Do I have to pay tax on stocks if I sell and reinvest? Not with Exchange Funds.

Do you have to pay tax on stocks if you sell and reinvest? Yes. But there’s a way to effectively execute a similar transaction with similar positive outcomes through an exchange fund.

If you are a tech professional, building your wealth by holding on to your employer’s stock was probably a big part of your financial success. However, now you are either worried about the downside or a large capital gains tax bill. In the past, we wrote about various strategies you can utilize to address these two concerns.

Today we would like to highlight a strategy advisors call exchange funds.

How do exchange funds work?

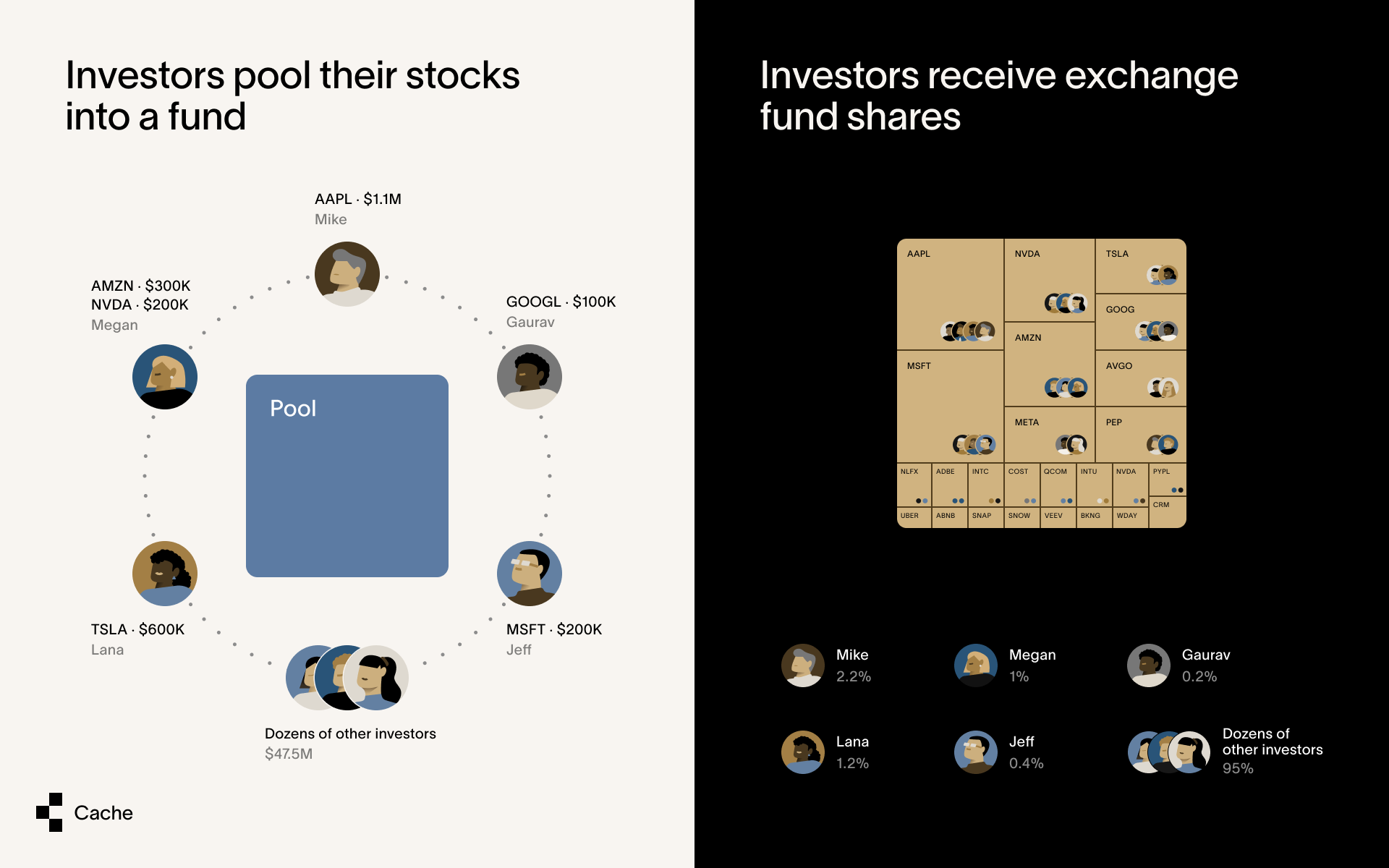

Exchange funds are private investments you participate in with other investors who are in a similar situation. You and other investors who want to avoid paying tax on stocks that have appreciated, will “sell” (in actuality contribute) and reinvest, through a swap. This process involves swapping your appreciated shares for a diversified portfolio of stocks of equivalent value, effectively deferring capital gains tax.

This strategy helps with avoiding capital gains tax for an extended period of time. Deferring those taxes requires several criteria to be met.

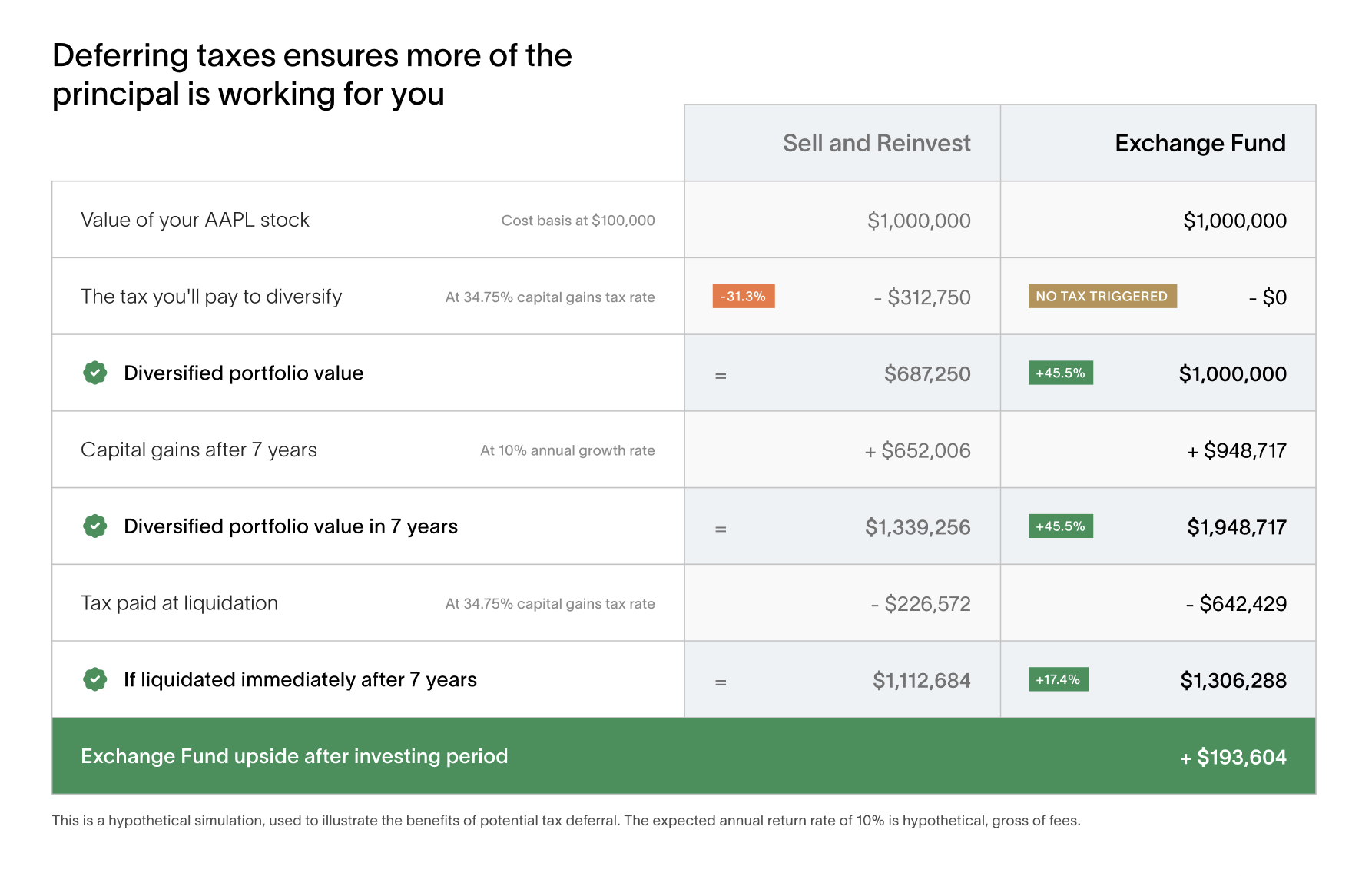

First, the investor must retain their stake in the exchange fund for a minimum of seven years to benefit fully from the tax deferral. After this period, they receive the diverse stocks from the portfolio of the exchange fund.

Secondly, while exchange funds typically aim to mirror major indices like the S&P 500 or Nasdaq 100, IRS regulations require that at least 20% of the fund’s investments be in qualifying assets, such as real estate or commodities, to ensure eligibility.

Despite the attractive proposition when it comes to avoiding paying tax on stocks when you sell and reinvest, exchange funds aren’t universally used due to several drawbacks. Entry thresholds often exceed $500,000, coupled with high initial sales fees and ongoing management fees that can potentially add up to 2.5%. Furthermore, eligibility may demand a net worth of at least $5 million, and historically, few providers have offered this investment option. Additionally, exchange funds are selective about the stocks they accept, aiming to align with their investment strategy in a limited window of time, which might limit participation opportunities.

However, the growing demand for such tax-efficient investment avenues has prompted fin-tech companies like Cache to innovate, making exchange funds more accessible and appealing for those looking to avoid capital gains tax on stocks sales.

Our fiduciary commitment to our clients’ best interests means we never accept referral fees from providers. Our enthusiasm is genuine when we can spotlight innovative solutions like those from companies such as Cache that could benefit our clients and readers.

If you want to see how exchange funds could be a solution to a part of your tax and risk problem, then schedule a free 15-minute call with us HERE.

If you want to see how exchange funds could be a solution to a part of your tax and risk problem, then schedule a free 15-minute call with us HERE.

To get a better sense of whether you have to pay tax on stocks if you sell and reinvest or if you should use an exchange fund it is important to understand exchange funds pros and cons.

Pros of Exchange Funds

Exchange funds offer several key advantages for investors:

- Diversification and Reduced Concentration Risk: Joining an exchange fund allows investors to share in the performance of a variety of stocks pooled together by fellow investors. This strategy effectively mitigates business risk associated with holding stocks in a single company, a challenge often difficult to overcome with other tax deferral and risk reduction methods. Exchange funds excel in diversifying and minimizing this specific risk.

- Tax Deferral: Among the limited options for deferring taxes on the sale and reinvestment of stocks, exchange funds stand out. By committing to a 7-year holding period, investors can defer taxes while still participating in the growth of a diversified portfolio of stocks. This deferral can significantly enhance wealth growth by postponing tax payments and benefiting from potential returns in the meantime.

- Access to New Investment Opportunities: Investing in the US and the Tech Sector has done well in the last decade. But even there we had winners and losers. Take the most recent AI boom that has driven the broad markets to all time highs. A select few companies have benefited while others have been left in the dust. By using an exchange fund, particularly those focusing on indices like the Nasdaq 100, such as Cache, you may get access to some of these investments while avoiding paying a capital gains tax bill.

- Estate Planning Strategies: For affluent individuals aiming to pass on appreciated investments to their heirs, exchange funds offer a strategic approach. Instead of bequeathing a single appreciated stock, which carries its own set of risks, exchange funds enable the transfer of a diversified portfolio. This not only reduces risk but also allows heirs to benefit from a stepped-up cost basis, potentially leading to significant tax advantages.

Cons of Exchange Funds

While exchange funds come with notable advantages, they also have their challenges:

- High Entry Requirements and Costs: Traditionally tailored for the ultra-wealthy, exchange funds often come with steep entry requirements, including high minimum investments, significant fees, and stringent net worth qualifications. For those hesitant about locking up $500,000, paying a high initial sales fee and an annual fee of .95% over seven years can be daunting, not to mention the challenge of meeting a $5 million net worth criterion. Cache, however, makes exchange funds more accessible with a lower minimum investment of $100,000, more achievable qualification criteria, and reduced fees as low as 0.4%.

- Liquidity Constraints: Avoiding capital gains tax through an exchange fund requires a long-term commitment of 7 years. If you decide to pull the funds out earlier you may lose tax benefits and be subject to fees. Furthermore, unlike your single stock position you can not borrow against it on margin.

- Investment Risk: Despite the diversification benefits, investing in a mix of tech or US stocks through an exchange fund doesn’t eliminate market volatility, sector-specific, or regional risks. This may be more risk than you are ultimately looking to take. An exchange fund may not be the perfect solution and usually is better as a part of a bigger strategy.

- Tax Reporting Complexity: After the seven-year holding period, investors and their tax advisors face the challenge of recalculating the cost basis for each position in the new, diversified portfolio. This requirement can introduce additional costs and complexity to the investment experience, necessitating careful consideration and planning.

One of the standout features of Cache is our capability to facilitate direct investments for our clients via Charles Schwab. Although exchange funds provide a compelling strategy to the question, “Do I have to pay tax on stocks if I sell and reinvest?” they are not without their limitations. Integrating them within a broader, more diverse set of inventive strategies allows us to tailor solutions that align with individual risk tolerances, fee sensitivities, and the wish to retain some level of investment in the stocks that have contributed significantly to their wealth.

If you are looking to better understand your options when it comes to avoiding capital gains tax and reducing the risk of your highly appreciate stock, set a 15-minute complimentary consultation with us HERE.

Disclosures

2024 Disclosures

RHS Financial is an SEC registered Investment Advisory Firm and distributes this presentation for informational purposes only. This presentation ( hitherto referred to as the presentation throughout this disclosure), blog post, infographic, slide deck or whatever form of informational modality the reader wishes to describe this as is provided for informational purposes only and should not be construed as investment advice in any way.

We believe the information, including that obtained from outside sources, to be correct, but we cannot and do not guarantee its accuracy in any way. RHS Financial uses information from outside sources to develop graphs, charts, infographics, etc. to enhance this presentation and while we believe the information from these outside sources, to be correct, we cannot and do not guarantee its accuracy in any way,

Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors who may be employees of but do not necessarily reflect the views of RHS Financial as a company. There can be no guarantee that developments will play out as forecasted. The information in this presentation is subject to change at any time without notice. This presentation contains “forward-looking statements" concerning activities, events or developments that RHS Financial expects or believes may occur in the future. These statements reflect assumptions and analyses made by RHS’s analysts and advisors based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond RHS Financials’ control, they are no guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements. In a nutshell; these are our best guesses and please don’t assume they are fact.

Mentions of specific securities, investment products, investment indices, companies or industries should not be considered a recommendation or solicitation. Data and analysis does not represent the actual or expected future performance of any investment or investment product Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This post may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with RHS Financial and does not sponsor, endorse or participate in the provision of any RHS’ services, or other financial products. Index information contained herein is derived from third parties and is proffered to you unaltered as we derived it from the third party.

RHS Financial, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where RHS Financial, LLC and its representatives are properly licensed or exempt from licensure. This presentation is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place.

If the client is deemed suitable and agrees, RHS may employ leveraged strategies for these clients. Leverage attained through margin on a client’s account can add additional risk. While RHS tends to seek to improve return with theses strategies by applying leverage to less risky indexes, there is no guarantee that that RHS will lower risk or improve returns.

RHS Financial. 4171 24th St. Suite 101 San Francisco, CA 94114