SBA Small Business Loans and Alternative Sources for Cash Strapped Business Owners

The Novel Coronavirus has affected the world’s economy and business owners in a tremendously staggering way. Government mandates for sheltering in place and requiring only “Essential Businesses” to operate have forcibly put many business operations on pause. These businesses no longer have revenues and as a consequence, they are laying off their employees at a record pace. In the four weeks following March 14, 22 Million Americans filed for unemployment, and more locally, 2.7 Million Californians filed for unemployment. These staggering numbers of unemployed are exactly what the Federal Government wanted to avoid when it developed the business-focused side of the CARES Act.

In this post, I want to outline the three types of loans that were available to businesses through government programs and what happened during the application process. As these loans were dramatically oversubscribed, many if not most of the business owners who applied will likely not receive these government-backed preferential loans. I will outline several other options business owners can tap in order to keep their businesses afloat.

CARES Act Small Business Rescue Package Loans

The CARES Act is a bi-partisan bill that was passed on March 27th and was designed to help individuals and businesses survive in the wake of the COVID-19 epidemic. The bill had multiple provisions designed to help businesses borrow money at either low or essentially free as long as they used the money to retain employees. The rollout of this plan was intended to be immediate, but it has been fraught with problems and difficulties. Effectively, there are two loan programs in the CARES Act.

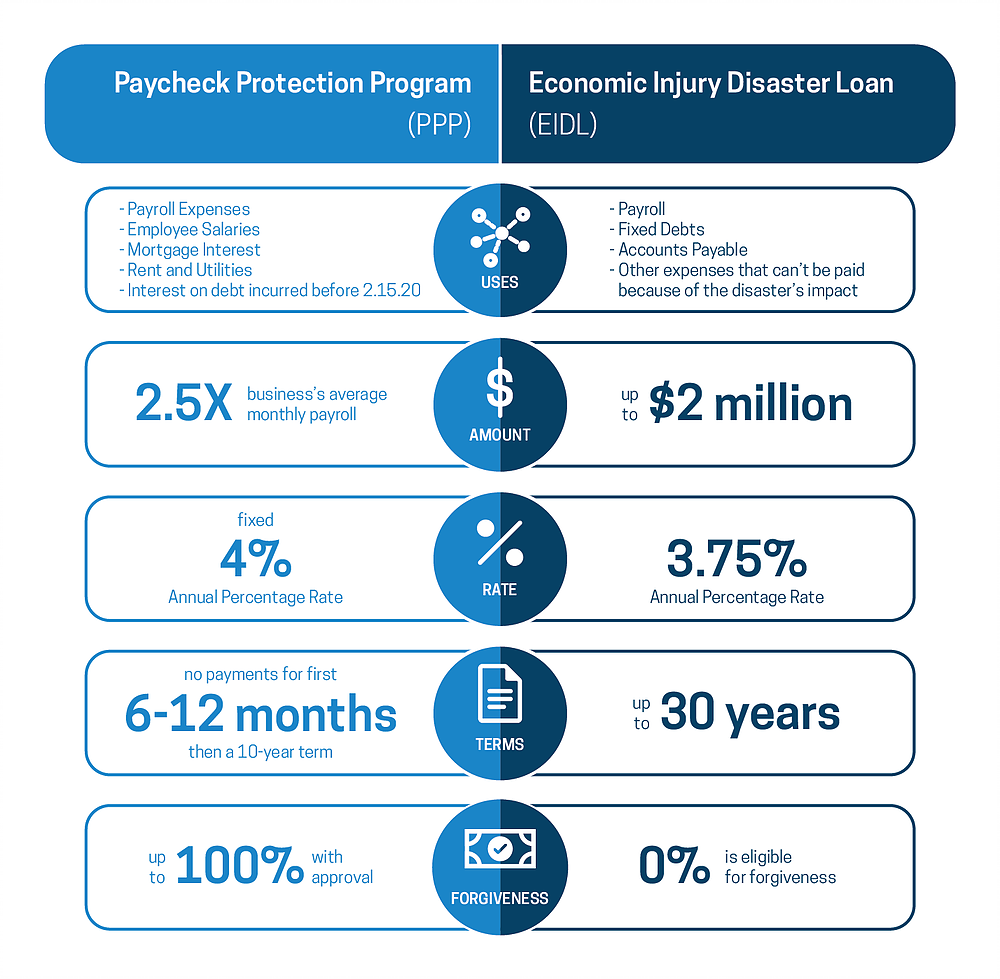

The first is through the SBA and it is called the Economic Injury Disaster Loan (EIDL).

The second program, also through the SBA is called the Paycheck Protection Program and it specifically requires employers to use the money to keep employees employed. Both loans were designed to help small businesses (under 500 employees) and each has its own parameters.

Also, the Federal Reserve developed a newer loan program on April 9th called “Mainstreet” that targets firms with 500 -10,000 employees. For a quick synopsis of the first two loans please review the infographic below.

Source: HD CPA

Source: HD CPA

There are numerous great very detailed sources of information on the web about these two types of loans but the simplest way to look at the differences is how they are structured.

An EIDL loan is much more like a traditional loan at a phenomenal long-term interest rate but it requires the business owner to have collateral and the requirements are more stringent.

The Paycheck Protection Program is effectively a grant from the government because up to 100% of the loan can be forgiven if the business owner keeps his/her employees on payroll. Given the forgivable nature of this loan, it was wildly popular and was oversubscribed by a great number of applications.

Big banks like Wells Fargo and Chase sent numerous emails out to business owners who applied for but did not receive funding on Friday the 17th of April letting them know they ran out of funds for the program and were unable to help. Both Chase and Wells Fargo were unable to accept applications until days after the program started and all applications were submitted online for the Paycheck Protection Program. Sources on the web say that most business owners submitted their applications but never heard anything back until they were notified on Friday, April 17th that they were denied.

According to the San Francisco Business Times, the 349 Billion dollar fund was exhausted by Thursday, April 16th. This leaves thousands of business owners scrambling for alternative methods to keep their businesses cashflow positive during these unprecedented times. According to the NFIB, only 20% of the PPP applications were funded, leaving the remaining 80% of business owners who did not get the loans and do not know where they stand in the process scrambling for alternative ways to fund their impending expenses with little or no revenue coming in.

Source NFIB Survey

Source NFIB Survey

The good news for many of the business owners who did not get funded in the first round, the Senate voted on Tuesday, April 20th on a bill that created a second round of funding for the PPP and EIDL where an additional 320 Billion is allotted to the popular Paycheck Protection Program. Congress is slated to vote and pass this measure on Thursday the 23rd of April and President Trump has said in a tweet he would sign it.

So help is likely on the way, the bad news is that if the first 350Billion covered only 20% of the applicants, will the additional 320Billion cover the remaining 80% of businesses that did not receive the first loan? It is my belief that it will not. Furthermore, if you are a business that is planning on submitting an application now, I believe that your chances of getting funded in the second round with such a large queue in front of you are slim to none. So what is a business owner to do and what are some of the alternatives available to business owners right now that they can tap in these uncertain times?

Alternative Sources for Cash Strapped Business Owners

The first thing business owners and executives need to do is revisit their cash flow forecast statements and figure out worst-case scenarios over the next 12 months. This will give the business owner a number that they will need to borrow to keep operations afloat.

Now that the business owner has a number, then review alternative funding options other than using a business owner’s personal savings to fund the business from best to worst. By the way, we do not endorse using the business owner’s personal savings to fund the business unless it is necessary. Unfortunately, this strategy tends to be the default strategy as it is easy but it should be avoided if at all possible.

Traditional Alternatives

The first alternative funding option is tapping existing business credit lines if you have them.

The second is to apply for a traditional SBA loan which is hard to get and may take too long in today’s environment to save your business.

Margin Loans

A very attractive alternative for business owners with large portfolios in non-retirement accounts is a margin loan from your brokerage firm.

Firms like Interactive Brokers have margin loan rates as low as 1.5% on brokerage account balances over 1 million. This may seem like a risky strategy to borrow against your portfolio, but it is a very inexpensive and fast way to get access to capital cheaply.

The chief benefit of this strategy is that you get to keep your money in the market, you don’t have to sell any securities or pay taxes on your gains and if the market recovers you get to participate in the upside all while borrowing at cheap rates to keep your business afloat.

If you are interested in this strategy, contact us, RHS Financial may be able to help you out.

Home Equity Line of Credit

The fourth and very often used option is the Business owner can take out a Home Equity Line of Credit to fund ongoing operations. Obviously, this route really puts a great deal of stress on the business owner by leveraging the value of their personal residence, but they are easy loans to get and at today’s low-interest rates, they can be quite attractive as a bridge loan.

For borrowers with very good credit, HELOC lenders charge a point or so over the prime rate, meaning this form of money is available for as little as 4.25 percent. Borrowers with riskier profiles, such as lower credit scores or higher loan-to-value ratios, might pay 1.5 or 2 points above prime.

Don’t ask Chase for a Home Equity Line of Credit, however, as of April 16, in the wake of the uncertainty caused by the Coronavirus Chase has stopped accepting new HELOC applications and I would not be surprised if other banks end up doing the same.

Working Capital Term Financing

If you are looking to pay off vendors only, you may qualify for Working Capital Term Financing. Working Capital Terms are specifically provided for customers to pay off their vendor invoices, with the idea that this will free up cash to use on other parts of the business. Funds will be deposited directly into the vendors’ accounts in as little as two days according to American Express.

Whole Life Insurance Cash Value

Finally, if you have permanent (not term) life insurance, you may have a cash value in your policy you can borrow against in order to fund your business in the short-term. This is a more common practice than you might think. Contact your insurance broker for more information on this strategy.

If You Have No Other Options

There are two final options that we do not recommend but are available to many business owners. Both options are pitfalls that can leave the business owner in worse shape than they already are and may hasten their financial ruin.

401k Loans

Borrowing money from your 401K may sound like a great idea but it is generally an unbelievably bad one. The CARES act of 2020 allows people to borrow up to $100,000 from their 401K and pay it back in 3 years without penalty. You can read all about it in RHS Financials’ previous post titled A Guide to the Stimulus Package for COVID-19 for Individuals and Families. Basically, as a business owner, you are raiding your personal retirement savings to save your business. If your money is out of the market and in your business you will miss any potential recovery in the market in your retirement fund. A potential double whammy to you if your business doesn’t make it.

Credit Cards

Many entrepreneurs started their business with credit cards and planned never to use them again, but desperate times call for desperate measures. Due to the incredibly high-interest rates credit cards charge for carrying a balance, we recommend that you do not take this route and take the time to explore the options I listed earlier. They will be better for you in the long run.

2024 Disclosures

RHS Financial is an SEC registered Investment Advisory Firm and distributes this presentation for informational purposes only. This presentation ( hitherto referred to as the presentation throughout this disclosure), blog post, infographic, slide deck or whatever form of informational modality the reader wishes to describe this as is provided for informational purposes only and should not be construed as investment advice in any way.

We believe the information, including that obtained from outside sources, to be correct, but we cannot and do not guarantee its accuracy in any way. RHS Financial uses information from outside sources to develop graphs, charts, infographics, etc. to enhance this presentation and while we believe the information from these outside sources, to be correct, we cannot and do not guarantee its accuracy in any way,

Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors who may be employees of but do not necessarily reflect the views of RHS Financial as a company. There can be no guarantee that developments will play out as forecasted. The information in this presentation is subject to change at any time without notice. This presentation contains “forward-looking statements" concerning activities, events or developments that RHS Financial expects or believes may occur in the future. These statements reflect assumptions and analyses made by RHS’s analysts and advisors based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond RHS Financials’ control, they are no guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements. In a nutshell; these are our best guesses and please don’t assume they are fact.

Mentions of specific securities, investment products, investment indices, companies or industries should not be considered a recommendation or solicitation. Data and analysis does not represent the actual or expected future performance of any investment or investment product Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This post may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with RHS Financial and does not sponsor, endorse or participate in the provision of any RHS’ services, or other financial products. Index information contained herein is derived from third parties and is proffered to you unaltered as we derived it from the third party.

RHS Financial, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where RHS Financial, LLC and its representatives are properly licensed or exempt from licensure. This presentation is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place.

If the client is deemed suitable and agrees, RHS may employ leveraged strategies for these clients. Leverage attained through margin on a client’s account can add additional risk. While RHS tends to seek to improve return with theses strategies by applying leverage to less risky indexes, there is no guarantee that that RHS will lower risk or improve returns.

RHS Financial. 4171 24th St. Suite 101 San Francisco, CA 94114