Social Security is Broke(n) and Cannot Be Fixed

In my last post, I wrote about how as of this year, the US Social Security system is bleeding cash and policymakers will soon be forced to make tough decisions about the future of the program. The long-term financial woes of Social Security are of course well known, and last month’s news of the deficit had been anticipated for decades. But prognostications about Social Security’s health are nearly always proceeded by prescriptions on how to fix it, whether coming from the left, right, center, or elsewhere. I, on the other hand, want to take a break from my normally optimistic outlook and make the case for Social Security pessimism: this widely beloved national institution is, in fact, a bad deal for the majority of Americans alive today, this is a problem that’s fundamental to the basic economic logic of Social Security and is not the result of inefficient administration or any specific policy, and there is no possible way we can fix the basic problem. So pour yourself a glass of something stiff and get ready to see how our society has and will continue to keep shooting itself in the foot for generations to come.

How to Lose Money Forever

Since the beginning, Social Security has been talked about as though it were some large pension or national savings account, and the user experience is purposefully set up to mimic that design: the benefits retirees receive are proportional to the taxes they pay in. In just the latest Trustees Report the administration uses this sort of language in describing the program:

The Social Security program provides workers and their families with retirement, disability, and survivors insurance benefits. Workers earn these benefits by paying into the system during their working years. Over the program’s 83-year history, it has collected roughly $20.9 trillion and paid out $18.0 trillion, leaving asset reserves of $2.9 trillion at the end of 2017 in its two trust funds.

Reading this, you might get the impression that Social Security operates more or less like any other private financial institution you might use to provide for yourself in retirement. Just like with a bank or an annuity provider or something, you pay money into the system over your working life, those funds are thrown into a big pile of money along with everyone else’s and invested in assets of some sort that earn a return over the years, and when you retire the income and principal from those investments can be used to cover your retirement expenses.

The essential feature of Social Security, however, is that absolutely nothing like this happens whatsoever. Social Security is set up primarily as what is known as a pay-as-you-go system (often abbreviated PAYGO in the literature). In a PAYGO system the funds that are collected in any given period are used to pay the beneficiaries and there is no accumulation of any assets, and so no actual investments are made. As I mentioned last time, the Social Security “trust funds” are mere accounting fictions that do not contain any economically meaningful assets. Though the specific rules Social Security follows for paying benefits are somewhat complicated and subject to change, so that in any given year outflows do not exactly match inflows, to a close approximation Social Security can be modeled as a pure PAYGO system.

A PAYGO system thus relies on a steady inflow of new workers to pay into the system. Without them the entire system collapses and the current cohort of beneficiaries loses their entire “investment.” This, of course, is also the basic structure of a Ponzi scheme, and Social Security has long been criticized as just being a government-sponsored Ponzi scheme. This may be technically correct, but arguably then all of civilization itself is a Ponzi scheme, so I wouldn’t lean too heavily on the comparison. The key difference, in any case, is that a private (criminal) Ponzi Scheme eventually must collapse, unless the fraudster(s) can magically manage to “fool all the people all the time,” because as soon as enough of the participants wise up and go to cash out, the entire system unravels. A government-mandated PAYGO system, on the other hand, can in principle exist in perpetuity, because the state can and does forbid its citizens from opting out.

What are the economics of a perpetual pay-as-you-go system? Yale economist John Geanakoplos is one of the leading authorities on the topic. In a 2000 paper, Social Security Money’s Worth, written for the National Bureau of Economic Research, he and his coauthors extensively detail the theoretical underpinnings to Social Security and various policy alternatives that have been proposed for it. They start by building a toy model of the US economy with a stable real interest rate r (which they assume to be 2.3%), and population and productivity growth rate g (assumed to be 1.2%). Then they imagine creating a pure PAYGO Social Security system in 1938. The question is, what rate of return do various cohorts of workers “earn” on their contributions, and how does that compare to the market rate of interest, r? Earning higher-than-r returns from Social Security makes you better off, if you earn less-than-r then Social Security is a bad deal for you.

The central upshot is that in a pay-as-you-go system, just as with a Ponzi scheme, the people who earn the greatest return are those who get in at the beginning. The cohort of workers that retired shortly after the system was set up in 1938 received a windfall as they paid little or no money into the system but received benefits for the rest of their lives. Subsequent cohorts spend a longer and longer time paying into the system in order to receive the same retirement benefits and thus earn lower and lower returns. Returns continue to fall for each new cohort until we reach the first one that entered the labor force with Social Security already in place, i.e. those who began their careers after 1938. For them and every generation thereafter, the return earned on Social Security contributions is equal to g, the growth rate of the wage base from which the system draws upon. The authors plot these rate-of-return calculations for each cohort in their hypothetical economy like so:

A PAYGO system then mostly benefits the first generation of retirees, who earn fantastically high returns on their “investment”, at the expense of all future generations, who earn only g on their money, which is lower than the market rate of interest. Note that this conclusion rests on the assumption that r > g; this is a core theorem in economics that pops up all over the place and if it weren’t true nothing in finance or economics would make sense. It’s like our field’s version of dividing by zero. Geanakoplos, et al. explicitly highlight the importance of the inequality in their analysis:

The fact that r is greater than g is very important to the qualitative features of a pay-as-you-go social security system such as the one sketched here, although the exact magnitudes of the numbers are not. If instead r were less than g forever, then any expansion of a pay-as-you-go social security system would make everybody better off, at least up until the point that the market interest rate r rose back to g. Indeed, if r < g, it is not even possible to assign a finite number to total social security benefits. Most economists, we believe, would subscribe to the idea that the real market rate of interest is greater than the rate of growth of the economy.

The supposition that r>g allows us to discount the future to a finite number. But it also makes the past loom large. As we shall see, one extremely important reason that our social security system imposes such a burden on today’s young is that the system transferred a great deal of wealth to the generations retiring just after the Great Depression. Since r>g, the present value in 1997 of a transfer in 1940 is a larger fraction of 1997 GDP than the actual transfer was of its contemporaneous GDP.

In other words, if r were less than g then the government could make everybody infinitely wealthy by expanding Social Security by an infinite amount, but since r is in fact greater than g then it necessarily has the effect of making early cohorts better off at the expense of all future cohorts.

Now, reality of course is a little more complicated than that. Both r and g bounce around a lot over time, and the rules of Social Security have changed as well. In particular, expansions to the Social Security system in its early days had the effect of improving returns for a larger number of the earlier cohorts, but ultimately this just comes at even greater cost to future generations. Using real historical data, Geanakoplos, et al. perform present value calculations and find that about the first 50 birth-year cohorts benefited from Social Security, receiving about $9.7 trillion in 1997 dollars worth of transfers, to be paid by everybody born after 1937. And so, while there are still some octogenarians (or greater) out there who are getting their money’s worth out of Social Security, those of us who are in our 70s or younger got the short end of the stick. We are stuck paying for a 10 trillion dollar gift made to our grandparents on credit and will get a far worse deal on Social Security than they did as a result.

What’s more, there is absolutely no way out of this predicament. Asking how we can fix Social Security now in 2018 is like investors who’ve lost everything in a Ponzi scheme asking how they can get their money back when the original investors have already spent their earnings on $10 trillion worth of Champagne. The answer is, you aren’t getting your money back. Your money is gone, spent by entire generations of retirees who are now mostly all dead. The best we can hope for now is to accept the measly, sub-market returns that will be paid to us by our grandchildren, who will themselves be getting the same raw deal, on and on down the line for eternity. The only way out would be for one generation to stand up and eat a $10 trillion loss. We could of course just stop all Social Security taxes and benefits right now, and save today’s children from this bad deal, but that would mean forcing all of today’s retirees and older workers to face massively-negative returns on all the contributions they made up to now. Or we could say, for instance, that no benefits will be paid to anybody born after this year but we’ll keep the taxes around long enough to pay off everybody who’s paid in so far. That of course would just shift the burden to the next generation, who would earn a -100% return on a lifetime’s worth of taxes they pay but for which they receive no benefit. Any gradual phase-out of the program would require multiple generations of people to earn less-than-g returns on their Social Security dollars.

What Falling into a Black Hole Looks Like

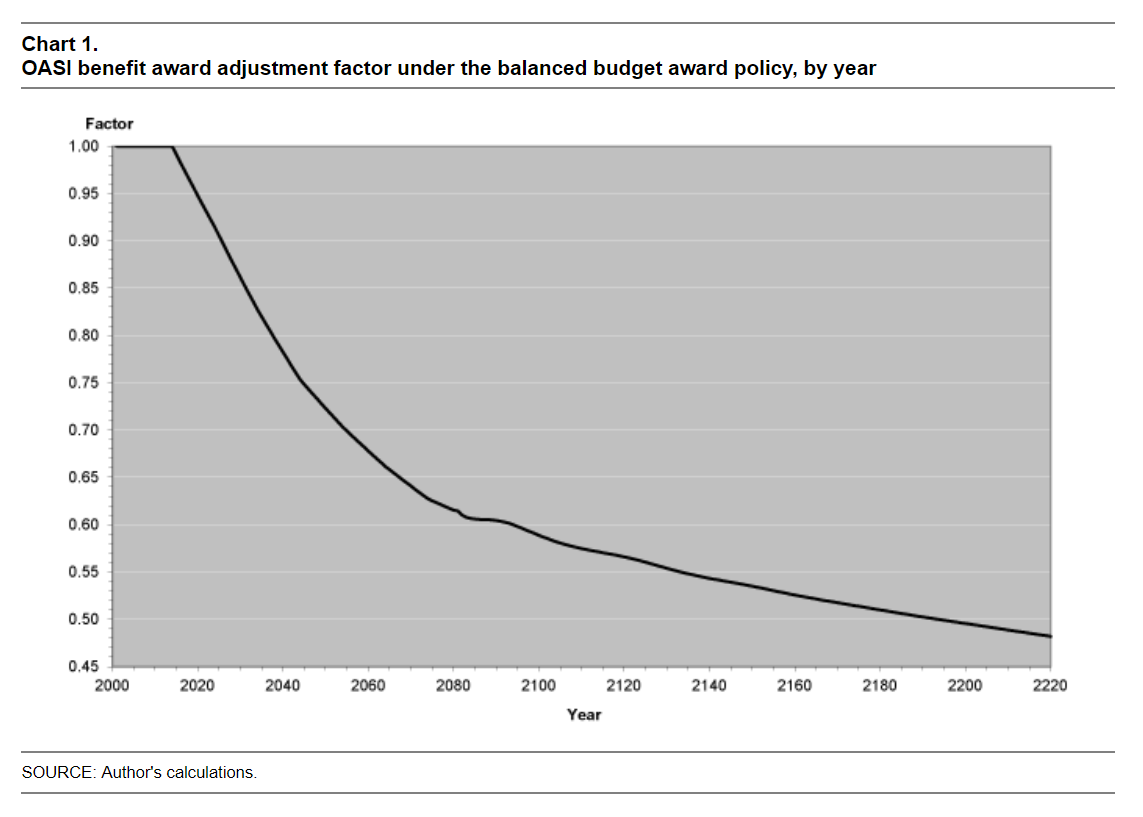

This is all very theoretical, but once we bring it back to the present day real world everything gets much worse. A pure PAYGO system doesn’t ever run at a deficit; it just pays out everything it brings in each year with nothing left over and nothing owed. The current Social Security system now faces an ongoing deficit because fundamentally, current law is written to promise higher-than-g returns to retirees, something that is ultimately unsustainable. How much would law have to change to restore long-run financial viability to the system? One of the most comprehensive treatments on this topic is this 2007 report by Dean Leimer working for the Social Security Administration Office of Policy. Using data current at the time (don’t worry, the numbers have only gotten worse since then), he plots the path benefits would have to decline by as a proportion of present law if we began cutting them in 2015. Here’s what that looks like:

This is, as Leimer notes, “rather dramatic.” Even if we get started three years ago, Social Security benefits would have be cut by 25% by the early 2040s to remain on a sustainable path, and would continue to fall for generations to come. Such draconian action is probably politically unacceptable, and polls show more Americans favor raising taxes instead of cutting benefits in order to support Social Security, so at least in the short-to-intermediate-term that’s probably what we’ll get. What will that look like? Leimer has a chart for that too.

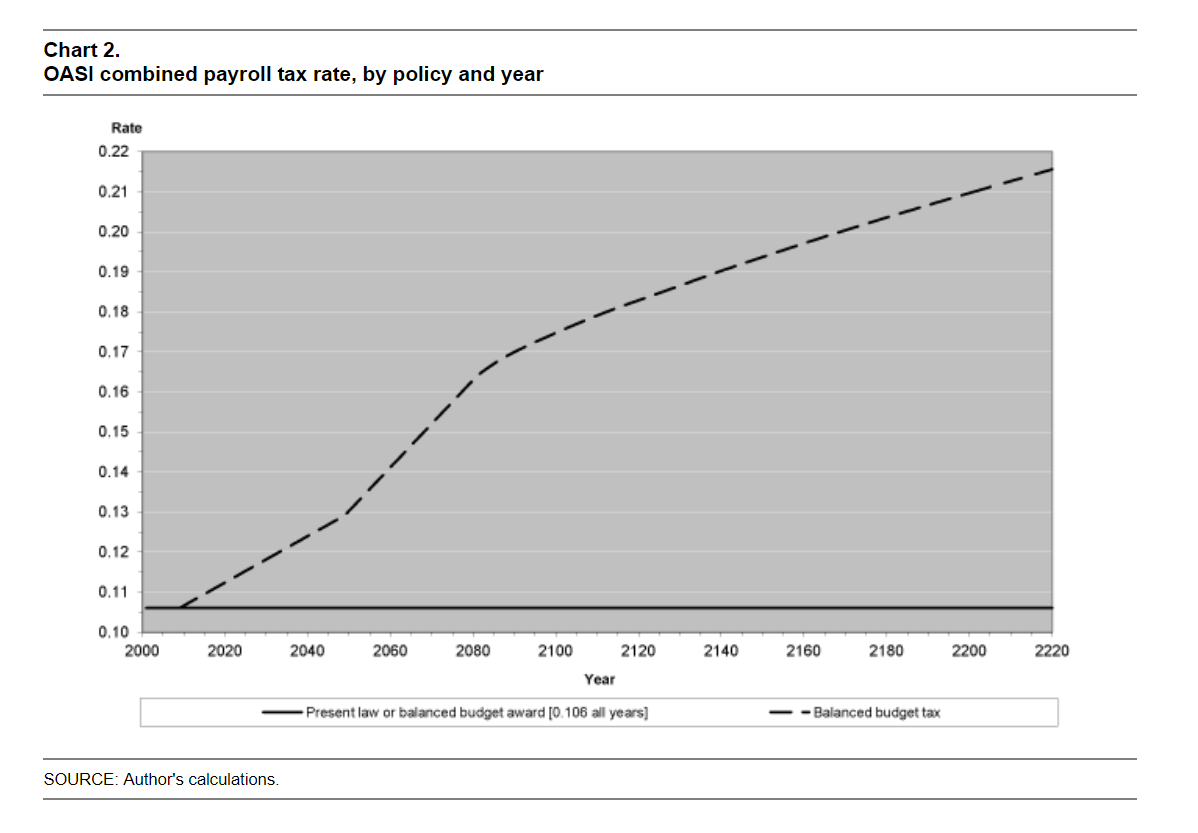

This is, as Leimer notes, “rather dramatic.” Even if we get started three years ago, Social Security benefits would have be cut by 25% by the early 2040s to remain on a sustainable path, and would continue to fall for generations to come. Such draconian action is probably politically unacceptable, and polls show more Americans favor raising taxes instead of cutting benefits in order to support Social Security, so at least in the short-to-intermediate-term that’s probably what we’ll get. What will that look like? Leimer has a chart for that too.

Taxes would have to steadily rise from here on in in order to support current benefit levels. Unlike with benefit cuts, though, there would be no end to the tax increases. Because benefits are now growing at greater-than-g, if left unchecked they would eventually take over the entire economy and in the logical extreme taxes would have to converge on 100% in order to support the system. Obviously this is impossible, and Leimer says that the just-raise-taxes strategy is “equivalent to a continuing succession of small program expansions. As a consequence, such a policy is not sustainable over the very long-run.” Granted, the “very long-run” here is multiple centuries, a period over which we’ll likely see much more radical changes to the nature of our economy and society. In the shorter run, like 2040, taxes would only have to be raised a few percentage points. That’s not so bad, right? Unfortunately, as I already mentioned, the numbers today are probably quite a bit worse than Leimer presented in 2007. How much worse?

Taxes would have to steadily rise from here on in in order to support current benefit levels. Unlike with benefit cuts, though, there would be no end to the tax increases. Because benefits are now growing at greater-than-g, if left unchecked they would eventually take over the entire economy and in the logical extreme taxes would have to converge on 100% in order to support the system. Obviously this is impossible, and Leimer says that the just-raise-taxes strategy is “equivalent to a continuing succession of small program expansions. As a consequence, such a policy is not sustainable over the very long-run.” Granted, the “very long-run” here is multiple centuries, a period over which we’ll likely see much more radical changes to the nature of our economy and society. In the shorter run, like 2040, taxes would only have to be raised a few percentage points. That’s not so bad, right? Unfortunately, as I already mentioned, the numbers today are probably quite a bit worse than Leimer presented in 2007. How much worse?

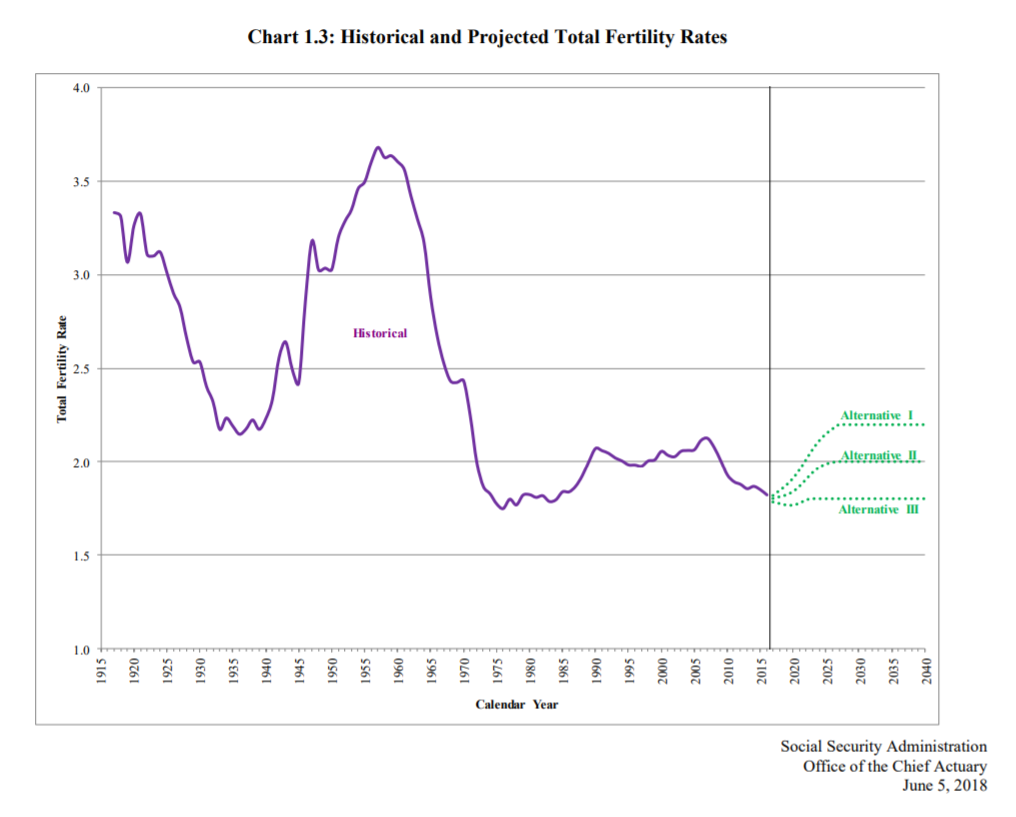

The SSA does a lot of work to model what they think r and g will be in the future. g is a combination of productivity growth and demographics (population growth), the latter of which relies principally on the fertility rate. Fertility rates around the world have of course been falling for a while now, in some cases for hundreds of years. As of the latest (2018) report, the SSA now assumes for its baseline projections that US fertility will stabilize at 2, which maintains a constant population. In their more pessimistic “high cost” scenario (Alternative III) they assume it will stabilize at 1.8, which would eventually result in a slowly declining population.

What is the actual US fertility rate right now? It just fell to a new low of 1.76, lower than the SSA’s worst-case scenario. And there’s not much hope it’ll bounce back anytime soon. The US actually has a higher fertility rate than most other developed nations. Many countries, such as Japan, have had below-replacement-level fertility for many years now and are experiencing shrinking populations. But despite pro-natalist measures adopted by many different governments around the world, societies seem mostly incapable of bringing their fertility rates back above replacement levels once they fall below. Perhaps after a few generations of declining population cultural norms around child-rearing will reverse and we’ll see a new baby-boom, but for the next several decades at least the developed world will almost certainly see their fertility rates continue to fall even lower, causing accelerating population declines. The US population will probably peak in the next decade or so and begin falling after that, bringing g down with it.

(Of course, population growth can also be achieved through immigration. Suffice it to say that doesn’t seem likely to increase under the current administration. We’ll see how future policymakers address this issue in the face of growing deficits and a shrinking tax base.)

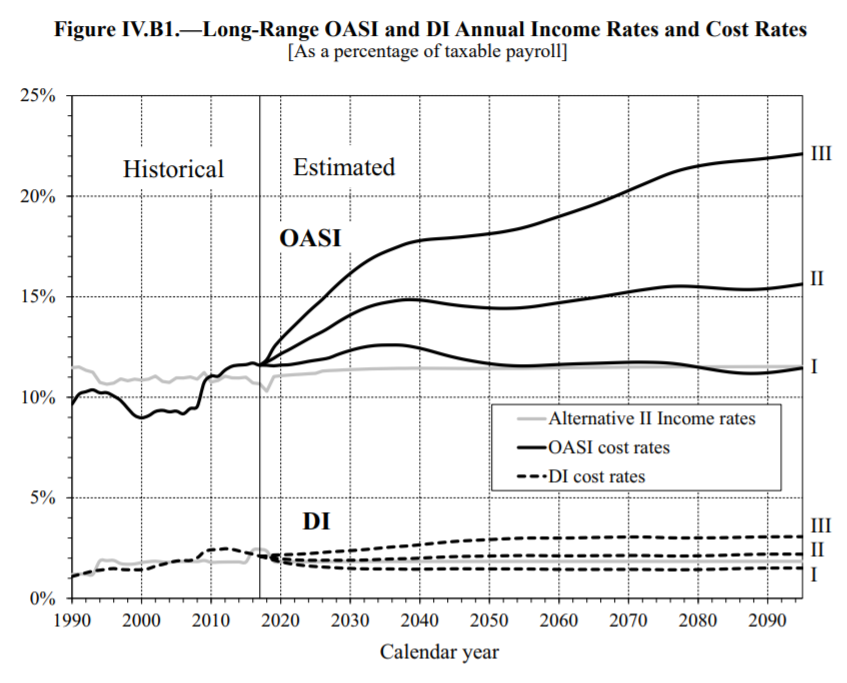

There’s also reason to suspect that the SSA’s projections for productivity growth are too high as well (1.68% in the baseline case, 1.38% in the high cost case), though this is more controversial and the topic of a larger discussion which I’ll be exploring in future posts. For now let’s take their high cost 1.38% figure as a given. Where does that put us in terms of plan sustainability? Here are the 2018 cost estimates the SSA projects for high-cost (III), low-cost (I), and baseline (II) scenarios into the future:

Using the somewhat more realistic fertility and productivity estimates the SSA considers pessimistic, the cost of Social Security as a percent of payrolls stands to nearly double by 2040, implying of course that we would need to roughly double FICA payroll taxes by then in order to keep treading water.

What about r? The SSA likes to use the interest rate it earns on its trust fund “assets” as its estimate of r, that is, the rate on treasury bonds. This makes the opportunity cost of the program seem not so bad. Treasury bond yields are low, historically barely higher than g. In fact, if we look up the yield on long-term inflation-protected treasury bonds right now, they’re only at 0.82%, even lower than our pessimistically-low projection of g. This would seem to violate our r > g assumption and imply that the government can make us better off by actually expanding Social Security, at least until rates rise. Is the situation maybe not as bad as I’ve been laying out?

Hahaha no of course the news isn’t as good as that. First of all, from the perspective of a Social Security participant, being “invested” in the program is actually much riskier than investing in treasury bonds. Your future benefits in fact depend on the path of average earnings in the economy, and this is a variable that is subject to the same sort of macroeconomic risks as the stock market. John Geanokoplos actually has another paper on this topic and concludes that the SSA should be using a much higher rate to discount its liabilities than the “risk-free” rate it currently prefers.

Secondly, the proper value of r to use if we’re evaluating the cost of Social Security to its participants is the r such participants would earn if investing for themselves. This will obviously vary widely depending on the individual, so we need an average value corresponding to a “representative agent.” Basic finance theory tells us that this should be the r that corresponds to the “market portfolio” of all the investable financial assets there are, ideally in the whole world, weighted in proportion to their market values. A recent paper, Historical Returns of the Market Portfolio, estimates that such a portfolio had an average annualized real return of 4.36% since 1960. Based on my own forward-looking return estimates, this figure is not far from what investors may reasonably expect going forward as well (it’ll likely be a little lower, but not as much lower as g will be). This three percentage point or so gap between r and g corresponds to hundreds of billions of dollars of missed opportunity for the American public every year.

Privatization to the Rescue?

Given this gulf between the returns people can get from Social Security and what they can get in private financial markets, many people support some form of Social Security privatization. Instead of contributing money to Social Security’s PAYGO structure, we could set up a forced savings plan where an individual’s contributions were actually invested into the financial markets, either through a private and individually managed account, similar to a 401(k) plan, or managed collectively through a sovereign wealth fund (or some combination of the two). Social Security privatization has generally been a policy proposal associated with the Republicans in the US (it was a major part of George W Bush’s platform, but he never got it off the ground), but around the world various forms of private, forced-savings plans are commonplace and not necessarily seen as a left-right issue, with countries as varied as Australia, Sweden, Chile, Singapore, Mexico, and the UK each having some version of privatized retirement accounts (some with a sovereign wealth fund on top of that).

Some privatization advocates in the US see this as a free lunch that can solve all the problems of Social Security with ease. They are wrong. The fundamental problem is that because the Social Security system doesn’t have any assets, there isn’t actually anything to privatize. Investing in the financial markets is great and all, but you need some actual money to invest in the first place. But we don’t, so we can’t. We could, of course, adopt a policy that from now on all FICA payroll taxes would be directed into privatized accounts, but this would leave no money to pay the benefits of today’s retirees and older workers who spent their entire lives paying into the old system. Once again, we get can’t get there from here without one or more generations eating a multi-trillion dollar loss.

Here’s one clever thing the government could do that would at first seem to solve the problem: calculate an actuarially fair estimate of the present value of benefits owed to each individual currently in the Social Security system based on what they’ve paid so far, from current retirees to youngsters who just started working last year (there are various estimates of what this number would be, suffice it to say it would be at least $10 trillion); issue the face value of this estimated benefit to each individual right now in the form of newly-issued treasury bonds deposited into newly-established private Social Security accounts; individuals could then hold the treasury bonds if they want and earn interest on them, or sell them into the open market to reinvest in other assets like stocks and corporate bonds; going forward, all payroll taxes are directed into each individual’s private account and invested as they see fit (perhaps subject to certain government restrictions or based on some default option setting). This would achieve the goal of pre-funding Social Security and solve the problem of unfunded liabilities. Unfortunately, it would not solve the problem of Social Security still being a bad deal for everyone alive today. Instead, Geanokoplos shows that for an economy in equilibrium, the amount of taxes the government would have to raise to pay for all this newly issued debt would exactly offset the increase in returns participants saw from privatization, bringing us all back to square one. I won’t walk through the entire argument, and it applies only in broad aggregate; individual outcomes would vary a great deal. But the essential point remains that Social Security was, first and foremost, a massive inter-generational wealth transfer to the constituency of Franklin Delano Roosevelt, that money is gone now, and there is absolutely nothing we can do to get it back.

Now, it may still be worth transitioning to a system where Social Security funds are invested into financial assets, because this would increase our economy-wide level of investment, which would likely increase our economic growth rate. So while we can’t earn r on our Social Security dollars, we can hopefully increase the g that we do get. Geanokoplos once again has a complicated argument for why this could only have very small effects, but I think he’s a bit too pessimistic on this front, for reasons I won’t get into here. Transitioning to a privatized system would not fix Social Security in the sense of making it a good deal for most Americans, but we could at least make it slightly less bad. Of course, achieving this modest improvement would require heroic levels of foresight and cooperation among and between Congress and the Presidency. So, um, don’t hold your breath.

What can we do as individuals about this? Plan ahead. If you plan on working for more than a few more years, you can pretty safely bet on your payroll taxes going up pretty soon, probably the next time the Democrats are in control. If you’re young, it’s probably safe to guess you won’t be getting as much in benefits either, especially if you’re a high-income earner. For someone such as myself who was born in 1985 and is in the top 20% of earners, I’d assume a haircut of 50% or so to be conservative. Above all, save more! You’ll need it. But of course, you already knew that. Did you really need to read 4,000 words of such depressing exposition to get to such a predictable climax?

Disclosures: This post is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place. Please contact us at your earliest convenience with any questions regarding the content of this post. For actual results that are compared to an index, all material facts relevant to the comparison are disclosed herein and reflect the deduction of advisory fees, brokerage and other commissions and any other expenses paid by RHS Financial, LLC’s clients. An index is a hypothetical portfolio of securities representing a particular market or a segment of it used as indicator of the change in the securities market. Indexes are unmanaged, do not incur fees and expenses and cannot be invested in directly.

2024 Disclosures

RHS Financial is an SEC registered Investment Advisory Firm and distributes this presentation for informational purposes only. This presentation ( hitherto referred to as the presentation throughout this disclosure), blog post, infographic, slide deck or whatever form of informational modality the reader wishes to describe this as is provided for informational purposes only and should not be construed as investment advice in any way.

We believe the information, including that obtained from outside sources, to be correct, but we cannot and do not guarantee its accuracy in any way. RHS Financial uses information from outside sources to develop graphs, charts, infographics, etc. to enhance this presentation and while we believe the information from these outside sources, to be correct, we cannot and do not guarantee its accuracy in any way,

Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors who may be employees of but do not necessarily reflect the views of RHS Financial as a company. There can be no guarantee that developments will play out as forecasted. The information in this presentation is subject to change at any time without notice. This presentation contains “forward-looking statements" concerning activities, events or developments that RHS Financial expects or believes may occur in the future. These statements reflect assumptions and analyses made by RHS’s analysts and advisors based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond RHS Financials’ control, they are no guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements. In a nutshell; these are our best guesses and please don’t assume they are fact.

Mentions of specific securities, investment products, investment indices, companies or industries should not be considered a recommendation or solicitation. Data and analysis does not represent the actual or expected future performance of any investment or investment product Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This post may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with RHS Financial and does not sponsor, endorse or participate in the provision of any RHS’ services, or other financial products. Index information contained herein is derived from third parties and is proffered to you unaltered as we derived it from the third party.

RHS Financial, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where RHS Financial, LLC and its representatives are properly licensed or exempt from licensure. This presentation is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place.

If the client is deemed suitable and agrees, RHS may employ leveraged strategies for these clients. Leverage attained through margin on a client’s account can add additional risk. While RHS tends to seek to improve return with theses strategies by applying leverage to less risky indexes, there is no guarantee that that RHS will lower risk or improve returns.

RHS Financial. 4171 24th St. Suite 101 San Francisco, CA 94114