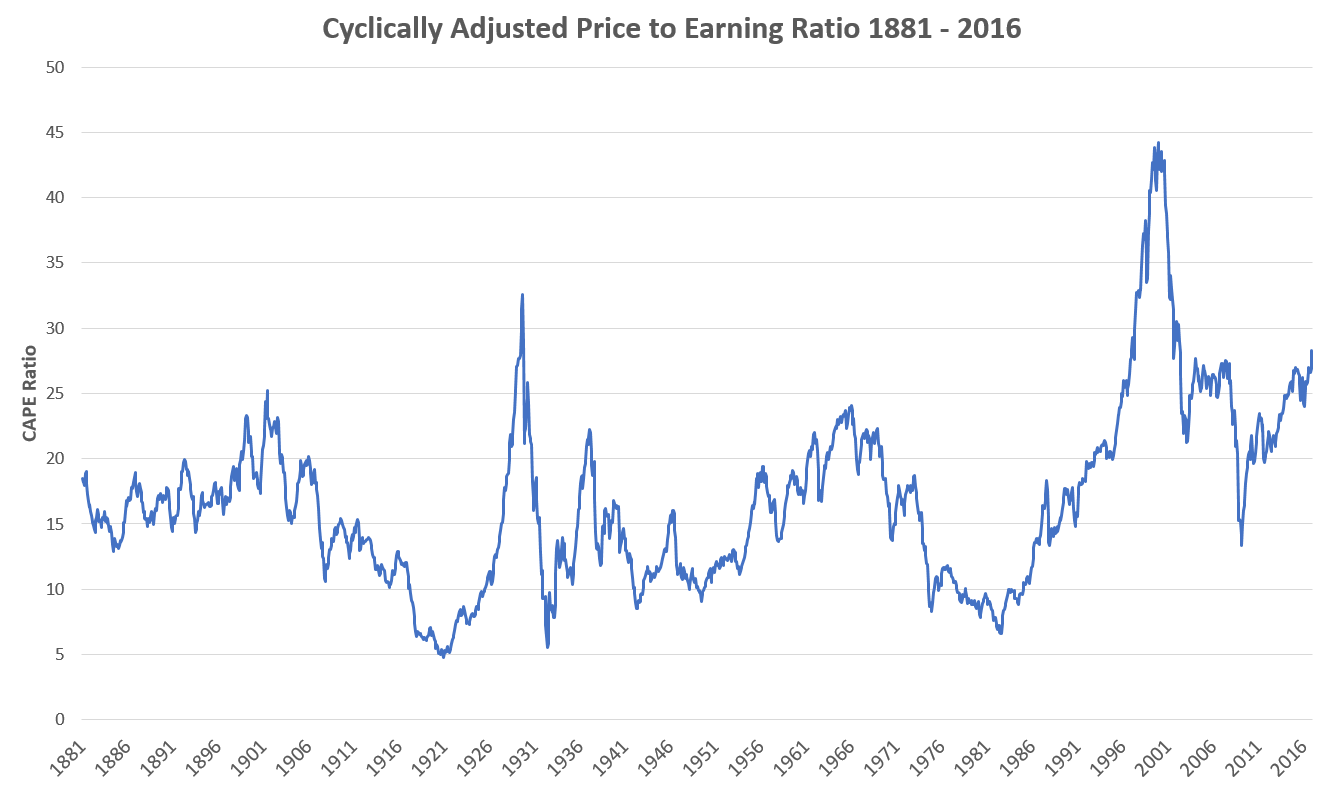

The S&P 500 finished the year up 11.96% for 2016, marking the eighth straight year in a row the US stock market has posted a gain in what is now the 2nd longest bull market in history. And if this keeps up through March it will become the number one longest bull market in US history, stealing the title from that long-time champion, the roaring twenties. But that is not all today’s stock market has in common with the late 20s; today’s valuations are similarly lofty. Below I plot the cyclically adjusted price to earnings ratio (CAPE), a widely-used metric for gauging how expensive the market is.

Source: Robert Shiller’s Website

The CAPE ratio compares the average inflation-adjusted aggregate earnings over the last ten years on the stock market to its current market capitalization. The higher the number, the more investors are paying for firms’ earnings. Nobel Laureate Robert Shiller popularized the measure in his book Irrational Exuberance, published at the zenith of the dot-com bubble, and showed that the higher the CAPE, the lower the returns on the market were over the next several years, and argued that the market was dangerously overvalued at the time.

Well, with the turn of the year the US market’s CAPE ratio has now surpassed 28, a figure that has been reached only twice before in US history:

- In 1929, on the eve of the Great Depression, and

- In 1997, near the height of the dot-com bubble

Suffice it to say, the years following both these periods did not treat US investors kindly.

Should I Start Panicking?

No, please don’t panic. First of all, today’s environment is completely different than that of the late 20s or 90s. For example, the 1929 market crash happened against the backdrop of a rising wave of protectionism around the world, and the late 90s dot-com boom was a tech frenzy in which investors hurled money at anybody in Silicon Valley who had an idea for a startup. Oh wait…

Seriously though, it’s important in investing to use statistics, not anecdotes. What do the statistics say?

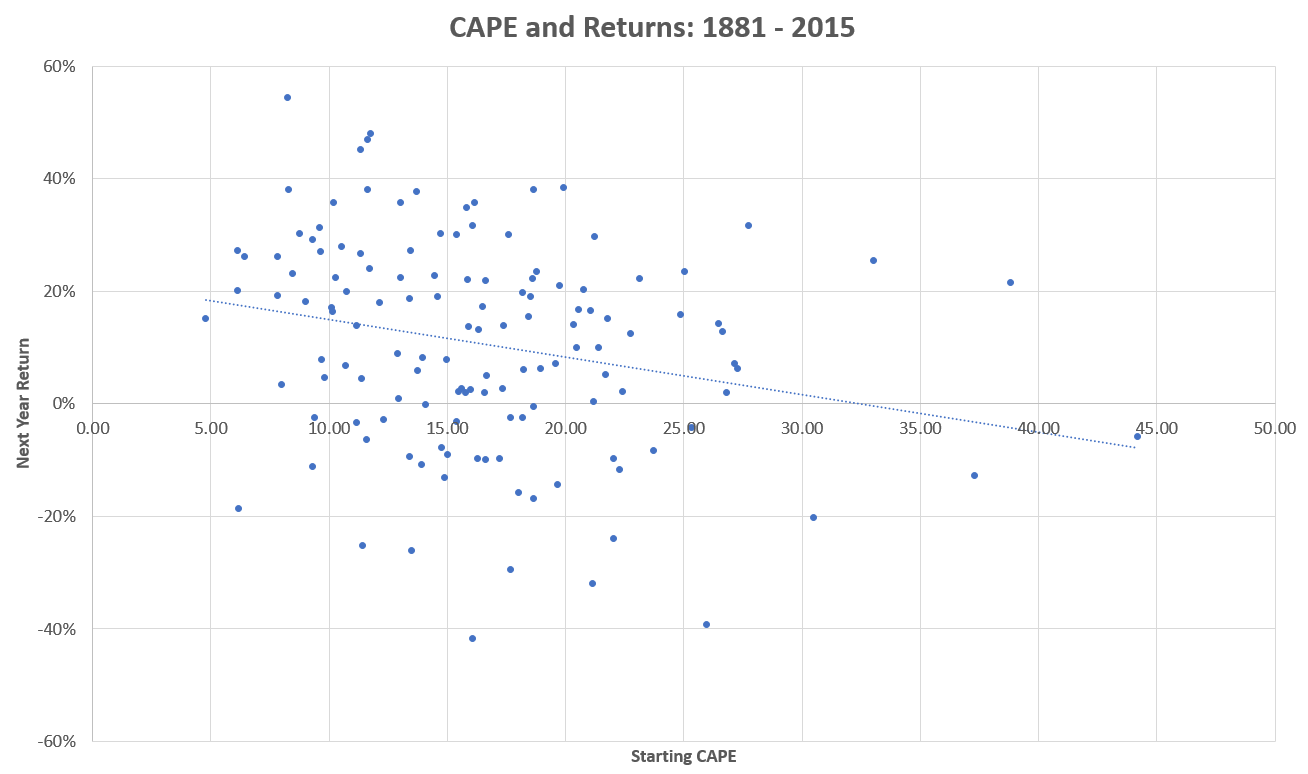

First of all, they say that predicting the return on the stock market is hard. In their 2008 paper, Predicting Excess Stock Returns Out of Sample: Can Anything Beat the Historical Average? Campbell and Thompson ask the question, can anything beat using the historical average when predicting excess stock returns out of sample? That is, if the long-run average return on the S&P 500 is about 9.8%, can I do any better than simply assuming this going forward using information I have right now? Answering this is not as straightforward as it might sound. It’s that “out of sample” bit that’s tricky. For example: here’s a scatterplot of annual US stock returns against their starting CAPE:

Source: Robert Shiller’s Website

There’s indeed a negative relationship, albeit a pretty noisy one, and the regression line over our current point of 28 is barely above zero. But using this regression when explaining the past is sort of cheating. An investor in 1920 would not have had the benefit of knowing at the time that she was investing in the cheapest market of the 20th century, and would have estimated a much different relationship between CAPE ratios and returns even if she had access to the data. Campbell and Thompson try to address this by assessing the predictive ability of different variables over time using only then-available data. Testing a laundry list of variables related to profitability, growth rates, interest rates, inflation, and valuations, they universally find that anything that works in-sample has much less explanatory value out-of-sample, and sometimes doesn’t work at all. The most robust variable they test is indeed the smoothed earnings yield (simply the reciprocal of the CAPE ratio), which itself loses half is explanatory power out-of-sample.

This should not be too surprising. It makes sense that valuations are related to future returns, but the exact manner in which the history of the stock market has unfolded is the result of a chaotic interplay between technological, demographic, political, and other trends that we shouldn’t expect to see repeated. With that in mind, Campbell and Thompson rerun their experiment but constrain the parameters of the variables in various ways in order to cohere better with our prior knowledge of economic logic. Of the possibilities they test, they find that the most robust way to predict the stock market is to simply assume its return will be equal to the current smoothed earnings yield, or one over CAPE. This is nice, intuitive result that allows us to readily compare equity expected returns to yields on bonds or savings accounts or other assets. Below, I plot the smoothed earnings yield over time against the next 10 year annualized real return on US stocks:

Source: Robert Shiller’s Website

So what does the CAPE/smoothed earnings yield tell us about today’s prospective returns? The current CAPE ratio of 28.26 equates to a smoothed earnings yield and an expected real return of 3.54%. Add in an expected inflation rate of about 2% for a 5.54% nominal expected return. Barely half of the long-term historical averages, but hardly catastrophic.

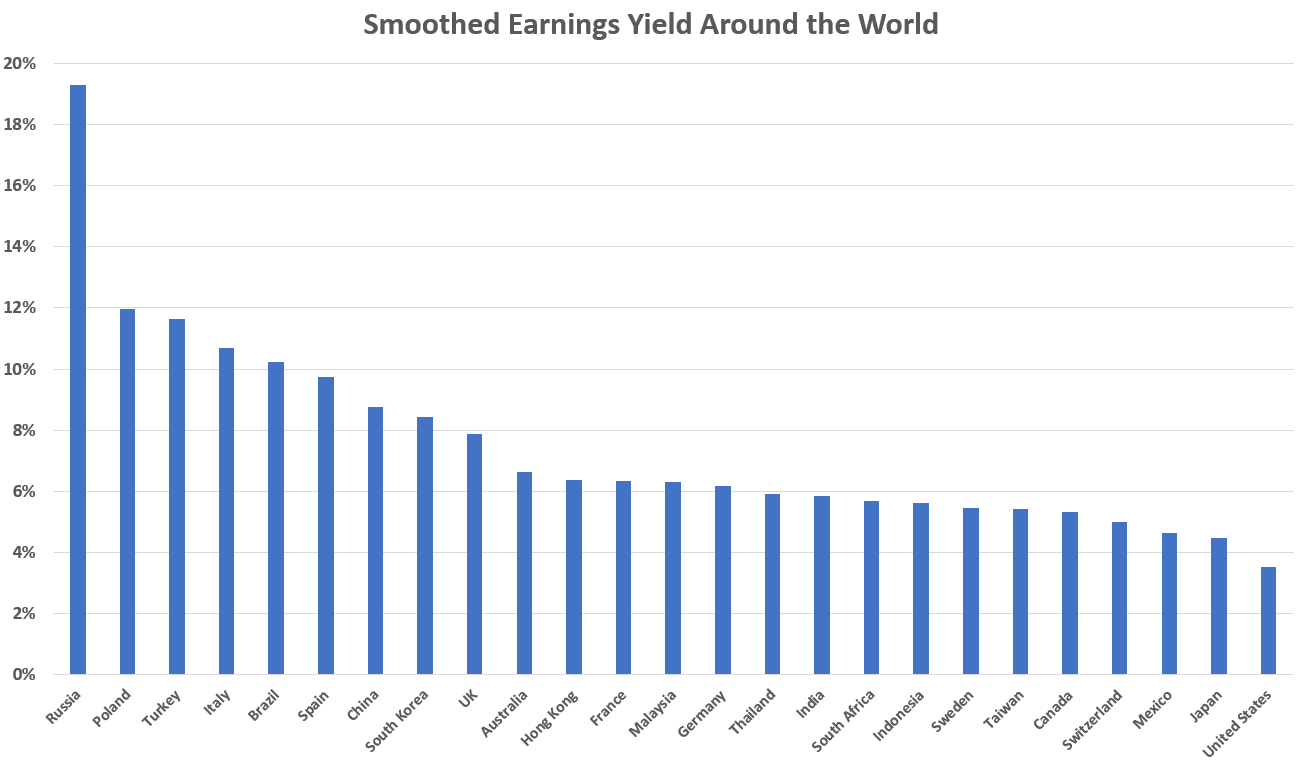

Fortunately, the United States is not the only market available to invest in, though it is currently the most expensive. Many of the markets around the world have had more prosaic returns over the last eight years and are much more attractively priced. 2017 might be a good year to travel abroad with your investments.

Source: Robert Shiller’s Website, Research Affiliates

Disclosures: This post is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RHS Financial, LLC unless a client service agreement is in place. Please contact us at your earliest convenience with any questions regarding the content of this post. For actual results that are compared to an index, all material facts relevant to the comparison are disclosed herein and reflect the deduction of advisory fees, brokerage and other commissions and any other expenses paid by RHS Financial, LLC’s clients. An index is a hypothetical portfolio of securities representing a particular market or a segment of it used as indicator of the change in the securities market. Indexes are unmanaged, do not incur fees and expenses and cannot be invested in directly.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}