Culture, Investor Behavior, and the Market

Investors, being human, are not always perfectly rational, but sometimes make decisions that are influenced by their emotions or cognitive biases, which can effect market prices in interesting and predictable ways. Such is the one sentence summary and motivating principle behind behavioral finance, a topic I’ve written about quite a bit here myself. But how much of what we know about the behavior of investors is influenced by the cultures which they come from? This is the question posed by researchers in a fascinating paper I recently came across called Individualism and Momentum Around the World.

In the paper, the authors investigate how cultural variation is related to the profitability of one of the most famous and historically successful market “anomalies”: the momentum effect. Momentum is the tendency of recently outperforming stocks (or other assets) to continue to outperform, and likewise for underperforming stocks. The effect has been observed in markets around the world and in data series going back over two hundred years, making it one of the most robust findings in empirical finance. But because momentum profits seem to be unrelated to standard measures of risk, the effect is usually ascribed to “irrational” causes like investor overconfidence, inattention, or herd mentality. The authors look at how these effects may be mediated by culture, looking in particular at measures of individualism vs collectivism in society. They hypothesize that individualistic cultures are associated with more overconfident investors, who overestimate their investment knowledge and trade more aggressively on their beliefs, leading to the predictable price trends of momentum.

This is interesting because I could see it going the other way as well. It could be that in collectivist cultures investors all mimic one another’s decisions and that’s what gives rise to the momentum effect. With no obvious reason to be confident it should go one way or another, we’re left with the data to sort it out. The authors compare the returns on a long-short momentum strategy and other market data within the markets of a sample of 50 countries against each country’s score on Hofstede’s Individualism vs. Collectivism index, a widely cited scale developed by social psychologists based on extensive survey data. According to the authors, “In individualistic cultures, individuals tend to view themselves as ‘an autonomous, independent person’… while in collectivistic cultures, individuals view themselves ‘not as separate from the social context but as more connected and less differentiated from others.'” Western cultures, especially the Anglophone countries, are famously the most individualistic in the world, while Eastern cultures are known to be more relatively collectivist, though there is considerable variation within these groupings. The authors cite previous work in psychology demonstrating that persons from individualistic cultures are more likely to evaluate their own abilities as being above average, and speculate that this is likely to lead to more overconfident and excessive trading behavior when interacting with financial markets.

Their data support the hypothesis: the stock markets of more individualistic countries have higher trading volume, are more volatile, and provide greater momentum profits. And the effect size is substantial: in their sample several of the English-speaking countries experienced double-digit annual momentum returns while those of Japan, Korea, and Taiwan were not even statistically significant. Indeed, the authors cite the Japanese case as their motivating example behind the study, as Japan is somewhat famous in the literature as being the exception to the rule that momentum works “everywhere.”

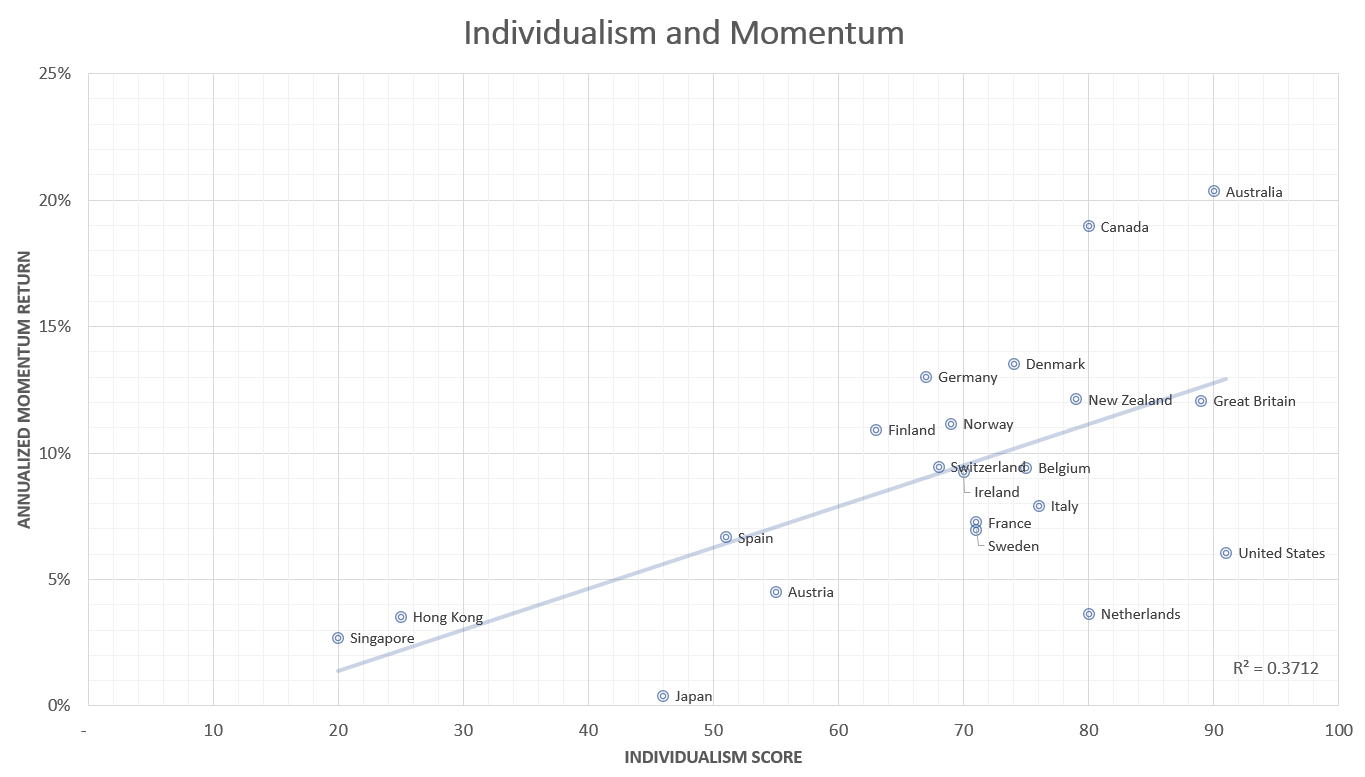

I decided to replicate the authors’ findings myself by downloading Hofstede’s data and comparing it to factor returns data provided by AQR (the UMD factor). Below I plot the relation between the individualism score and the average annualized returns to a long-short momentum strategy between 1987 and 2016 for a sample of 20 developed market countries.

Interesting… So if you’re reading this post in your native language, you may want to reconsider when deciding to buck the trend with your investments (unless you’re Hong Kongese or Singaporean, then you’re probably fine).

The intersection of culture and investor behavior is rich and underexplored vein of research, and one I will probably be returning to in future posts. Stay tuned!

Disclosures: This post is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place. Please contact us at your earliest convenience with any questions regarding the content of this post. For actual results that are compared to an index, all material facts relevant to the comparison are disclosed herein and reflect the deduction of advisory fees, brokerage and other commissions and any other expenses paid by RHS Financial, LLC’s clients. An index is a hypothetical portfolio of securities representing a particular market or a segment of it used as indicator of the change in the securities market. Indexes are unmanaged, do not incur fees and expenses and cannot be invested in directly.

2024 Disclosures

RHS Financial is an SEC registered Investment Advisory Firm and distributes this presentation for informational purposes only. This presentation ( hitherto referred to as the presentation throughout this disclosure), blog post, infographic, slide deck or whatever form of informational modality the reader wishes to describe this as is provided for informational purposes only and should not be construed as investment advice in any way.

We believe the information, including that obtained from outside sources, to be correct, but we cannot and do not guarantee its accuracy in any way. RHS Financial uses information from outside sources to develop graphs, charts, infographics, etc. to enhance this presentation and while we believe the information from these outside sources, to be correct, we cannot and do not guarantee its accuracy in any way,

Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors who may be employees of but do not necessarily reflect the views of RHS Financial as a company. There can be no guarantee that developments will play out as forecasted. The information in this presentation is subject to change at any time without notice. This presentation contains “forward-looking statements" concerning activities, events or developments that RHS Financial expects or believes may occur in the future. These statements reflect assumptions and analyses made by RHS’s analysts and advisors based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond RHS Financials’ control, they are no guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements. In a nutshell; these are our best guesses and please don’t assume they are fact.

Mentions of specific securities, investment products, investment indices, companies or industries should not be considered a recommendation or solicitation. Data and analysis does not represent the actual or expected future performance of any investment or investment product Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This post may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with RHS Financial and does not sponsor, endorse or participate in the provision of any RHS’ services, or other financial products. Index information contained herein is derived from third parties and is proffered to you unaltered as we derived it from the third party.

RHS Financial, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where RHS Financial, LLC and its representatives are properly licensed or exempt from licensure. This presentation is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place.

If the client is deemed suitable and agrees, RHS may employ leveraged strategies for these clients. Leverage attained through margin on a client’s account can add additional risk. While RHS tends to seek to improve return with theses strategies by applying leverage to less risky indexes, there is no guarantee that that RHS will lower risk or improve returns.

RHS Financial. 4171 24th St. Suite 101 San Francisco, CA 94114