Testosterone is not an Investment Performance Enhancer

Finance, especially investment management, has traditionally been a male-dominated industry, often noted for its swashbuckling machismo, aggressive competitiveness, and otherwise male-high-school-jock-stereotype nature as in popular movies like Wall Street and The Wolf of Wall Street. In Michael Lewis’s debut book Liar’s Poker, about the time he spent working at a major investment bank, the top traders are referred to as “big swinging dicks” as a superlative. Liar’s Poker remains one of the most widely read books among employees of the financial industry and has influenced many young men to join the profession, contrary to the author’s intentions.

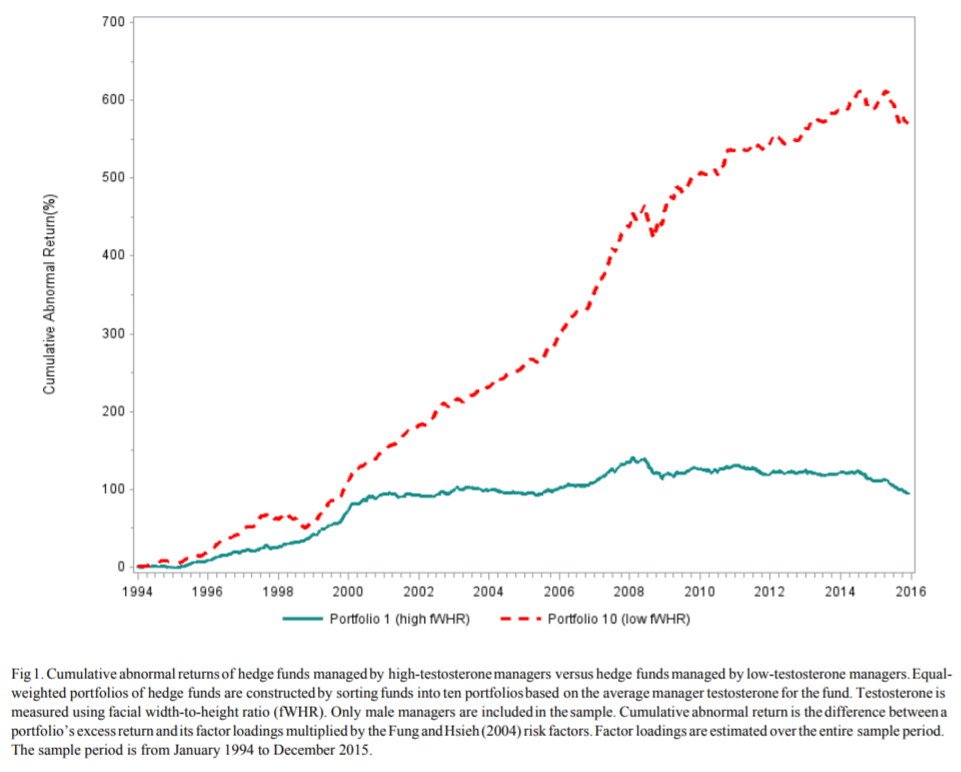

Which is why, as someone who always enjoys a nice dose of irony, I was pleased to read a (wonderfully titled) new paper Do Alpha Males Deliver Alpha? Testosterone and Hedge Funds by researchers Yan Lu and Melvyn Teo. Lu and Teo examine the performance of 3,228 male hedge fund managers over a 22 year period and compare their returns to their facial width-to-height ratio using image recognition software. Facial width-to-height is a well-established indicator of testosterone. What the authors find is that hedge fund managers with high levels of testosterone, as proxied by their facial width-to-height ratio, significantly underperformed lower-testosterone managers.

What’s more, the reasons for worse performance among higher-T managers could often be traced to exactly the sort of things we might suspect from such a finding: reckless risk-taking, stubbornness, and unethical behavior. For example, they find that higher-T managers “are more likely to succumb to the disposition effect.” The disposition effect refers to the tendency of investors to refuse to sell an asset after it has lost them money, even if the original reason for buying it is no longer true. It’s basically the investment version of “refusing to admit you were wrong.” Higher-T managers also “have a stronger preference for lottery-like stocks.” That is, they swing for the fences buying more of stocks that have recently had very high returns, even though such high-fliers are usually a bad bet. Higher-T managers are also more likely to disclose civil and criminal violations on their regulatory filings (form ADVs), suggesting a higher degree of unethical behavior and operational risk, not generally the sort of thing you want from somebody who’s running a complicated and non-transparent investment strategy for you.

Comparing the returns of the 10 funds ran by the managers with the highest indicated levels of testosterone each year with the 10 funds with the least, Lu and Teo find that the low-T funds outperform the high-T funds by 5.80% per year, after adjusting for common risk measures.

This is an incredible performance gap, comparable to the long-run difference in returns between stocks and cash, but instead of contrasting the performance of different assets or different investment strategies like we normally see in graphs like these, we’re basically just looking at whether the guy running the money has a strong jawline or not. Why might testosterone have such a large impact on investment outcomes?

The results of this study are particularly interesting because they stand in contrast to previous research suggesting that male CEOs with wider (more masculine) faces achieve superior financial results for the companies they run (albeit also with greater risk). So manly men are better at running companies but not picking stocks?

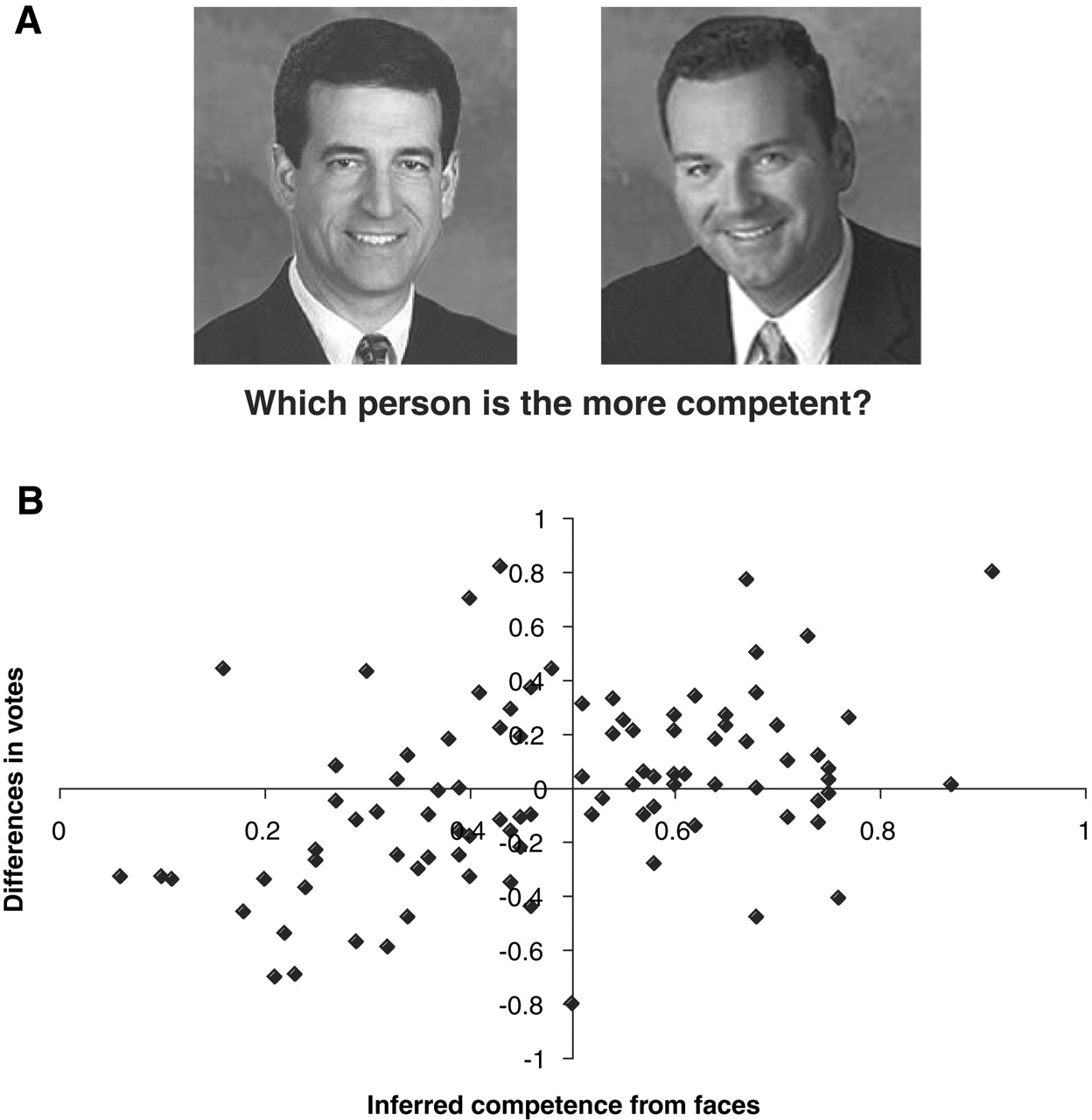

Then there is an even larger literature on how superficial features like one’s face can influence others’ perceptions in ways that have real-world consequences. One influential paper showed subjects side-by-side pictures of two faces for one second and asked them to evaluate who appeared more competent. The faces, it turned out, were candidates in the 2004 US congressional elections, and the respondents’ snap judgments about their faces were able to predict the victor with a high degree of statistical confidence. A later paper was able to replicate the finding using only 100 milliseconds of exposure.

What cues are people using to so quickly judge competence? You guessed it, facial width-to-height. And it’s not just faces, other studies have found that people perceive lower-pitched voices to be more competent and more electable as well. When evaluating say, how effective a leader someone might be, both men and women seem to rely to a large degree on split-second, unconscious impressions largely related to indications of masculinity.

Now, this may have served us in our evolutionary past when the sort of physical strength necessary to run down a woolly mammoth was an important component of leadership. And it’s plausible that when choosing who to run a large company you want somebody with the sort of assertive, confident demeanor that might be correlated with testosterone. But when it comes to how to invest in the stock market, now you’re dealing with an entirely different kind of beast. While boards of directors and company officers may be swayed by your charisma, the market simply does not care what you think, and dealing with such an impersonal and chaotic machine requires an entirely different kind of composure.

So what are good investors made of? One paper that tried to answer this question looked at measures of personality traits and emotional states of day-traders over a several week period and compared them to their investment results. One of the authors, Andrew Lo, writing in his recent book Adaptive Markets, summarizes the findings this way:

Traders who described more intense reactions to both losing and making money performed significantly worse than others. In addition, those who scored higher on a measure of “internality” – the tendency to ascribe the causes of various events in their lives to their own doing versus random chance – also performed much worse than those who scored lower on this scale. These patterns tell us something about the stuff good traders are made of: more controlled emotional responses, including the ability to refrain from blaming (or lauding) oneself too much for trading outcomes.

Not exactly the picture we envision when imagining the highly-masculine alpha male. To this I would add, echoing others, that some of the most important qualities to have when investing are humility, self-criticism, and open-mindedness. These traits will help you avoid throwing good money after bad in the market and allow you to cope with a system that is adapted to outsmart you. The problem is, these are not the same traits that make you persuasive to other people, like the people who you’re trying to convince to invest with you. This might be the fundamental problem with investment management and why markets can be so consistently irrational: the people who are good at managing money are not necessarily the ones who are any good at convincing people to give it to them and the people who are able to persuade others to give them money might not be any good at managing it.

Just remember, nerds > jocks when it comes to investing. Granted, as someone who writes blog posts about academic papers on facial width-to-height ratios, I might be a little biased.

Disclosures: This post is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place. Please contact us at your earliest convenience with any questions regarding the content of this post. For actual results that are compared to an index, all material facts relevant to the comparison are disclosed herein and reflect the deduction of advisory fees, brokerage and other commissions and any other expenses paid by RHS Financial, LLC’s clients. An index is a hypothetical portfolio of securities representing a particular market or a segment of it used as indicator of the change in the securities market. Indexes are unmanaged, do not incur fees and expenses and cannot be invested in directly.

2024 Disclosures

RHS Financial is an SEC registered Investment Advisory Firm and distributes this presentation for informational purposes only. This presentation ( hitherto referred to as the presentation throughout this disclosure), blog post, infographic, slide deck or whatever form of informational modality the reader wishes to describe this as is provided for informational purposes only and should not be construed as investment advice in any way.

We believe the information, including that obtained from outside sources, to be correct, but we cannot and do not guarantee its accuracy in any way. RHS Financial uses information from outside sources to develop graphs, charts, infographics, etc. to enhance this presentation and while we believe the information from these outside sources, to be correct, we cannot and do not guarantee its accuracy in any way,

Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors who may be employees of but do not necessarily reflect the views of RHS Financial as a company. There can be no guarantee that developments will play out as forecasted. The information in this presentation is subject to change at any time without notice. This presentation contains “forward-looking statements" concerning activities, events or developments that RHS Financial expects or believes may occur in the future. These statements reflect assumptions and analyses made by RHS’s analysts and advisors based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Because these forward-looking statements may be subject to risks and uncertainties beyond RHS Financials’ control, they are no guarantees of any future performance. Actual results or developments may differ materially, and readers are cautioned not to place undue reliance on the forward-looking statements. In a nutshell; these are our best guesses and please don’t assume they are fact.

Mentions of specific securities, investment products, investment indices, companies or industries should not be considered a recommendation or solicitation. Data and analysis does not represent the actual or expected future performance of any investment or investment product Index information is used to illustrate general asset class exposure, and not intended to represent performance of any investment product or strategy.

This post may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with RHS Financial and does not sponsor, endorse or participate in the provision of any RHS’ services, or other financial products. Index information contained herein is derived from third parties and is proffered to you unaltered as we derived it from the third party.

RHS Financial, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where RHS Financial, LLC and its representatives are properly licensed or exempt from licensure. This presentation is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place.

If the client is deemed suitable and agrees, RHS may employ leveraged strategies for these clients. Leverage attained through margin on a client’s account can add additional risk. While RHS tends to seek to improve return with theses strategies by applying leverage to less risky indexes, there is no guarantee that that RHS will lower risk or improve returns.

RHS Financial. 4171 24th St. Suite 101 San Francisco, CA 94114