Four Ways for Optimizing Your Executive Deferred Comp Plan

A non-qualified deferred compensation plan (NQDC) can be one of the better tax savings and planning tools a tech executive can utilize as part of your overall wealth management and retirement savings strategies. However, to maximize these deferred compensation plans, you need to understand their pros and cons so that you can effectively navigate many of the small decisions that in the end, could make a big impact on your financial future.

Sometimes called deferred retirement plans, (DC Plans, or DCPs), these plans are often offered to tech executives and highly compensated employees. These plans differ from 401k’s, which are governed by IRS rules. NQDC’s rules, such as how much you can contribute, when and how you can distribute, and who can participate, are set by your employer.

These deferred income plans can allow you to set aside massive amounts of income from your salary and bonus and frequently have a matching component, making them more attractive to participate in.

In today’s blog, we’ll look at four strategies that allow you to leverage your executive deferred compensation plans:

- Drop your tax bracket and invest tax-free.

- Control your income around key events such as bonuses, sales of assets, and exercising of stock options.

- Match your timing of distributions with short and long-term goals and career decisions.

- Use these plans as a diversification vehicle especially if you hold a lot of employer stock.

If deferred compensation plans sound too good to be true it’s because there are some key risks associated with executive deferred compensation plans, which we’ll explore below.

What are the downsides of deferred executive compensation plans?

The risk of forfeiture is the biggest downside of using a non-qualified deferred compensation plan. When you invest in a DC Plan, the money is not yours; rather, you are an unsecured creditor.

This means that there is a very real chance that if your company goes bankrupt, you will never see this money. This can significantly impact your decision about how much you contribute and when you get paid.

In worst-case scenarios, even without bankruptcy, a hostile takeover or merger can impact new management’s willingness to pay out the deferred compensation. This can lead to deliberate foot-dragging and administrative barriers that can only be solved by lawsuits that force you to settle for less than 100 cents on the dollar.

Unlike a 401k, an NQDC is very restrictive regarding changes to almost anything within the plan. This includes when and how you receive the funds. Accelerating the distribution can be very difficult as it often requires a year’s worth of notice and a minimum of five years before you receive the payments.

How to Implement and Participate in a DCP:

Here are important facts to understand before you establish and participate in an executive deferred compensation plan:

Most DCPs are established as a Rabbi Trust. Rabbi trusts set aside your money in non-revocable trusts, often overseas, to avoid tampering. This makes the risk of forfeiture not as big of a deal. However, it’s important to understand that risk.

In order to meet the qualifications of forfeitable income and for you to get the tax benefits of an executive deferred compensation plan, the Rabbi Trust is subject to your company’s general creditor claims. But the money actually exists rather than just a promise.

Before you start allocating large chunks of your salary and bonus to your non-qualified deferred compensation plan, you should max out your contributions to your 401(k), HSA, and mega-backdoor Roth accounts. All of these retirement savings vehicles will offer better flexibility, investment options, and a guarantee that the funds contributed to these plans are yours.

If your DCP allows for a match factor, consider, at a bare minimum, taking advantage of the match.

You will usually have a very limited window of time to sign up for your NQDC, the enrollment period lasts 30 days annually. It’s typical for the deferred compensation plan to require you to make a decision in the current year about your salary next year and how much you will want to contribute to the plan. You should have a good understanding of your cash flow needs and options for cash.

Your NQDC will ask you to set up either an evergreen plan, which refreshes every year with the same contribution, investment, and distribution decisions, or a decision that you must renew annually.

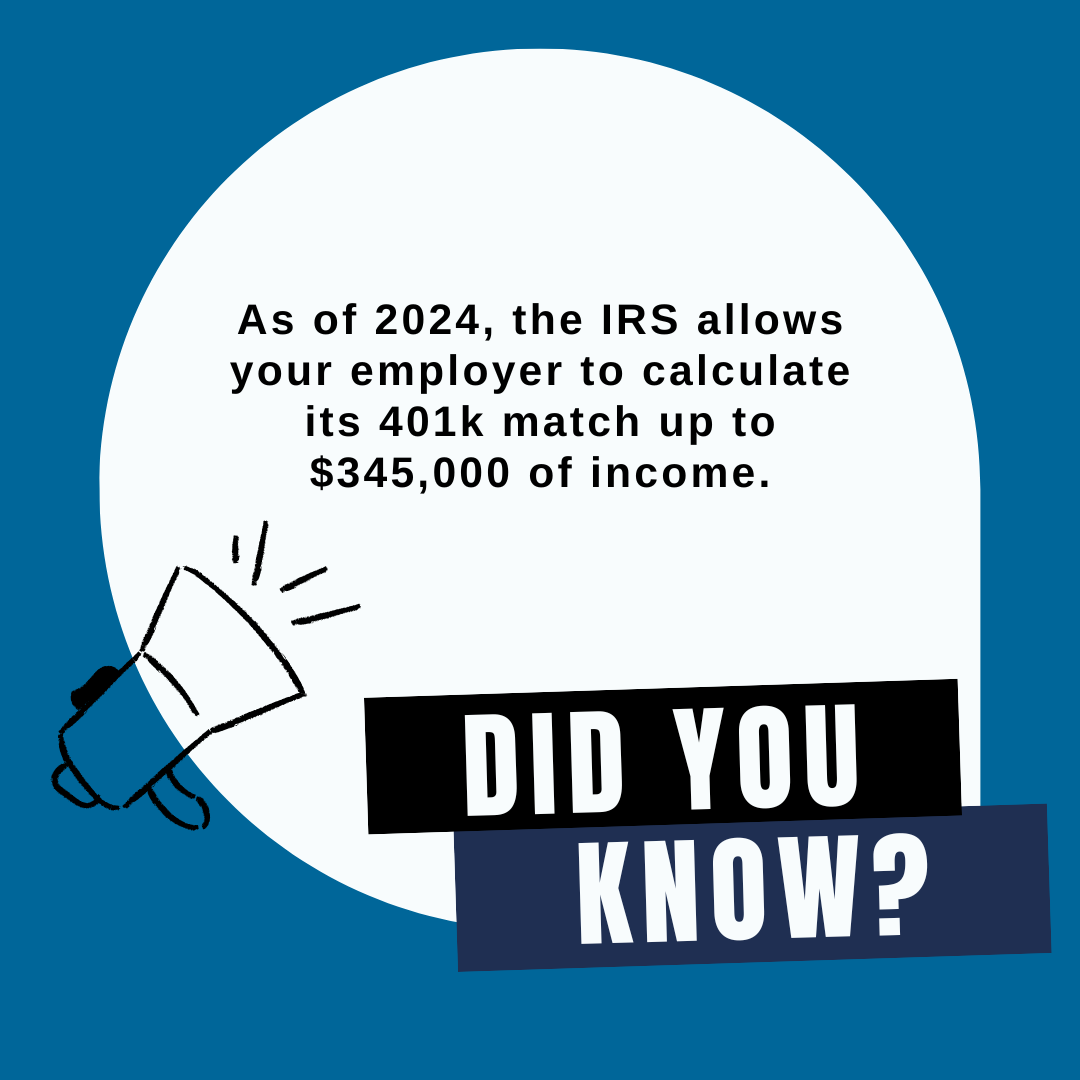

Finally, it’s important to understand that contributions to your executive deferred compensation plan can impact your 401k match.

As of 2024, the IRS allows your employer to calculate its 401k match up to $345,000 of income. This means that if you make more than $345,000 and you choose to use the non-qualified deferred compensation plan to defer your income so it is below the $345,000 total, you may not get the full benefit of your employer’s match.

If you aren’t overwhelmed and excited yet, have no fear, as we’re about to share four ways you can maximize your executive non-qualified deferred compensation plan.

If you need help navigating this complicated yet very useful employer benefit, reach out to us using this link: HERE. We have over fifteen years of experience helping tech professionals maximize their non-qualified deferred compensation plans.

Tax Benefits of a Non-Qualified Deferred Compensation Plan:

Undoubtedly, the biggest benefit to an NQDC is the tax savings. The ability to defer your tax bill and to shelter the growth from capital gains and ordinary income makes this the primary reason to utilize a DCP. However, there is some nuance to it.

Specifically, choosing the right distribution date can help you benefit from tax arbitrage and get the most out of the portfolio appreciation in a tax-free environment.

Tax Arbitrage

If you have access to a non-qualified deferred compensation plan, it’s safe to assume that you are in your highest earning years. The decision to defer the compensation to a later time should be based on when you think you will have low-income years. This doesn’t mean the furthest possible date. You could be anticipating a sabbatical, family leave, looking for new work, starting a business, and many other short windows where you would benefit from income and the lower tax bracket.

Second, there is a sweet spot window in retirement when your income will be historically low. This is typically right after retirement before you start taking social security at age 70, assuming you opt to delay taking your benefits, and before you are required to take distributions out of your retirement accounts, which is currently at age 75. So, if you retire at 65, you will have five years of low-income and ten modest income years.

Finally, if you plan to move to a zero-income-tax state, you can be taxed in the new state’s tax regime if your payments are made over ten years or more. Any payout structure with a shorter window will result in tax payments based on the state of origination.

Tax-Free Growth

The second benefit is that any growth you experience in the portfolio will be tax-free. The longer the time horizon before your distributions are made and the longer the distribution period, the greater the tax benefit.

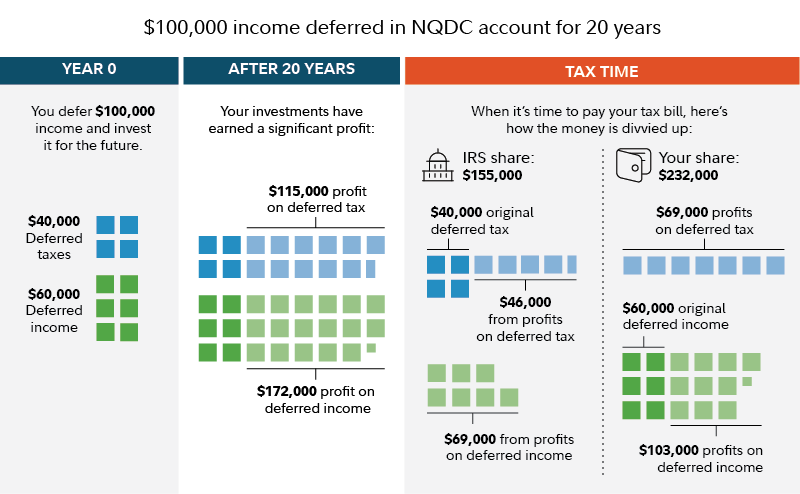

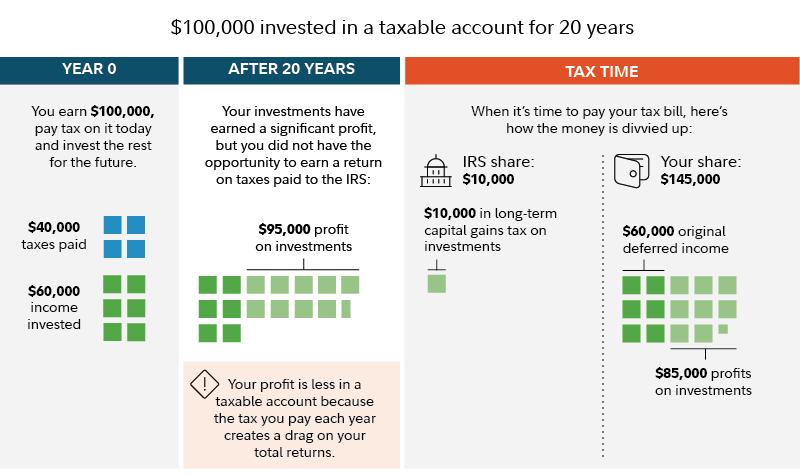

Below is an example of using an NQDC for 20 years vs investing in a taxable account.

Even if you think that tax brackets will go up in the future, a likely scenario given the federal deficit, the benefits can be significant. In the above example, the difference between your share under an NQDC and a taxable account is $87,000. To wipe out this difference, the tax rates would need to increase by 30%. Some plans will allow you to kick the distribution further down the road. This means that if you are in a high tax regime, you can wait it out and see if it changes.

Using a DCP to plan around income recognition:

All deferred retirement plans require you to set up distributions in advance, usually for the following year. This allows you to plan around tax events, whether voluntary or not.

Here are a few examples of when it would make sense to implement a deferred compensation plan:

- You anticipate a large bonus next year

- You would like to exercise a large chunk of non-qualified stock options and, in some cases, incentive stock options

- You would like to sell some appreciated shares of stock

- You are selling a property, residential or investment

As a tech executive, you may have a high concentration in your employer’s stock, or your stock options are getting close to expiration. By utilizing a deferred compensation plan, you can drastically reduce your tax bracket and the tax brackets at which sales of stock and exercising of options would occur.

However, remember that you are swapping equity risk for risk of debt. This is lower on the notch of risk. Equity risk and debt risk can coincide, however, it is very likely that if your company is having a hard time paying its debtors, its stock won’t be doing well either. This allows you to reduce your exposure and risk all while controlling the tax impact.

DCP as a tool for reaching goals and planning your career:

The ability to control your distributions also allows for creative planning. Most deferred income plans ask you to set up a new contribution and distribution structure yearly. Matching the amount contributed and when it is distributed can be planned around key life events.

This could include things like taking sabbaticals, paying for college education, big purchases such as vacation homes, or starting a separate business.

Planning the distributions around your career stage is also critical. If this is your last job and your last employer, you may set the distribution to start at your termination. This provides you the greatest flexibility to work as you see fit and retire when you wish without worrying about massive amounts of income in one year.

However, if this is far from your last job, you may set the distribution to occur at a specific age. As mentioned before, some plans will allow you to extend as long as you notify the plan far enough in advance. This strategy allows you some flexibility to keep working into your later years.

Finally, there is no maximum age at which you need to take your distributions. This can allow you to plan for your sunset years as your IRAs dwindle and you may consider large medical expenses such as retirement homes.

Diversify through a NQDC:

The final way to maximize your executive non-qualified deferred compensation plan is to use diversification strategies. This is especially applicable if you have accumulated a large amount of your wealth in employer stock.

Despite all the restrictions on DCPs, you do have the flexibility to adjust your investment mix. If the investment selection is robust enough, it can provide the ability to create a complementary portfolio.

For example, if most of your wealth is tied up in a tech stock, you may choose to invest your NQDC in foreign markets, value investments, or more conservative assets like bonds.

Because selling and rebalancing do not have tax ramifications, you can reevaluate your household asset allocation and adjust it based on your ever-changing wealth. Of course, this asset allocation mix will also depend on the timeline of your overall goals and the timeline of when the distributions will start and how long they will continue..

Summary:

Executive deferred compensation plans are a great way to save additional money for retirement and other financial goals when 401k savings rates just won’t support your executive lifestyle. But they are so much more than that.

They provide tax savings and flexibility to navigate key financial events in your life.

Keeping track of various deferred compensation distribution dates can become challenging. This is where we highly recommend using financial planning software to map out your cash flows intelligently.

As a tech professional, you know your financial journey is more like debugging complex code than following a straight line. You’ve put in the hard work to reach your current success. At RHS, we get the unique challenges and opportunities of your profession. Think of us as your financial developers, crafting solutions tailored to your needs.

Choosing a financial advisor is a big decision, and we know you have options. That’s why our focus isn’t just on growing and protecting your assets. We go beyond understanding your financial goals by creating and refining tools and strategies designed specifically for you. It’s like having a custom app to optimize your financial health.

When thinking about who will help you grow and preserve your wealth, it should be based on their expertise and trustworthiness.

You’ve dedicated years to reaching your goals. Don’t settle for a generic investment strategy with mediocre results. Let’s create a plan that’s as unique as your journey.

If you need help with your executive non-qualified deferred compensation plans, contact us using THIS link.

2024 Disclosures

RHS Financial is an SEC registered Investment Advisory Firm and distributes this presentation for informational purposes only. This presentation ( hitherto referred to as the presentation throughout this disclosure), blog post, infographic, slide deck or whatever form of informational modality the reader wishes to describe this as is provided for informational purposes only and should not be construed as investment advice in any way.

We believe the information, including that obtained from outside sources, to be correct, but we cannot and do not guarantee its accuracy in any way. RHS Financial uses information from outside sources to develop graphs, charts, infographics, etc. to enhance this presentation and while we believe the information from these outside sources, to be correct, we cannot and do not guarantee its accuracy in any way,

Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors who may be employees of but do not necessarily reflect the views of RHS Financial as a company. There can be no guarantee that developments will play out as forecasted. The information in this presentation is subject to change at any time without notice. This presentation contains “forward-looking statements" concerning activities, events or developments that RHS Financial expects or believes may occur in the future. These statements reflect assumptions and analyses made by RHS’s analysts and advisors based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond RHS Financials’ control, they are no guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements. In a nutshell; these are our best guesses and please don’t assume they are fact.

Mentions of specific securities, investment products, investment indices, companies or industries should not be considered a recommendation or solicitation. Data and analysis does not represent the actual or expected future performance of any investment or investment product Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This post may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with RHS Financial and does not sponsor, endorse or participate in the provision of any RHS’ services, or other financial products. Index information contained herein is derived from third parties and is proffered to you unaltered as we derived it from the third party.

RHS Financial, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where RHS Financial, LLC and its representatives are properly licensed or exempt from licensure. This presentation is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place.

If the client is deemed suitable and agrees, RHS may employ leveraged strategies for these clients. Leverage attained through margin on a client’s account can add additional risk. While RHS tends to seek to improve return with theses strategies by applying leverage to less risky indexes, there is no guarantee that that RHS will lower risk or improve returns.

RHS Financial. 4171 24th St. Suite 101 San Francisco, CA 94114