RSU Tax Rate Is Exactly The Same As Your Paycheck

One of the biggest benefits of working for a tech company is receiving equity. As a CFP, it is one of my favorite and most important topics to discuss. Your employer can pay equity in several ways. With each form of equity compensation, there are a variety of tax rules and strategies that you should consider.

Over the last few years, tech companies started to favor Restricted Stock Units(RSU) as the preferred form of compensation. In comparison to equity compensation such as Incentive Stock Options and Equity Stock Purchase Plans, RSUs have a straightforward tax implication for employees and founders. However, even with their simplistic nature, employees across the country are still having a hard time managing RSUs intelligently.

Perhaps the biggest challenge you will face is understanding how RSUs fit into your overall compensation. If you fail to have the proper perspective on RSUs you will fail to prioritize your personal goals. You will also stumble to make tax-savvy decisions.

There are two factors to consider when evaluating RSUs: how total compensation from RSUs is calculated and how the RSU tax rate is applied.

Amount You Get Paid, RSUs vs Salary

When we traditionally think about W-2 income we think of our salary and bonus. Your salary and bonus have two similarities and two differences with RSUs.

RSUs vs Salary Similarities

- How valuable does your employer think you are when they hire you? Your employer will grant you the number of shares it deems you are due based on your experience, skill set, and education. Your company could gift you additional shares if you get promoted or if they have a refresh in place.

- How long you decide to stay? RSUs act as golden handcuffs. You will get some of them and maybe all of them if you stay a predetermined amount of time. This creates the same effect as bonuses paid out quarterly or at the end of the year. This results in a trend of employees holding out for an extra few months to get an end-of-the-year bonus.

RSUs vs Salary Differences

- You receive shares instead of dollars. At every vesting period, you will receive a number of shares as dictated in your equity agreement.

- What do millions of market participants think your employer stock is worth? This is completely independent of your effort and sometimes even independent of how well the company is doing. Sometimes it is dependent on how well the whole market is doing. At the end of the day this deciding factor, one that you can’t even remotely control, will decide how much income you will get during each vesting period.

Unlike your salary and bonus, because of market swings, your income from RSUs is not promised nor can be controlled. You must avoid the mistake of associating the value of your RSUs at the time that you get hired with the amount you will actually be paid.

If you are still having a hard time making sense of RSUs reach out to your financial advisor.

RSU Tax Rate

The beauty of RSUs is in the simplicity of the way they get taxed. Unlike the much more complicated ESPP, they get taxed the same way as your income. RSUs are taxed as W-2 income subject to federal and employment tax (Social Security and Medicare) and any state and local tax.

End of story.

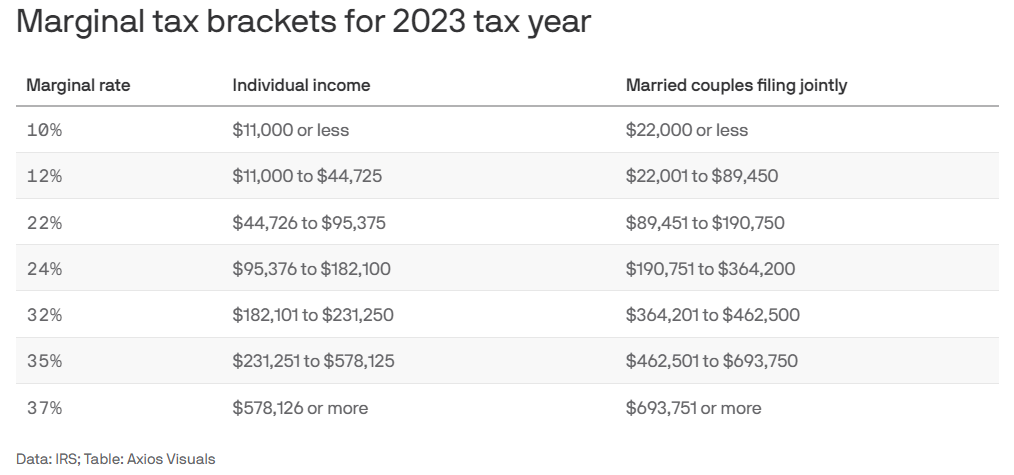

The timing of RSU tax is exactly the same as any other form of your W-2 compensation. On the date that your RSUs vest you will get shares net of the tax your employer withholds. Your employer will instantly sell a number of shares to cover taxes based on supplemental wage withholding. As with salary and bonus, at the end of the year, you will either owe more or get a refund. This over or underpayment will depend on all your other sources of income. This includes additional vested RSUs you receive throughout the year. Based on where you fall within the federal and state income tax brackets you will have your ultimate RSU tax rate.

For most, the supplemental wage withholding will not be enough. If that is the case, you will want to hold on to some cash to pay taxes on April 15th. If your RSU compensation is significant you may also consider paying quarterly estimated taxes. Calculating estimated taxes or getting the withholding right usually take the help of a professional.

RSU Double Tax

There is a second taxable event or at least a perception of an RSU double tax. This second tax event happens if you decide to hold your RSUs and then sell them for capital gain.

If you choose to hold those shares for less than one year, then any gain will be recognized as a short-term capital gain. If you hold on to them for a year and one day, then they will be recognized as a long-term capital gain.

While this may seem like an RSU double tax it is not.

You deciding to hold on to RSUs once they vest is the same as buying shares of any stock with your paycheck and then realizing a capital gain when you sell.

The real question you should be asking yourself is should you hold on to your RSUs once they vest? The answer isn’t as straightforward as you may think.

If you still find yourself wondering how to make sense of your RSUs and other equity compensation reach out to us. We are happy to offer you a free consultation to answer your questions and see if we can be of help.

Click HERE to get your questions answered.

2024 Disclosures

RHS Financial is an SEC registered Investment Advisory Firm and distributes this presentation for informational purposes only. This presentation ( hitherto referred to as the presentation throughout this disclosure), blog post, infographic, slide deck or whatever form of informational modality the reader wishes to describe this as is provided for informational purposes only and should not be construed as investment advice in any way.

We believe the information, including that obtained from outside sources, to be correct, but we cannot and do not guarantee its accuracy in any way. RHS Financial uses information from outside sources to develop graphs, charts, infographics, etc. to enhance this presentation and while we believe the information from these outside sources, to be correct, we cannot and do not guarantee its accuracy in any way,

Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors who may be employees of but do not necessarily reflect the views of RHS Financial as a company. There can be no guarantee that developments will play out as forecasted. The information in this presentation is subject to change at any time without notice. This presentation contains “forward-looking statements" concerning activities, events or developments that RHS Financial expects or believes may occur in the future. These statements reflect assumptions and analyses made by RHS’s analysts and advisors based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond RHS Financials’ control, they are no guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements. In a nutshell; these are our best guesses and please don’t assume they are fact.

Mentions of specific securities, investment products, investment indices, companies or industries should not be considered a recommendation or solicitation. Data and analysis does not represent the actual or expected future performance of any investment or investment product Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This post may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with RHS Financial and does not sponsor, endorse or participate in the provision of any RHS’ services, or other financial products. Index information contained herein is derived from third parties and is proffered to you unaltered as we derived it from the third party.

RHS Financial, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where RHS Financial, LLC and its representatives are properly licensed or exempt from licensure. This presentation is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place.

If the client is deemed suitable and agrees, RHS may employ leveraged strategies for these clients. Leverage attained through margin on a client’s account can add additional risk. While RHS tends to seek to improve return with theses strategies by applying leverage to less risky indexes, there is no guarantee that that RHS will lower risk or improve returns.

RHS Financial. 4171 24th St. Suite 101 San Francisco, CA 94114