2022: Bad Beta, Good Alpha

It’s a new year, 2022 is behind us, and good riddance as far as many investors are concerned. As inflation soared to multi-decade highs, war broke out in Europe, and the world’s second-largest economy remained in lockdown, financial markets around the world recoiled and shed trillions of dollars of investor wealth. 2022 was the worst year for stocks since the 2008 financial crisis. Even more incredibly, 2022 may very well have been the worst year ever for bonds. The standard benchmark for the US bond market, the Bloomberg Aggregate Bond Index, was down 13% in 2022, its worst year by far since the index’s inception in 1976 (the second worst year was 1994 with a 2.9% loss). If we look back further, Ibbotson Associations maintains an index of long-term treasury bonds that goes back to 1926. The 2022 loss on that index was the all-time worst as well! (Long-term treasuries, which are more volatile than the rest of the market, were down 26.1% in 2022 versus 14.9% for the next-worst year, 2009.)

Normally stocks and bonds aren’t very correlated with each other, and they rarely lose a lot of money together, so 2022 was shockingly bad for investors holding conventionally diversified stock-bond portfolios. If we look at a scatterplot of the annual returns of US stocks versus US bonds (long-term treasuries) over the long run we see just what an outlier 2022 was.

So whether you were an aggressive investor holding mostly stocks, a conservative (or so you thought!) investor holding mostly bonds, or a moderate investor holding the gold-standard 60/40 portfolio, 2022 was probably an unprecedentedly bad year for you if you were broadly diversified across markets. In the finance biz we call returns associated with purely being exposed to markets overall “beta”. 2022 was a really bad year for beta. The silver lining was that for investors following some of the most well-established active investment strategies such as value investing and trend following (strategies we talk about a lot here at RHS Financial), 2022 was a year of redemption for them, strongly outperforming in 2022 after a handful of years of floundering. Alpha, the returns associated with picking the better investments within the market and/or timing its entry and exit, was really good in 2022 for systematic active investors, and cushioned the blow of bad markets overall. So 2022 was a mixed bag for disciplined, diversified investors: bad beta, good alpha. Let’s look at these more closely, bad news first.

Bad Beta

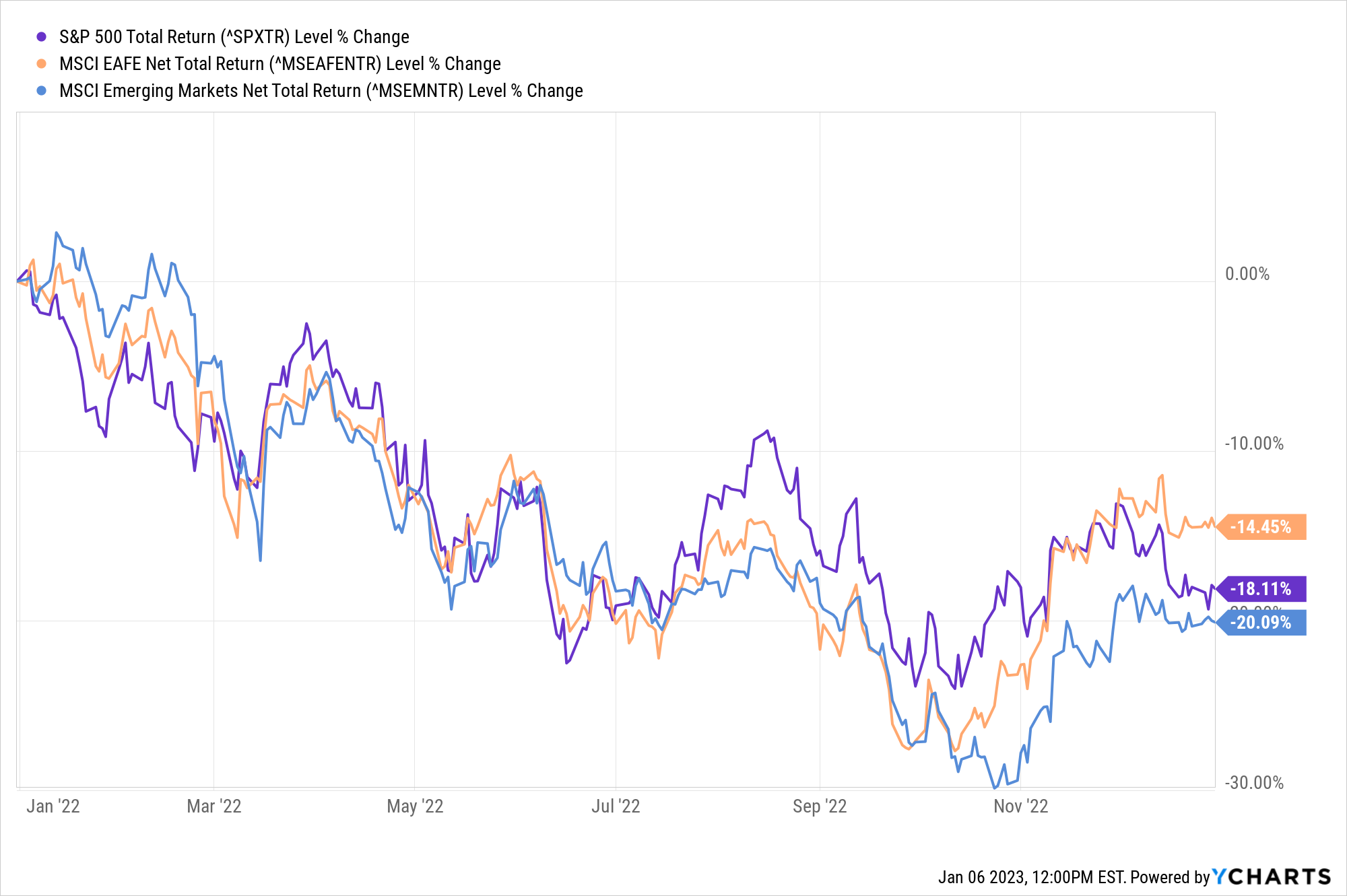

Almost every major asset class around the world was down in 2022, no matter where in the world you looked. Starting with stocks, below we see the 2022 returns for the S&P 500 index of US Stocks, MSCI EAFE (international developed markets), and MSCI Emerging Markets.

Data by YCharts

All of the world’s major stock markets followed each other down the same bad path in 2022. Stock markets are generally pretty correlated with each other so this isn’t too surprising in itself, but given the variety of different economic news coming out of different regions it is interesting how much it all amounted to the same. The collapse of the tech bubble in the US, the energy crisis in Europe, and the COVID lockdowns in China would seem to be mostly unrelated events that would affect each region in its own way, and if we drill down to certain specific companies and industries it did, but in the aggregate it all added up to bad news bears no matter where you looked.

Bonds fared little better. As inflation spiked across the globe the central banks of the world found it necessary to start raising their policy rates at the fastest pace we’ve seen in nearly 50 years, clobbering bond prices as a result. Below we see the turns for US treasury, investment grade corporate, and high yield corporate bonds, as well as an index of bonds of international developed markets.

Data by YCharts

Foreign bonds suffered the worst in 2022 as the dollar appreciated against basically every other currency in the world. High yield bonds, which are typically considered the most risky segment of the bond market, was interestingly one of the segments least badly hurt last year. High yield (or “junk”) bonds are less interest rate sensitive but depend more on the creditworthiness of their issuers, which, despite deteriorating economic conditions, did not suffer quite as much over the year.

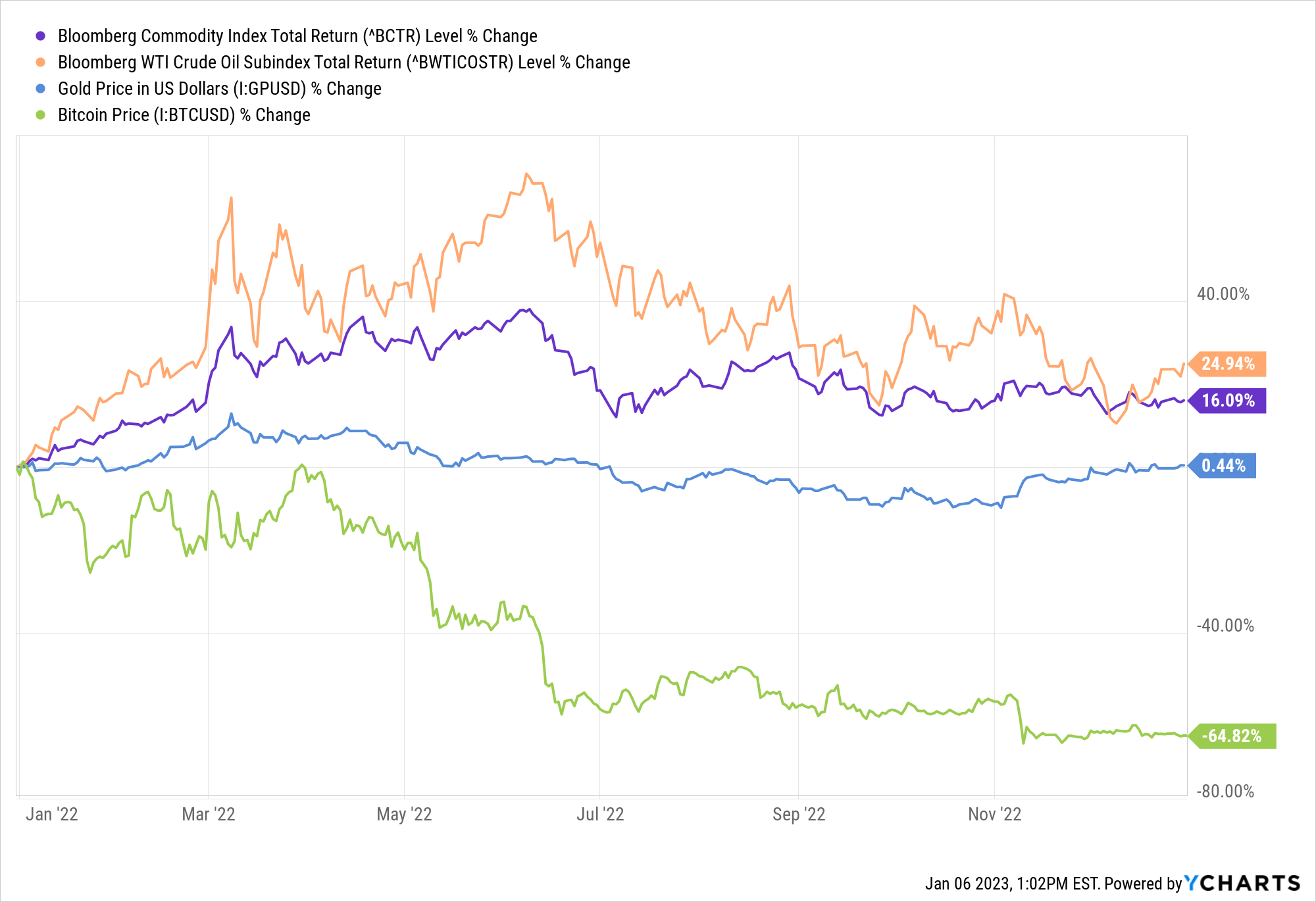

About the only major asset class that did well last year was commodities, not surprising in a year where high inflation dominated the economic headlines. But even here it was a mixed bag and depended on your definition of the commodities market. The commonly benchmarked Bloomberg Commodity Index, which balances allocations across energy, agricultural, and metals commodities roughly evenly, was up about 16% in 2022.

But commodity index performance was driven mostly by the meteoric rise in the price of oil and other fuels, something you may have noticed if you drove a car at any point last year. Somewhat surprisingly, gold – which, in terms of investment dollars allocated to it, is by far the world’s most important commodity – went nowhere over the course of the year, meaning of course that it lost value after inflation. A caveat here is that because the dollar appreciated so much over other currencies, the price of gold denominated in other currencies like the euro or yen rose quite a lot, making gold one of the best investments last year for e.g., Japanese or European investors. Still, it was a disappointing showing for an asset often held specifically for its supposed inflation-hedging qualities. Other commodity groups like agricultural products and industrial metals had similarly near-zero returns.

The “commodity” that had by far the worst performance and arguably the worst major asset class overall for 2022 (besides Russian stocks) was Bitcoin, losing about 65% and erasing nearly all its gains since its last major run-up in 2020. This is an embarrassing result for an asset that is explicitly touted by its proponents as a way to protect against inflation. While in earlier years Bitcoin showed little to no correlation with other assets and looked potentially interesting as a diversifying asset, it increasingly just looks like a high-risk speculative asset that can go up a lot when times are good but crashes even more when times are bad.

What Gives?

We’ve talked to many investors over the last several months who’ve been frustrated and exasperated at this turn of events. For years investors have been told that diversifying across stocks and bonds would protect against major drawdowns. Investors have gotten used to the idea that not only are bonds less volatile than stocks, they’re a safe haven asset for when stocks hit the wall, outperforming during equity bear markets and cushioning their blow, as they did in the dot-com bust, the financial crisis, and the COVID crash. 2022, in contrast, saw the 60/40 portfolio fall nearly as much as being invested purely in stocks, leading to many a popular finance article proclaiming the death of 60/40.

So what happened? Not surprisingly, inflation is a big part of the story here. Stocks, bonds, and commodities all have different fundamental relationships to inflation and how their returns vary with respect to each other will depend on where inflation is compared to expectations and perceptions of whether inflation risk is high or low. Most obviously, commodities on average tend to benefit from inflation, almost by definition, as inflation is the phenomenon of “too much money chasing too few goods”, and commodities are the basic constituents of the goods in our economy. Equivalently, commodity investments tend to suffer during lower-than-expected inflation or deflation. Bonds are the mirror image of this: as fixed claims to a certain number of dollars (or other currency), they lose value as more dollars are printed and dollars get devalued, but benefit during periods of deflation (as long as the issuer is still able to keep servicing their debt!). Stocks are somewhat more complicated. Because the value of a stock is ultimately derived from its profits, and inflation should increase a firm’s revenues roughly in line with its costs on average, you might think that inflation shouldn’t have any effect on stock returns. And indeed stocks are generally less sensitive to inflation than either bonds or commodities, but the problem comes when when things go too far off the rails in one direction or another. Financial markets are always graded on the curve of expectations. Firms, households, and other economic actors plan their behavior using some baseline expectations of where prices are going to be in the near future; if these expectations end up being significantly off the mark, it can be disruptive and make it difficult to act strategically. Because inflation does not spread uniformly and instantaneously through the economy but in fits and spurts, relative price differences tend to be very volatile when inflation is much higher (or lower) than expected, and this is inherently difficult for firms to adapt to and tends to hurt profitability. Indeed profit margins for S&P 500 companies declined throughout 2022.

To illustrate this point, let’s look at what average stock, bond, and commodity returns have been in periods when inflation is surprisingly high versus surprisingly low. To do this I collected average annual returns for US stocks, (treasury) bonds, and commodities since 1926, then constructed a measure of “surprise” inflation, which I defined as the inflation rate of the year in question minus the inflation rate of the previous 10 years. I then graphed what returns were on average in each of these markets when surprise inflation was -3% or lower (Surprise Low Inflation), +3% or higher (Surprise High Inflation), as well as the full sample period covered. (Note that these are arithmetic averages and so don’t correspond exactly to compound returns, which would be somewhat lower.)

We can see that both stocks and bonds do better when inflation is lower rather than higher than expected, and the effect is much stronger in bonds. Commodities show the opposite relationship, and the strongest effect of all. I was actually surprised to see stocks did slightly better in the surprise low inflation environment than the full sample average, because deflationary shocks are associated with some of history’s worst bear markets, including the Great Depression and the ’08 financial crisis, but it turns out we’ve had more episodes in the last century of US history of inflation falling from too-high into the goldilocks zone than we’ve had of it falling from the goldilocks zone into deflation.

So what we generally see is that when inflation is dramatically and surprisingly high stocks and bonds are highly correlated to each other and both perform badly, while commodities are negatively correlated to stocks and perform well. In deflationary episodes this relationship flips as stocks and bonds move opposite each other while stocks and commodities become correlated and suffer together (bonds and commodities are almost always negatively correlated to each other).

Over the last forty years inflation has steadily fallen across the developed world, to the point that by the mid-2010s the concern among macroeconomists was that it was too low and we might not be able to get it back up again. Against this backdrop, stock-bond correlations fell as well, and had been consistently negative since the turn of the century, and especially after the financial crisis. Many investors began to treat this inverse relation as a law of nature. So the sharp spike in inflation in late 2021 through 2022 was a shock to many peoples’ expectations, indeed. As I write this, the year-end inflation figure for 2022 isn’t out yet, but as of November, year-over-year inflation in the US was 7.11%, versus just 2.02% over the previous 10 years.

So inflation in 2022 was a major shock that unsurprisingly hurt both stocks and bonds. Add to this the fact that both stocks (at least in the US) and bonds (across the developed world) were both very expensive relative to historical valuations going into 2022, and so they each potentially had a long way to fall. Throw in a dash of geopolitical tumult and supply-side disruption and you have a recipe for a historically bad year for beta.

So should investors hold more money in real assets like commodities to protect against years like 2022? Maybe. Most individual investors have no direct allocation to commodities whatsoever, and they are not commonly found in asset allocation products used in 401(k) plans such as target retirement funds. Studies suggest that adding allocations to physical gold and commodity futures can improve the risk-return efficiency of a stock-bond portfolio, and we at RHS Financial often recommend small strategic and/or tactical allocations to such investments. “Small” is a key word here, though. The commodities market itself is much smaller in size than stock and bond markets and it would not be possible for investors in aggregate to shift their portfolio substantially in their direction. Nor would they want to; commodity investments have earned lower long-term returns than either stocks or bonds, despite being the most volatile of the three, and they often go decades at a time making no money at all before finally having a windfall year. Their value comes almost entirely from their upside potential during rare inflation shocks.

On the other hand, many systematic active strategies commonly used by quantitative investors are robust to or even benefit from macroeconomic volatility, and 2022 was a year in the sun for them.

Good Alpha

Data-oriented investors with an eye for exploiting market inefficiencies often gravitate to a handful of systematic active strategies to try to earn alpha: returns in excess of those attributable purely to exposure to broad-based markets. I’ve often discussed such strategies on this blog and they are often employed by hedge funds. 2022 delivered heaps of alpha to many of these systematic active strategies, cushioning the blow of bad beta returns for investors who used them. Indeed, hedge funds were basically flat for the year, as judged by the 0.53% YTD return on the commonly benchmarked HFRI as of November. Half a percent of return isn’t usually something to get excited about, especially when inflation was about 7%, but compared to double-digit losses in stocks and bonds it’s a home run, and considering that most hedge funds have some embedded market exposure, a flat year is impressive. If we strip out that beta exposure and focus only on the alpha component, returns in 2022 for these strategies was very strong, as we’ll see.

This is great news for quant investors because many of these strategies struggled over much of the previous several years (something I’ve documented on this blog before), leading many investors to lose faith and throw in the towel. But 2022 paid off for patient investors who held on. I’ll focus here three of my favorite strategies: value, low-volatility, and trend-following. Each of these strategies has delivered positive alpha over the long run (decades or even centuries) for investors, had disappointing returns over the several years prior to 2022, but strongly outperformed last year.

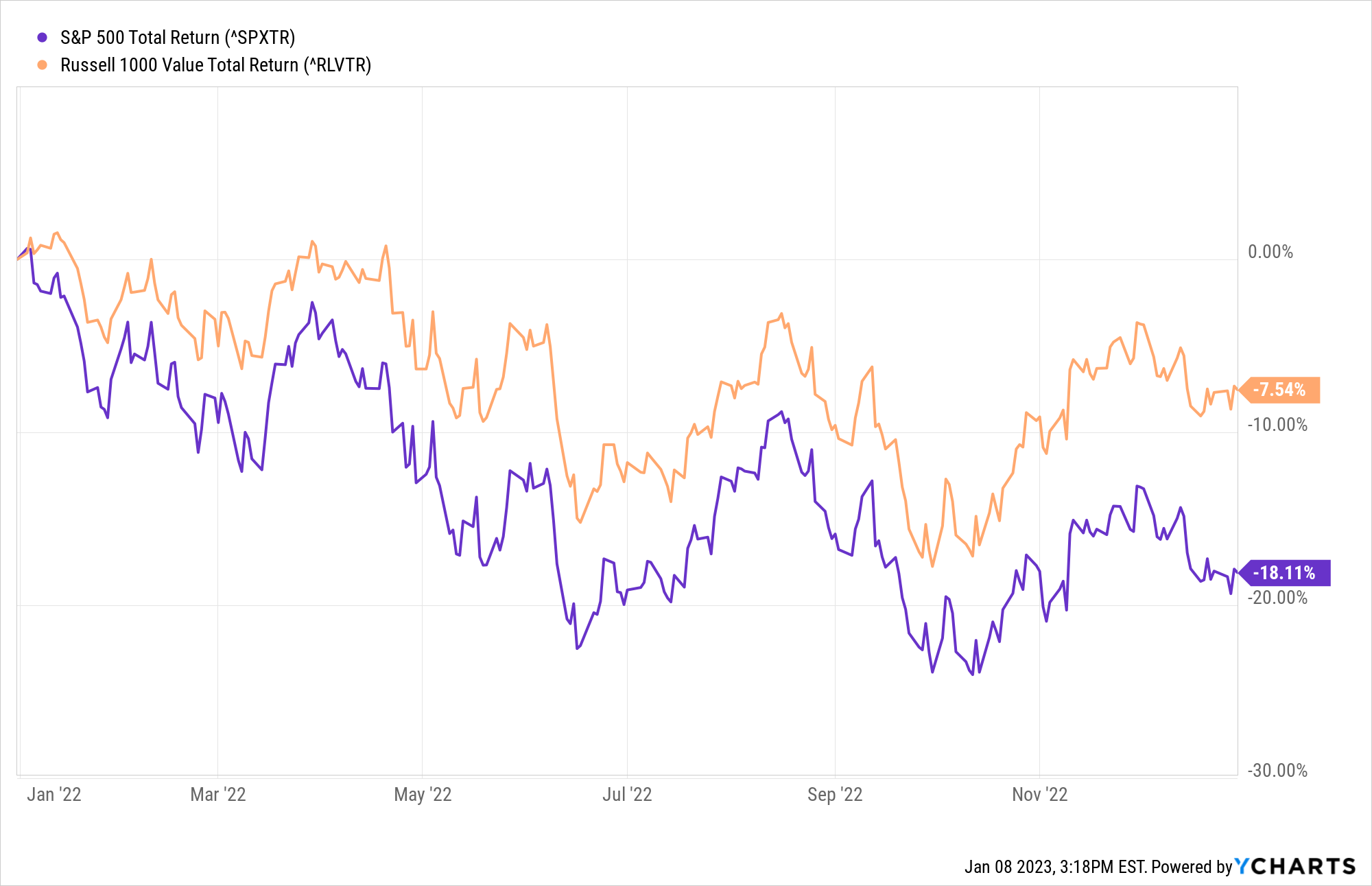

The success of value investing – or maybe rather the failure of its opposite and the spectacular implosion of the most speculative growth sectors of the market – was one of the biggest stories in the market last year. Overvalued companies in the tech sector, which powered much of the post-2009 bull market, blew up in 2022, while more modestly priced stocks trudged along with only slightly-negative returns for the year. Observe the difference between the S&P 500 and the Russell 1000 Value index.

Data by YCharts

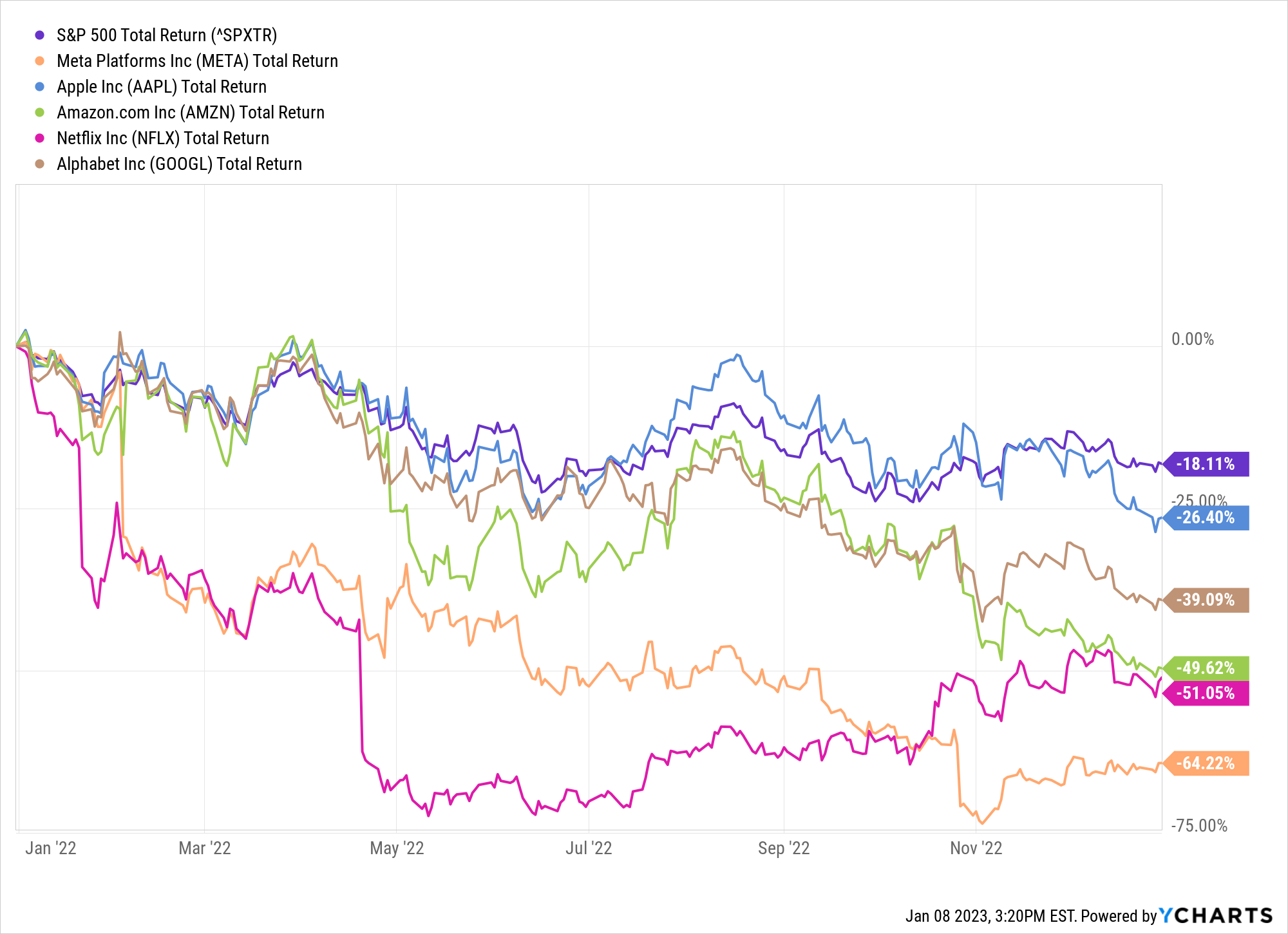

Now compare this to the performance of the famous FAANG stocks which were the darlings of the market over the previous decade. Each lost anywhere from a quarter to two-thirds of their value in 2022.

Data by YCharts

And the FAANG stocks were among the most well-established and relatively safe in the speculative growth space. Many of the smaller and newer growth companies that were so popular with retail investors during the COVID boom period were decimated in 2022. The Renaissance IPO index and corresponding ETF was down about 57% in 2022. The popular ARK Innovation ETF helmed by the famous Cathie Wood lost 67% (!) over the year.

I have particular reason to crow about this turn of events. In August 2020 I wrote a couple of blog posts calling out the US stock market in general and the growth/tech segments in particular as in a bubble. I was a little early as the US market continued to rally through 2021 and value and growth kept up neck and neck. But as of the end of 2022 value stocks have since trounced over the rest of the market since I wrote that piece, and the NASDAQ is now underwater, as are the FAANGS and almost all the other speculative growth names in the market. Granted, I didn’t predict that the much more undervalued foreign stock markets would fall just as much as the US, but you win some, you lose some.

So how much did value investors outperform in 2022? There are many different indexes that attempt to capture the returns of value strategies, such as the Russell 1000 Value depicted above, each with somewhat different specifications, and there are many different markets it can be applied to as well. To get a sense of what might be representative of diversified value investors, I gathered returns on a couple different popular value stocks indexes in each of the three major stock market regions: the US, foreign developed, and emerging markets. I then subtracted the returns of the respective underlying benchmark markets from these indexes to isolate the value-add or “pure” alpha of the strategy. I then averaged these all together to get a composite global value equity strategy. Here’s how it looked:

Globally diversified value stock strategies outperformed by roughly 8% last year with very little volatility (the Sharpe ratio for the year was 2.0 under this methodology, extremely high by historical standards).

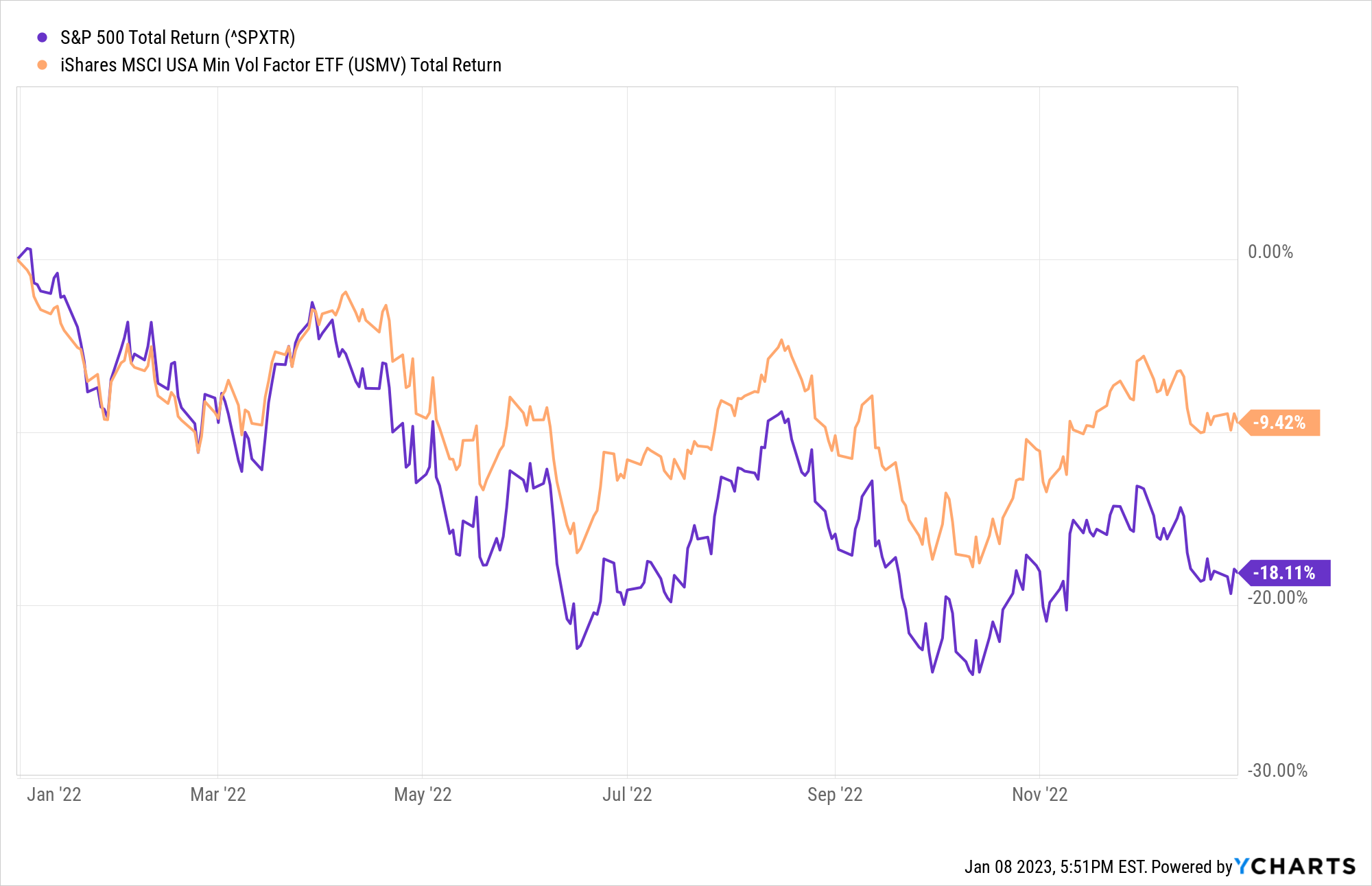

Another equity strategy that did very well in 2022 was low-volatility investing. Low-volatility strategies, as the name suggests, involve overweighting stocks (or assets generally) that are among the least volatile or overall risky in the market. Historically, low-volatility stocks have earned long-run returns about the same as the overall market, but with (not surprisingly) less volatility, which means that these strategies have historically earned superior risk-adjusted returns than the overall market. Intuitively, low-volatility stocks tend to trail behind their riskier peers during red-hot bull markets, but then lose less ground during downturns. And they delivered as promised on that goal in 2022. Consider the performance of the popular low-volatility ETF, USMV, verses the S&P 500:

Data by YCharts

We can see that USMV generally lost slightly less ground during each of the market’s dips last year, which added up to over 10% of outperformance.

Similar to value above, I collected a couple different low-volatility stock benchmarks in each of the three major markets, stripped out their market returns, then averaged them together for a composite global low-volatility strategy.

Similar to value, this construction of the low-volatility strategy outperformed by about 8% in 2022, albeit with slightly-lower-but-still-great risk-adjusted returns (the Sharpe ratio was 1.2).

Finally, another systematic active strategy that performed great last year was trend-following. Trend-following is a form of momentum strategy that entails buying asset classes whose recent short-term performance has been positive and selling those whose has been negative, predicated on the notion that investors are often too-slow to react to news and therefore prices do not always immediately adjust but follow “trends” over short intervals (on the order of months). The most popular implementations of trend-following are “managed futures” strategies, which use futures markets to go long or short different markets, generally across all the major asset classes: stocks, bonds, commodities, and currencies. Managed futures funds are one of the most popular categories of hedge fund and alternative mutual fund due to their history of providing not just strong absolute returns but excellent protection during major bear markets. Despite treading water for most of the previous decade, managed futures (and trend-following generally) strategies pulled through in 2022.

Here, because there are fewer indexes to choose from, I simply depict the Credit Suisse Managed Futures Liquid Index, a common benchmark among managers in the space.

The Credit Suisse index was up a whopping 22% in 2022. This looks to be broadly representative of what live funds in the space earned as well, making managed futures funds one of the best investments investors could hold last year, even better than long-only diversified commodity futures (note that because trend-following has a much higher volatility than the composite value and low-volatility strategies depicted above its risk-adjusted return was still actually between them, with a Sharpe ratio of 1.5).

These three classic active strategies are each based on very distinct concepts and constructed very differently. Despite all three of them having a somewhat similar “shape” to them over the year, their correlations to each other over 2022 were close to zero, consistent with what we’ve seen historically, while their correlation to the market was negative. This means they have great value as diversifiers and is why, in addition to alternative assets like commodities, we continue to recommend systematic active strategies with a long history of success as a means to smooth out the ride offered by just stocks and bonds alone.

What’s Next?

Unless you had all your money tied up in crude oil futures, 2022 was probably a bad year in investing for you. Now what? If you’re a long term investor, this bad year is actually good news for you. With the stock/bond rout, yields on nearly all assets are now higher, which means they actually have greater wealth-generating capacity than they did a year ago, even taking the loss of principal into account. Next week I will dive into this counterintuitive result and explain the good news about bad markets. Until then, stay invested!

2024 Disclosures

RHS Financial is an SEC registered Investment Advisory Firm and distributes this presentation for informational purposes only. This presentation ( hitherto referred to as the presentation throughout this disclosure), blog post, infographic, slide deck or whatever form of informational modality the reader wishes to describe this as is provided for informational purposes only and should not be construed as investment advice in any way.

We believe the information, including that obtained from outside sources, to be correct, but we cannot and do not guarantee its accuracy in any way. RHS Financial uses information from outside sources to develop graphs, charts, infographics, etc. to enhance this presentation and while we believe the information from these outside sources, to be correct, we cannot and do not guarantee its accuracy in any way,

Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors who may be employees of but do not necessarily reflect the views of RHS Financial as a company. There can be no guarantee that developments will play out as forecasted. The information in this presentation is subject to change at any time without notice. This presentation contains “forward-looking statements" concerning activities, events or developments that RHS Financial expects or believes may occur in the future. These statements reflect assumptions and analyses made by RHS’s analysts and advisors based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond RHS Financials’ control, they are no guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements. In a nutshell; these are our best guesses and please don’t assume they are fact.

Mentions of specific securities, investment products, investment indices, companies or industries should not be considered a recommendation or solicitation. Data and analysis does not represent the actual or expected future performance of any investment or investment product Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This post may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with RHS Financial and does not sponsor, endorse or participate in the provision of any RHS’ services, or other financial products. Index information contained herein is derived from third parties and is proffered to you unaltered as we derived it from the third party.

RHS Financial, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where RHS Financial, LLC and its representatives are properly licensed or exempt from licensure. This presentation is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place.

If the client is deemed suitable and agrees, RHS may employ leveraged strategies for these clients. Leverage attained through margin on a client’s account can add additional risk. While RHS tends to seek to improve return with theses strategies by applying leverage to less risky indexes, there is no guarantee that that RHS will lower risk or improve returns.

RHS Financial. 4171 24th St. Suite 101 San Francisco, CA 94114