Does the Stock Market Take a Summer Break?

This week, I’m going to be taking a little summer vacation and go camping. As a result, our trading activity over the next several days is likely to be lower than usual. And of course I’m not the only one; this summer other financial advisors, broker-dealers, hedge fund managers, and other professional and amateur traders all around the world will be taking holidays, during which most will do little or no trading. Do all these vacations have an effect on market prices?

There is an old piece of advice in finance, “Sell in May and go away.” That is, sell your stocks before the summer months and buy them back in the fall (usually around Halloween). The phrase is so old in fact, that no one is sure exactly when it was first said, but it seems to have originated in 19th century London. The thinking goes that since financial professionals will be away in large part for the summer, there will be little buying pressure for stocks during the season, so you might as well sell them ahead of time and wait til everybody gets back to work.

Now, I don’t normally like to give investment advice based on rhyming couplets, and the “vacation theory” above would be laughable to a financial economist. But time (and data) make fools of us all. Below is a chart comparing the average monthly returns during the summer months of May through September against the rest of the year in 17 developed market countries going back to 1970 and 14 emerging market countries starting between 1988 and 1995.

It’s rare that we see such a consistent pattern in financial markets. Every single country has lower average returns in the summer than in the rest of the year. Eleven countries have even experienced negative average returns over the summer. Strangely, the pattern is strong even in such southern-hemisphere countries as Australia, Chile, and South Africa, where the concept of a summer vacation is probably a bit different than for those of us on the top side of the world.

What’s going on here? The “Sell in May” effect is, to my mind, one of the strangest phenomenons in finance. Other return “anomalies” that I’ve talked about, such as value, momentum, and low-volatility investing have clear economic and psychological explanations. I cannot, however, think of any reasonable way to explain why the stock market should care about the changing of the seasons. Certainly macroeconomic risks do not depend on the tilt of the Earth’s axis, nor can I think of any behavioral bias that would cause investors to be particularly averse to equity risk during the summertime of the northern hemisphere. The default explanation is the traditional “summer holiday” hypothesis; but this is hardly an explanation at all. Clearly, if this were the only reason behind the pattern, it should be swiftly destroyed by arbitrage. If stocks consistently fall in May and rise again in October because of investment managers’ vacations, then more hard-working investors (or the algorithms they employ) should jump ahead of the pack and sell in April and buy in September. As more investors try to jump in front of one another, eventually any predictability from one month to the next should be eliminated, but this doesn’t seem to be happening.

Digging Deeper

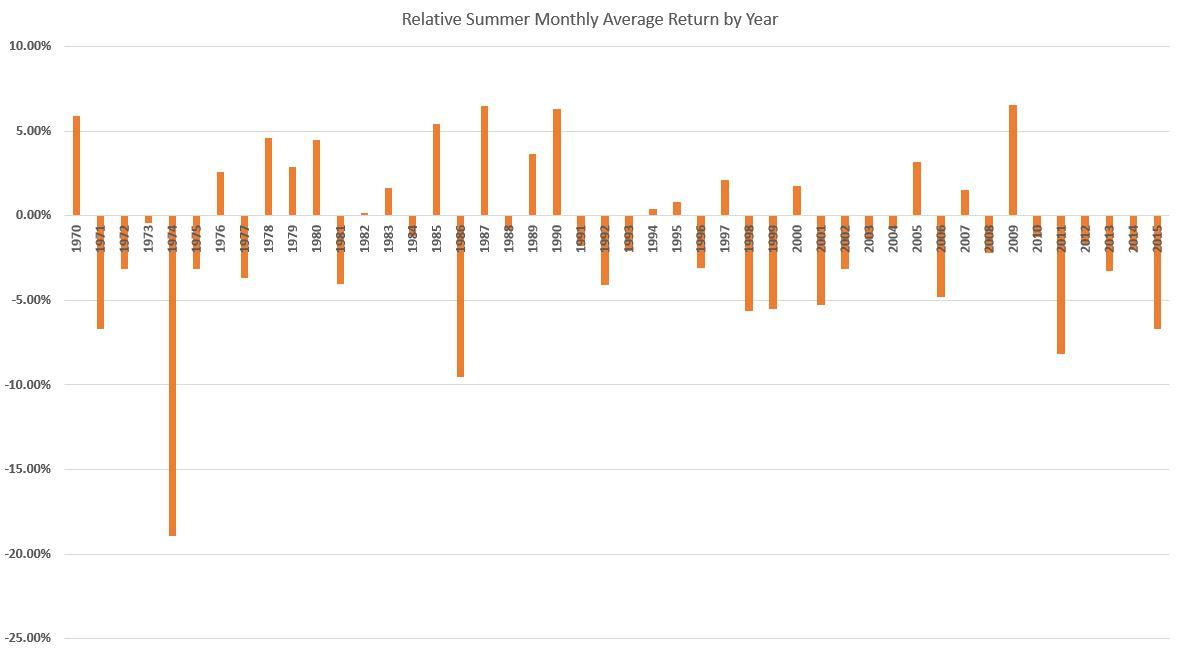

There’s a joke about the statistician who sleeps with his head in the oven and his feet in the freezer because the average temperature is comfortable. Sometimes broad averages are misleading, especially in financial markets where outliers oftentimes dominate. Below I break down the “Sell in May” phenomenon year by year, looking at how the summer months did on average compared to the rest of the year, averaged across all the same countries in the above sample.

Between 1970 and 2015, the summer delivered higher average returns than the rest of the year in 18 out of 46 years; about 40% of the time – only marginally less than the 50/50 ratio we should expect. Most of the weakness we’ve seen in the summer is concentrated in a few particular episodes: the oil-shock related crisis of ’74; another oil related crash in ’86; the eurozone crisis of 2011. Throw out just these three bad years and the underperformance of summer goes away almost completely.

Are crises such as these actually more likely to happen in the summer? Perhaps the heat causes policy-makers and banking executives to lose their heads. Or maybe it’s just a fluke. My money is on the latter.

So should investors sell in May and go away? I wouldn’t recommend it. Even if this seasonal effect does continue – and I doubt that it will – jumping completely in and out of the stock market is almost always hazardous to your wealth. Transactions costs and taxes can easily take a big bite out of any profits you might make, and sitting on cash earns you less than nothing after inflation these days. The average summer returns on stocks at least have been above zero, something that can’t be said for today’s money market interest rates.

Nonetheless, I think there is something important to learn from the Sell in May effect. As I have been writing about in my Postmodern Finance series, we cannot rely solely on theory at the expense of facts that don’t fit it. But neither can we look exclusively at facts, free of any theoretical understanding of them. The world is a messy, complicated place and random, unexplainable events are the norm. In investing as in life, we must try to distinguish the noise from the signal, lest we become like the gambler betting on a completely random outcome because his lucky number is “due to come up.” Investment decisions should be made on the basis of a sound economic rationale backed by large amounts of evidence; the Sell in May effect lacks the former, and the latter doesn’t hold up to close scrutiny. This summer, keep your stocks out in the sun.

Disclosures: This post is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place. Please contact us at your earliest convenience with any questions regarding the content of this post. For actual results that are compared to an index, all material facts relevant to the comparison are disclosed herein and reflect the deduction of advisory fees, brokerage and other commissions and any other expenses paid by RHS Financial, LLC’s clients. An index is a hypothetical portfolio of securities representing a particular market or a segment of it used as indicator of the change in the securities market. Indexes are unmanaged, do not incur fees and expenses and cannot be invested in directly.

2024 Disclosures

RHS Financial is an SEC registered Investment Advisory Firm and distributes this presentation for informational purposes only. This presentation ( hitherto referred to as the presentation throughout this disclosure), blog post, infographic, slide deck or whatever form of informational modality the reader wishes to describe this as is provided for informational purposes only and should not be construed as investment advice in any way.

We believe the information, including that obtained from outside sources, to be correct, but we cannot and do not guarantee its accuracy in any way. RHS Financial uses information from outside sources to develop graphs, charts, infographics, etc. to enhance this presentation and while we believe the information from these outside sources, to be correct, we cannot and do not guarantee its accuracy in any way,

Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors who may be employees of but do not necessarily reflect the views of RHS Financial as a company. There can be no guarantee that developments will play out as forecasted. The information in this presentation is subject to change at any time without notice. This presentation contains “forward-looking statements" concerning activities, events or developments that RHS Financial expects or believes may occur in the future. These statements reflect assumptions and analyses made by RHS’s analysts and advisors based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond RHS Financials’ control, they are no guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements. In a nutshell; these are our best guesses and please don’t assume they are fact.

Mentions of specific securities, investment products, investment indices, companies or industries should not be considered a recommendation or solicitation. Data and analysis does not represent the actual or expected future performance of any investment or investment product Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This post may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with RHS Financial and does not sponsor, endorse or participate in the provision of any RHS’ services, or other financial products. Index information contained herein is derived from third parties and is proffered to you unaltered as we derived it from the third party.

RHS Financial, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where RHS Financial, LLC and its representatives are properly licensed or exempt from licensure. This presentation is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place.

If the client is deemed suitable and agrees, RHS may employ leveraged strategies for these clients. Leverage attained through margin on a client’s account can add additional risk. While RHS tends to seek to improve return with theses strategies by applying leverage to less risky indexes, there is no guarantee that that RHS will lower risk or improve returns.

RHS Financial. 4171 24th St. Suite 101 San Francisco, CA 94114