will have 98 * (1 + 2%) = $99.96. As markets zig and zag over time, the levered investor will inevitably suffer a greater drag as the result of this compounding effect.

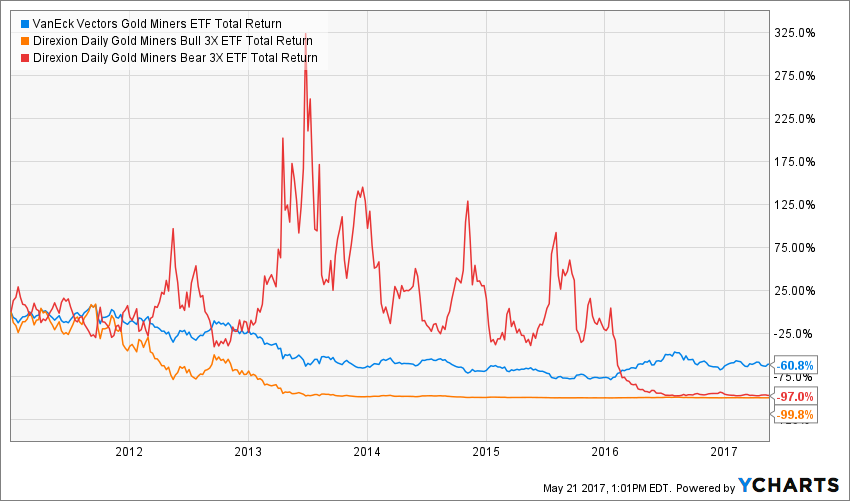

The more volatile the investment and the more leverage used, the greater this drag will be. On this score, SSO actually does fairly well compared to most levered ETFs. For some products, the volatility drag is so great they don’t even go in the same direction as the underlying market long term! My favorite example of this is with gold miners and Direxion Investments’ pair of 3x levered products on them.

In this chart, the blue line represents GDX, a popular ETF of gold mining stocks. The orange line is NUGT, which essentially applies 3x leverage to GDX, and the red line is DUST, which is 3x short GDX. As you can see, over this period gold miners have been in a protracted bear market, losing 60% of their value since 2011. It may not be surprising then to see that a 3x levered long position in the fund then has lost almost everything. What is shocking, is that being triple short the same market would have lost you almost just as much money! Because gold mining stocks are such a volatile asset class, often experiencing daily swings of 5% or more in either direction, what their long-run returns have ended up being has ultimately been less important for these levered instruments than the cumulative eroding effect of compounding.

Inexplicably, the funds remain extremely popular with investors, with millions of shares traded every day, despite billions of dollars having been collectively lost on them. Popular 3x levered funds exist for oil, gas, treasury bonds, and myriad corners of the stock market, almost all of which have been long term performance disasters. There’s not just one but two different 3x levered S&P 500 ETFs, with over $1 billion in assets between the two of them. So it’s really not surprising that somebody now wants to launch a 4x version.

Nor will it be a surprise when investors lose billions more on such a fund. Just how bad would will it be? Below I simulate the hypothetical performance of a 4x levered S&P 500 fund[1] had it been trading over the same time period as SSO in the first graph above.

Yikes! The 4x levered would have actually lost money, at an average 2.71% annual rate over these last 11 years (less in real life, after fees and transactions costs were paid). What’s more, investors would have suffered through a whopping 99% maximum drawdown between 2007 and the bottom of the financial crisis in 2009.

In my next post, I’m going to dive into more detail on what is to distinguish between good and bad uses of leverage. In a third post on this topic I will explore what, if anything, these levered ETFs are actually good for. In the meantime, caveat emptor, UP and DOWN!

[1] To simulate 4x daily performance, I multiply the daily return on SPY by four, less three times the rate on 3 month treasury bills to account for financing costs. This is still an overly optimistic backtest because I do not account for transactions costs and management fees.

Disclosures: This post is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place. Please contact us at your earliest convenience with any questions regarding the content of this post. For actual results that are compared to an index, all material facts relevant to the comparison are disclosed herein and reflect the deduction of advisory fees, brokerage and other commissions and any other expenses paid by RHS Financial, LLC’s clients. An index is a hypothetical portfolio of securities representing a particular market or a segment of it used as indicator of the change in the securities market. Indexes are unmanaged, do not incur fees and expenses and cannot be invested in directly.

2024 Disclosures

RHS Financial is an SEC registered Investment Advisory Firm and distributes this presentation for informational purposes only. This presentation ( hitherto referred to as the presentation throughout this disclosure), blog post, infographic, slide deck or whatever form of informational modality the reader wishes to describe this as is provided for informational purposes only and should not be construed as investment advice in any way.

We believe the information, including that obtained from outside sources, to be correct, but we cannot and do not guarantee its accuracy in any way. RHS Financial uses information from outside sources to develop graphs, charts, infographics, etc. to enhance this presentation and while we believe the information from these outside sources, to be correct, we cannot and do not guarantee its accuracy in any way,

Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors who may be employees of but do not necessarily reflect the views of RHS Financial as a company. There can be no guarantee that developments will play out as forecasted. The information in this presentation is subject to change at any time without notice. This presentation contains “forward-looking statements" concerning activities, events or developments that RHS Financial expects or believes may occur in the future. These statements reflect assumptions and analyses made by RHS’s analysts and advisors based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond RHS Financials’ control, they are no guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements. In a nutshell; these are our best guesses and please don’t assume they are fact.

Mentions of specific securities, investment products, investment indices, companies or industries should not be considered a recommendation or solicitation. Data and analysis does not represent the actual or expected future performance of any investment or investment product Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This post may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with RHS Financial and does not sponsor, endorse or participate in the provision of any RHS’ services, or other financial products. Index information contained herein is derived from third parties and is proffered to you unaltered as we derived it from the third party.

RHS Financial, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where RHS Financial, LLC and its representatives are properly licensed or exempt from licensure. This presentation is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place.

If the client is deemed suitable and agrees, RHS may employ leveraged strategies for these clients. Leverage attained through margin on a client’s account can add additional risk. While RHS tends to seek to improve return with theses strategies by applying leverage to less risky indexes, there is no guarantee that that RHS will lower risk or improve returns.

RHS Financial. 4171 24th St. Suite 101 San Francisco, CA 94114